Blackstone's recent bet on digital gaming technology offers a live case study in exactly this shift. In March 2026, Blackstone — one of the world's largest private equity firms — committed $250 million to a newly created company called Advanced Digital Gaming Technology, or ADGT.

The company did not exist before this transaction. It was built specifically for this deal through a four-way alliance bringing together Blackstone, Abu Dhabi-based Raya Holding, NRT Technology, and Sightline Payments.

Blackstone did not buy something that already existed. It put money into building something from scratch — betting on an idea, the people behind it, and the technology they planned to build, rather than on a company with years of revenues and a proven history.

Major deals don't stop in uncertain times — they change shape. And what is happening now across Gulf investment activity reveals a new logic at work: rather than full ownership and centralised control, global capital is moving toward distributed partnerships.

Less money upfront, shared risk, and a deliberate reliance on local partners who understand the regulatory and operational landscape. This was not the preferred structure in stable times. In uncertain ones, it is becoming the smartest.

Full ownership and governance details have not been made public, but the logic of the structure is legible. Each partner brought what it does best.

Blackstone brought the capital — $250 million that almost certainly makes it the largest shareholder, with governance and protection rights proportional to that commitment.

NRT Technology brought venue-level payments infrastructure. Sightline Payments brought the digital wallet layer and the funding and payout rails that move money through the platform.

Raya Holding brought what is hardest to buy outright: local knowledge, regulatory relationships, and the operational ability to execute in a market that works very differently from Western ones.

Commercially, the model likely combines transaction fee-sharing across partners with licensing or royalty-style returns tied to technology use and intellectual property — meaning each partner earns in proportion to what they contributed, rather than through a simple equity dividend.

The deeper question is not what ADGT does, but why Blackstone chose this form of partnership over a straightforward acquisition. The answer points to something structural about how international capital is approaching the Gulf right now.

Multi-party joint ventures spread risk rather than concentrating it in a single balance sheet — which becomes essential when the geopolitical environment is volatile and the cost of being wrong is high.

The investment case for ADGT

ADGT has no operating history — it has not yet opened for business, generated revenue, or proven its model in practice. Blackstone is therefore not investing in what the company has already built.

It is investing in what the company could become, based on one central bet: that being early and well-positioned in a newly regulated market is itself a form of advantage worth paying for.

The market in question is the UAE's emerging licensed gaming sector. The UAE has established a dedicated regulatory authority to oversee and license commercial gaming — a significant policy shift that effectively opens a market that did not formally exist before.

The sector is still in its early stages, and how quickly and broadly licensing rolls out will determine everything. But if the market develops as anticipated, independent industry estimates suggest total annual gaming revenues in the UAE could eventually reach somewhere between $5 billion and $8 billion.

That number could be substantially lower if the rollout is slower or more restricted than expected. There is an important distinction worth understanding here.

ADGT is not a gaming operator — it will not run casinos or take bets directly. It sits underneath the gaming economy, processing the payments that flow through it.

Think of it less like a casino and more like the invisible financial plumbing that makes the casino function. Its revenues would come from taking a small cut of every transaction that passes through its platform, from fees tied to digital wallet balances, and from compliance and identity services embedded in the infrastructure.

This means ADGT's slice of that $5 to $8 billion market is narrower than the headline number suggests. But the model is also more resilient and potentially more profitable — because payment infrastructure earns on volume and scales without the same operational complexity or risk exposure that gaming operators themselves carry. The business grows as the ecosystem grows, without needing to win any individual bet.

What the valuation tells us

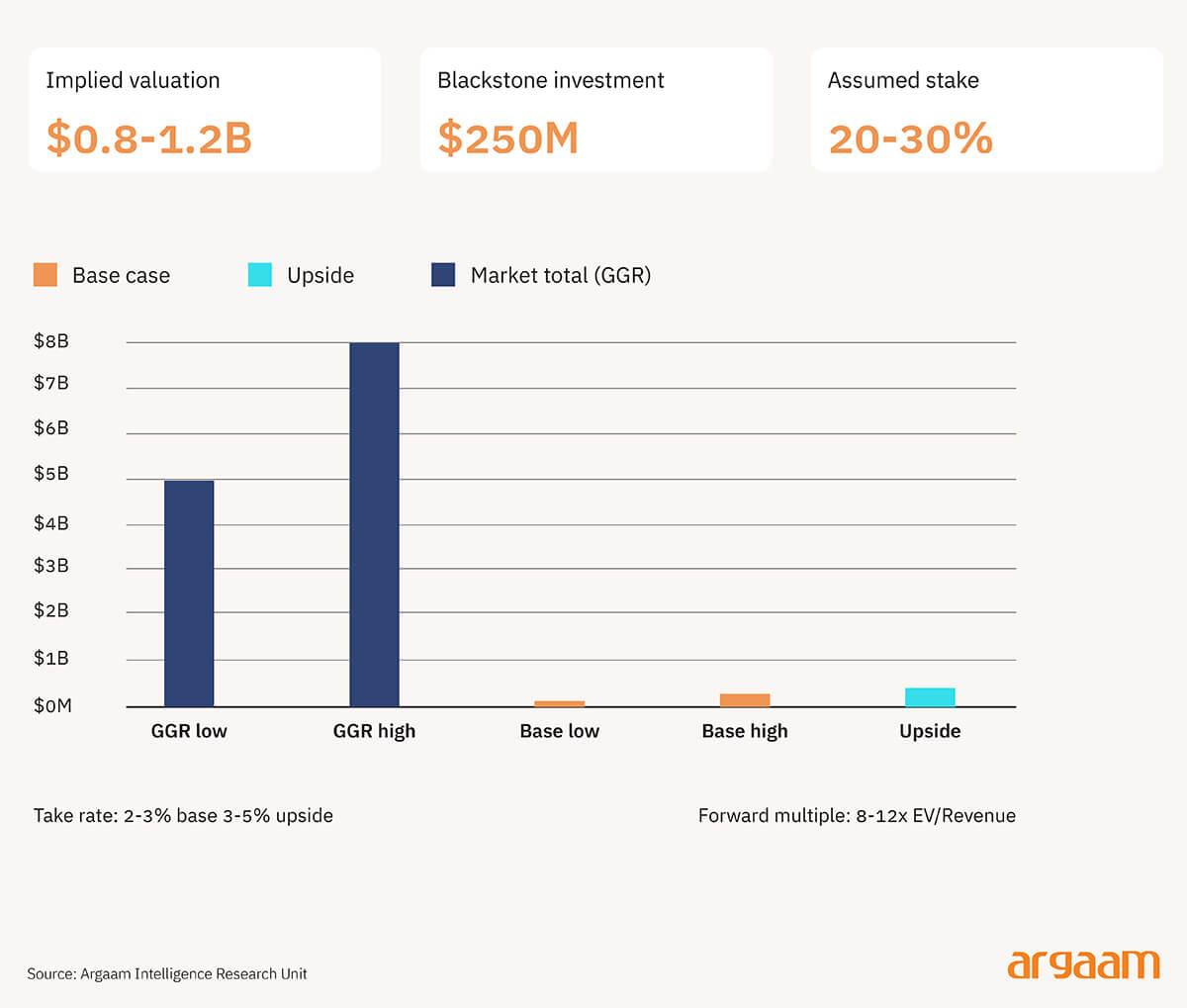

Blackstone has not disclosed the price it paid. But the size of the cheque — $250 million — combined with typical minority stake sizes of 20–30%, implies ADGT was valued somewhere between $800 million and $1.2 billion at the time of investment.

That is a significant number for a company with no revenue history and no established earnings base. It cannot be justified on current fundamentals. It is a forward bet, priced on what the market could become.

Independent estimates put total gaming revenues in the UAE at $5–8 billion once the market is fully operational. ADGT does not capture all of that — it sits in the payments layer and takes a fee on flows passing through it.

A realistic processing fee of 2–3% on those flows would generate roughly $100–250 million in annual revenue in a base case. If ADGT expands deeper into the ecosystem — wallets, compliance, fund movement — that figure could approach $400 million in an upside scenario.

How the valuation is justified

Payment companies with exposure to regulated gaming — Paysafe and Nuvei are the closest listed comparisons — have historically traded at 4–6x revenue.

ADGT is being valued at an earlier stage, so the multiple applied is higher: roughly 8–12x forward revenue, reflecting the scarcity of its regulatory position and the depth of its integration into transaction flows.

Applying that range to a forward revenue estimate of $75–125 million produces a valuation broadly in line with the $800 million–$1.2 billion implied by the investment size.

This is a triangulation, not a precise calculation. The actual outcome will depend on how large the market becomes, what fee rates ADGT can sustain, and whether competitors — new licence holders, operators building their own payment infrastructure, or global payments players — erode its position over time. The valuation is defensible, but it requires most of the assumptions to hold.

✧ Concluding thoughts ✧

The ADGT deal is not a sign that investment across the region is picking up broadly. It shows that large capital can still find a home here, but only in assets with a clear regulatory position and an obvious way to make money. Those assets are rare.

Deal activity will recover, but slowly and selectively. Investors will want to understand the downside before committing, and will release capital in stages tied to milestones rather than writing big cheques upfront.

The sectors that will attract capital are those with structural backing — digital infrastructure, logistics, defence, healthcare. Everything else will wait.

Joint ventures remain the preferred entry route, increasingly with global operators coming in as equity partners alongside local platforms.

The result: fewer deals, larger tickets, and a small number of assets capturing most of the capital.