The UAE’s AppliedAI has recently completed a pre-Series B finacning by Mubadala’s sovereign MENA VC platform. This bridge round follows a $55 million Series A completed in February 2025, backed by a high-profile syndicate including G42, Bessemer Venture Partners and e&.

While modest in size relative to late-stage enterprise AI rounds in the US and Europe, the transaction is significant by regional standards. It represents a meaningful inflection point for enterprise AI applications in the GCC. This analysis from Argaam Intelligence examines the transaction and valuation in the context of broader enterprise AI market dynamics.

Valuation Context

AI valuations have become one of the most actively debated topics in global technology markets, as outcomes increasingly diverge from traditional software benchmarks.

Unlike conventional SaaS, where valuations are more tightly anchored to observable revenue growth, margins and path to profitability, many AI companies are valued primarily on long-term strategic importance, platform potential and control over proprietary data assets.

As a result, headline revenue multiples can vary significantly across different segments of the AI stack. Instead, they differ depending on the specific segment or layer of the AI ecosystem.

The foundation models or large language models (LLMs) might, for example, command higher revenue multiples due to their strategic importance and the value of their proprietary data assets.

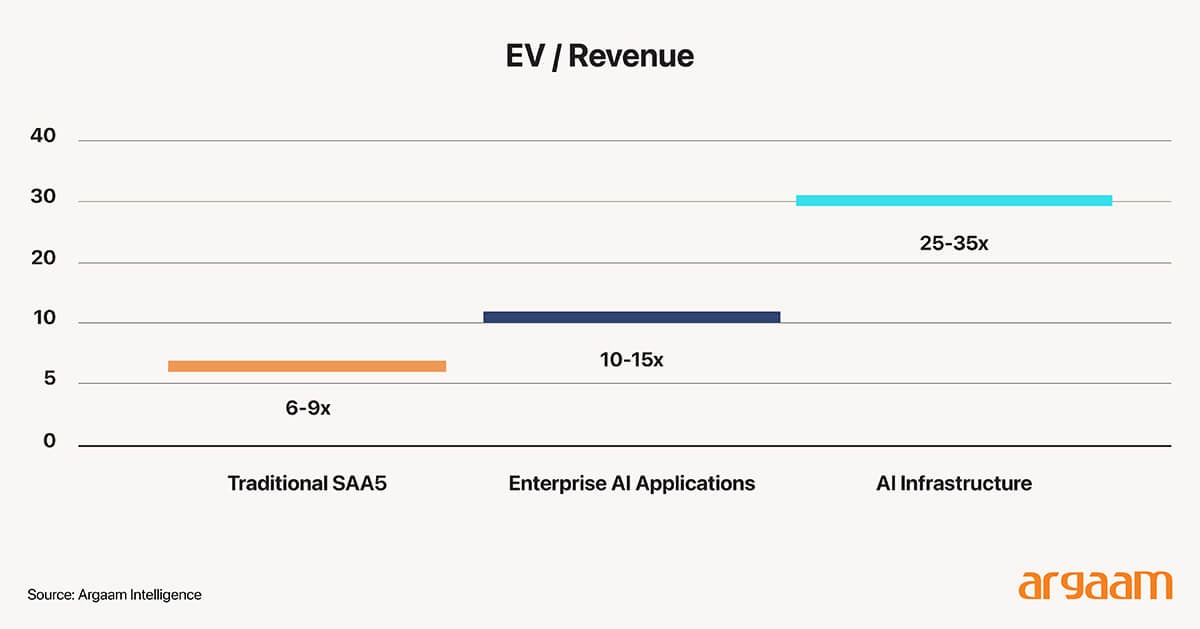

These differences are most noticeable in how the public market values various AI sectors, each exhibiting materially difference EV/Revenue multiples driven by distinct business models, strategic relevance and capital requirements.

● Traditional SaaS: ~6–9× EV/Revenue, serving as a valuation baseline for established software businesses

● Enterprise AI applications: ~10–15× EV/Revenue, representing an ideal level of valuation for high growth platforms such as AppliedAI

● AI infrastructure companies: ~30–35×, with examples including Snowflake and Datadog.

This high valuation shows that these companies are highly effective platforms that are closely integrated into a wide range of enterprise systems, making them very valuable.

✦ Note: Foundational model providers are not yet publicly listed. Private-market valuations for leading players (e.g., OpenAI, Anthropic) are materially higher than other AI segments.

Infrastructure companies often sell for higher prices, sometimes equal to or even more than foundational AI models. This is because core resources like computing power, data infrastructure, and system monitoring are still key limitations for deploying AI.

Additionally, revenues for these infrastructure companies typically grow directly as more AI is used and adopted across industries.

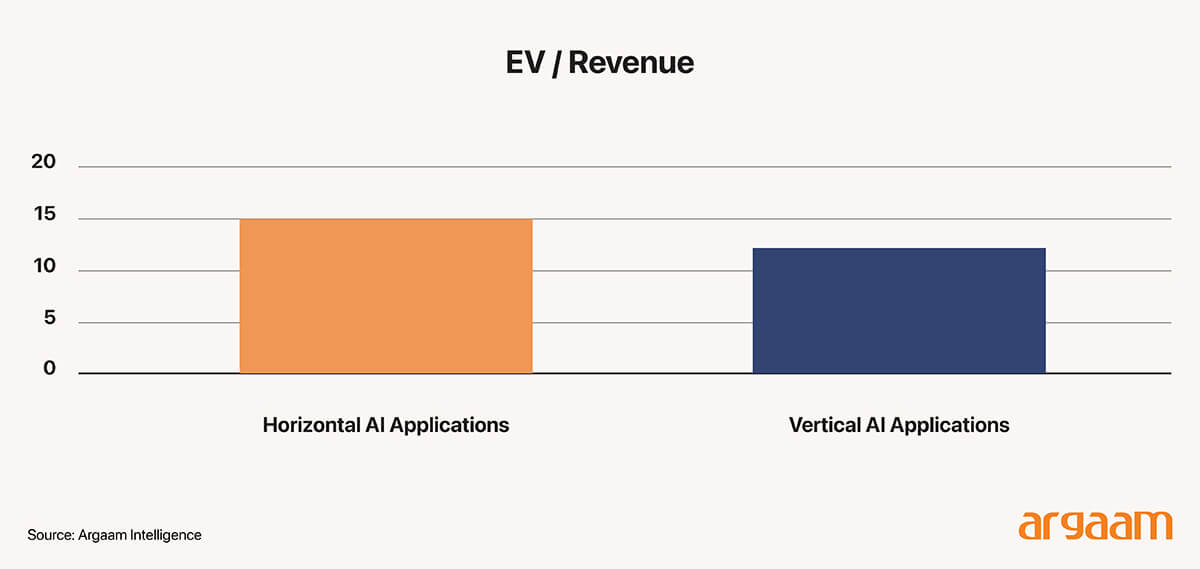

Within enterprise AI applications, valuation multiples further diverge based on product architecture:

➢ Horizontal Enterprise AI – i.e. broad AI platforms that can be used across many different industries. (~12–15× EV/Revenue) – horizontal platforms benefit from cross-industry applicability, larger addressable markets, faster scalability and greater strategic optionality. These attributes support a structural valuation premium relative to more specialized AI solutions.

➢ Vertical Enterprise AI – i.e. designed specifically for a particular industry (~8–12× EV/Revenue) – Vertical AI solutions usually provide more in-depth knowledge of a specific industry, making them harder for competitors to copy and encouraging customers to stay loyal.

However, because these products are highly specialized for one industry, their market is smaller, and selling them can take longer. It is worth noting that vertical AI companies can still outperform horizontal counterparts if they demonstrate clear category leadership and a credible expansion path beyond their initial niche.

Public disclosure of revenue multiples for private AI startups remains limited, as the majority of observable data points stem from primary capital raises rather than traditional M&A transactions.

Available datasets suggest that median revenue multiples across private AI funding rounds have ranged between ~25x-30x. this data is skewed towards the largest and most successful companies and should be interpreted with caution.

Breaking down AppliedAI’s multiple

While no valuation was formally disclosed in AppliedAI’s recent pre-Series B financing, such rounds are typically structured as bridge financings.

These transactions are generally modest in size and designed and aimed at giving the company more time to operate, rather than significantly changing its overall value or price.

As a result, AppliedAI’s post-money valuation is unlikely to have shifted meaningfully from its prior Series A, which valued the company at approximately $300million pre-money (or ~$355 million post-money).

✦ Note: Pre-money valuation refers to the value of a company before any new funding or investment is added.

High-risk valuations usually refer to the company's total value of its shares. For early-stage AI companies, this difference doesn't matter much because they usually have very little debt and often have extra cash from recent funding rounds.

For this analysis, pre-money valuation is therefore used as a proxy for enterprise value. Based on investor commentary suggesting AppliedAI was on track to generate ~$20 million in revenue in 2025, a pre-money valuation of $300 million implies an indicative multiple of ~15× EV/Revenue.

This multiple is illustrative only, given the absence of detailed financial disclosures.

Why a premium multiple is justified

AppliedAI’s core platform, Opus, automates complex, high-stakes workflows across highly regulated industries including banking, healthcare, insurance, energy and government.

Unlike narrowly focused vertical AI, AppliedAI’s horizontal architecture enables reuse across multiple workflows and industries, supporting a larger addressable market and greater long-term strategic optionality.

✦ Note: a platform like Opus would typically refer to a foundational software or infrastructure developed to support the company's AI applications, services, or solutions.

A main advantage of AppliedAI is that it has exclusive access to unique operational data collected directly from real customer workflows. This data helps them build highly specialized AI models for specific industries.

As they deploy their AI solutions more widely across businesses, they gather even more data, which makes their models better. This cycle makes it harder for competitors to catch up and keeps customers loyal to their platform.

AppliedAI has also demonstrated real-world performance in production environments, delivering measurable productivity gains and cost reductions for enterprise customers.

Strategic partnerships with global leaders such as Palantir and McKinsey further validate the platform’s credibility, scalability and relevance to global enterprise deployments.

Conclusion

AppliedAI represents a high-quality enterprise AI asset with strong long-term growth potential. Its indicative ~15× EV/Revenue multiple sits at the upper end of the enterprise AI application range.

This high valuation is justified by the platform’s extensive capabilities, unique data advantages, successful large-scale deployments, and validation from top-tier partners and investors.

The multiple is further justified when benchmarked against recent private AI funding rounds, which frequently clear at higher multiples, and comparable transactions such as DualEntry and Ivo.

Notably, Ivo raised a similarly sized round at a comparable valuation despite operating at a smaller scale, underscoring the reasonableness of AppliedAI’s valuation positioning.

AppliedAI represents a landmark moment for the GCC technology ecosystem. In a region historically dominated by B2C, fintech, and tech-enabled services, its global traction demonstrates that homegrown enterprise technology companies can compete credibly on the world stage.

For founders, the message is clear: enterprise AI demands a global mindset from day one. Over time, durable fundamentals (not hype) will determine the long-term winners in enterprise AI.