In today’s M&A environment, deal structuring has become a central lever for both value creation and risk management. In the US and Europe, transactions particularly in the mid-market remain predominantly sponsor-driven, highly leveraged and control focused.

This paper from Argaam Intelligence offers a comparative lens on key structural and buyer dynamics across regions. We chose the US and the EU versus GCC as a benchmark.

The key insight is not simply to replicate US or European structures but to analyse the underlying M&A mindsets, decision-making patterns and strategic priorities that drive transactions in the different regions.

By recognizing these differences alongside transaction-specific dynamics, GCC start-up founders and investors can better anticipate buyer motivations and structure negotiations more effectively and strategically.

Aggressive Scale vs. Defensive Growth The US and European M&A Playbooks

The US and European M&A markets are among the most competitive globally, underpinned by strong presence of private equity and sponsor-backed capital.

Strategies, however, differ markedly: US firms pursue aggressive, often cross-border expansion, rapidly acquiring assets to scale, whereas European funds are more conservative focusing on home markets.

Unsurprisingly, the US dominates the global private equity landscape, with 72 % of capital raised by the world’s 50 largest PE firms from North America, compared with roughly 10% from Europe.

ℹ︎

Definitions

●Aggressive Scale: The primary intent is to outpace competitors by rapidly increasing the company's size, market share, and influence. ●Defensive Growth: The goal is to protect and consolidate existing market position. Growth is employed strategically to prevent competitors from gaining advantages.

U.S. PE transactions also typically feature higher leverage and broader security packages, reflecting deeper and more sophisticated credit markets. The leverage could in several transactions magnify profits because it allows a private equity firm to invest more money than they have on hand.

If the investment succeeds, the returns are based on the total size of the deal, which includes both the firm’s own money and the borrowed funds. If the borrowed money is cheap based on transaction-related interest rates and can be paid back with the profits, the remaining profit for the firm is magnified relative to its original investment.

European deals, by contrast, tend to adopt a more conservative financing approach with leverage multiples generally lower than the US’s 5.0x-6.0x EBITDA levels in competitive credit markets.

Deal structures in private equity are typically designed to maintain founder alignment, optimize leverage and maximize returns. To ensure founders retain “skin in the game”, transactions often include equity rollovers in which founders / management reinvest a portion of their proceeds as ordinary or preferred equity, or vendor loan notes (deferred payment instruments that accrue interest over time).

Recent data from GF, a leading provider of closed-source transaction data for the private equity-backed middle market, shows about 63.6% of mid-market deals used rollover equity, with the rolled portion averaging roughly 14.5% of the purchase price.

Feature

Ordinary Equity

(Common Stock)

Preffered Equity

(Prefferred Stock)

Voting Rights

Usually yes

Usually no

Dividend

Variable/Optional

Fixed/Guaranteed

Priority in assests

Last

First

Risk

Higher

Lower

In the U.S., strategic buyers are often serial acquirers, particularly in technology, healthcare, and industrials.

Their extensive M&A execution experiences drives a preference for standardized consideration structures:

Cash, stock or combinations, paid upfront or with earnouts depending on valuation gaps, post-closing uncertainties and management retention incentives.

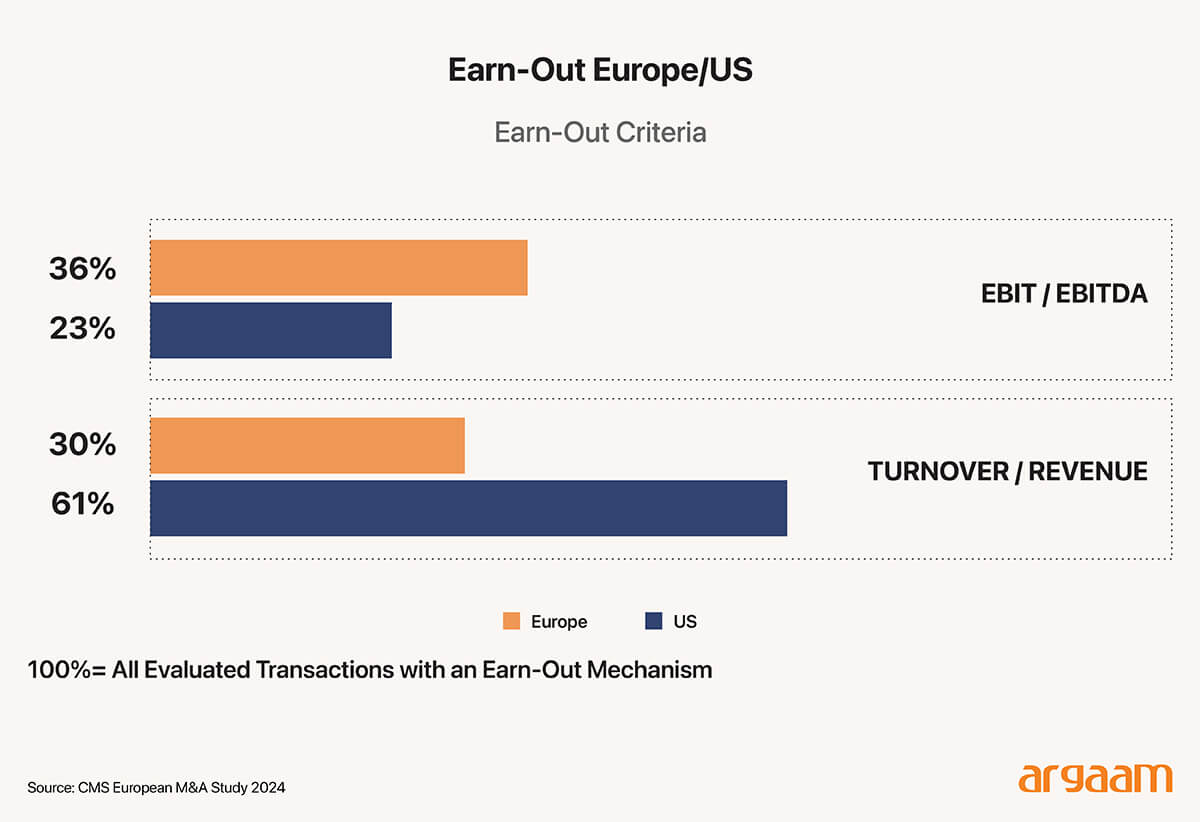

Earn-outs, appear roughly in 33 % of U.S. deals and 25 % of European transactions. However, they differ structurally: US earnouts are usually revenue-based aligned with rapid growth targets, while European earnouts they are typically tied to EBIT or EBITDA, reflecting a more conservative approach.

Earn-outs have become more prevalent in recent years due to market uncertainty and valuation gaps. While they can bridge disagreements and provide upside, careful negotiation, clear metrics, and setting realistic targets are essential to manage potential pitfalls.

Feature

U.S. Earnouts

European Earnouts

Frequency in Deals

Approximately 33% of deals

Approximately 25% of deals

Primary Performance Measure

Revenue (rapid growth targets)

EBIT (Earnings Before Interest and Taxes) or EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization)

GCC M&A Prioritizing Strategic Growth Over Short-Term Returns

The GCC is structurally distinct. Sovereign wealth funds, state-linked entities and large diversified groups dominate, favouring majority or full ownership, long-term hold periods, and simpler, cash-dominant structures.

Emphasizing capability transfer, platform creation and market development rather than short-term financial returns takes center stage.

In the UAE, for example, most private transactions are structured as outright share sales for cash, with limited use of share-for-share consideration or complex contingent structures.

Although this simplifies governance, it concentrates risk with the acquirer, reducing flexibility to share downside with partners. While earn-outs and minority investments are gaining traction in technology and growth sectors, they remain less embedded in GCC deal practice due to control sensitives, governance concerns and trust considerations.

Although cautious adoption may constrain external co-investment, it ensures alignment with long-term strategic objectives, particularly for sovereign-backed projects.

GCC deal-making is often structured around long-term partnerships and platform creation, emphasizing capability transfer and market development rather than short-term financial returns.

Characteristic

Description

Examples / Notes

Ownership

Favor majority or full ownership

Sovereign funds and state-linked entities prefer control

Hold Period

Long-term investment strategies

Focus on capability transfer, platform creation, market growth

Deal Structure

Cash-dominant, simple share sales

Outright share sales for cash, limited complex deals

Use of Co-investments

Limited especially outside tech/growth sectors

Due to control sensitivities and governance concerns

Risk Sharing

Risk concentrated with the acquirer

Limited use of earn-outs or minority investments

Strategic Focus

Emphasis on capability transfer and market development

Less focus on short-term financial returns

Partnerships/Platform Creation

Often long-term, collaborative partnerships

Focus on building platforms for sustainable growth

Consortia and Joint Ventures are growing

Consortium and joint venture (JV) structures in the GCC are frequently strategic, while in U.S. and Europe, consortia are often formed to manage equity sizes, share risk, or navigate regulatory constraints.

Although statistics are limited, JV activity in the Middle East has grown. Increases in FDI related projects (nearly 1,973 in 2024) and large strategic partnerships reflect rising collaborative deal activity that often takes JV or co investment form.

Recent examples include: ●The $11 billion Aramco-led Jafurah midstream consortium, bringing in Global Infrastructure Partners and other investors for long-dated gas infrastructure development.

●A multi-billion-dollar collaboration between Saudi Arabia’s Humain and U.S. semiconductor leader AMD to build a global AI hyperscaler with regional and international data center capacity.

JVs and strategic partnerships are particularly effective in technology, infrastructure, or regulated sectors, where capability transfer and co-investment are critical.

Indeed, joint ventures and strategic alliances have evolved into an important value creation framework. Companies increasingly view these partnerships as strategic instruments to unlock innovation, access new markets, and build resilience, with serial JV dealmakers driving superior shareholder returns.

These structures not only allow organizations to share risk and resources but also help lay the groundwork for future M&A activity.

For start-up founders, forming strategic alliances or JVs can be a way to demonstrate their capabilities and put themselves on the radar of more international buyers, bridging the gap between early collaboration and eventual acquisition opportunities.

While structural differences exist between the GCC and more mature markets in the U.S. and Europe, the increasing prominence of JVs in the region represents both a trend and a playbook worth paying closer attention to.

Regional context provides broad insight but deal structures are ultimately shaped by transaction-specific factors as explained in this table:

Factor

Description/Impact

Buyer Type

Strategic (company buyers)- Private Equity- Sovereign (government)

Seller Profile

Founder/Family-owned- State-owned

Managment Involvement

Dergree of management's participation in deal process

Underlying business strategy and sensitivity to financial changes

Customer & Supplier Contract Risks

Potential risks from key contracts with customers and suppliers

Regulatory Constraints

Legal and regulatory restrictions applicable to the deal

For instance, a US private equity fund acquiring a Middle Eastern tech business will often seek US-style rollovers and earnout structure to align incentives and bridge valuation gaps.

In contrast, a Gulf sovereign investor acquiring a European asset may prioritise full control, strategic integration and long-term partnership over complex financial engineering.

Where a business is highly dependent on a start-up founder and lacks a clear succession or deep management bench, buyers in GCC may require the founder to remain engaged for a defined period post-closing, using mechanisms such as employment agreements, equity vesting, or milestone-based retention, both to reduce operational risk and align incentives.

Deal competitiveness further shapes outcomes. Highly sought-after or strategically critical assets and competitive auctions tend to favour sellers, enabling them to secure premium pricing, upfront cash, and reduced post-closing conditionality, while limiting the acquirer’s ability to impose strict governance or risk protections.

Note local and cross-border regulatory requirements, including foreign ownership limits, antitrust rules and sector specific approvals can materially affect deal mechanics, timing and financing.

In some jurisdictions, regulation dictate whether a minority or stake, joint venture or government partnership is feasible, imposing ownership caps or mandatory local participation.

Key takeaways

Conclusion

For GCC investors, early understanding of mature market deal structures and buyer motivations is not an academic exercise, it is a source of real negotiating power.

It enables investors to shape deal terms proactively (governance, earn-outs, rollovers, control rights) rather than reacting defensively to buyer proposals.

“Speaking the same language” also enhances credibility with international buyers and investors, which can translate into better terms, faster processes and broader buyer interest.

Equally important is selecting partners whose strategic intent aligns with the founder’s own objectives whether that is building a scalable platform, pursuing rapid growth or prioritising margin protection and stability.

Clarity on personal and shareholder goals before entering negotiations is therefore critical to avoid structural misalignment and post-deal friction.

Transparency and deal reporting are equally critical.

In mature markets, granular data on deal terms, valuations and structures enables benchmarking, manging expectations and reduced information asymmetry. GCC markets often lack standardized disclosures which can complicate both local and cross-border negotiations.

Improving market-level reporting can tracking deal data can enhance efficiency, support better-aligned deals and foster greater buyer / investor confidence across the region.

More this Weekend

The Saudi Move from Isolated AI Pilots to Full Adoption in the Healthcare Sector to Reduce Revenue Leakage

Saudi hospitals have made real progress on digital transformation—but the next efficiency gains will come from intelligence, not more digitisation. In practical terms, the Kingdom now has a growing digital care layer (e.g., SEHA Virtual Hospital supports around 224 hospitals and is designed for large-scale virtual service delivery) and mass patient-facing uptake.

Understanding Saudi Arabia’s 11.2% Household Savings Rate: A Positive Sign of Prudence But Underlying Financial Complexities Remain

Saudi Arabia's 2023 Household Income and Expenditure Survey, which’s the latest available dataset and is our baseline in our argument, reveals average monthly household disposable income of SAR 18,056 and consumption of SAR 16,028, implying an 11.2% savings rate—dramatically higher than 2018's 1.6%.