Saudi SISCO HOLDING Holding, through its logistics platform LogiPoint, recently acquired a 51% stake in Public Storage Solutions (PSS).

Before outlining out objective analysis, we would first establish the strategic logic behind the bargain. Without this context, the acquisition looks like a routine real estate deal. With it, it reads as a deliberate, calculated step in a coherent national strategy.

A highly strategic transaction

SISCO HOLDING’s logistics strategy, anchored in its 6×26 strategic framework targeting SAR 6 billion of managed assets by 2026, is focused on building a nationally integrated, asset-backed logistics platform across Saudi Arabia’s core trade corridor.

LogiPoint's existing footprint establishes a critical baseline — not merely as a statement of current scale, but as the reference point against which the true strategic value of the PSS acquisition must be measured.

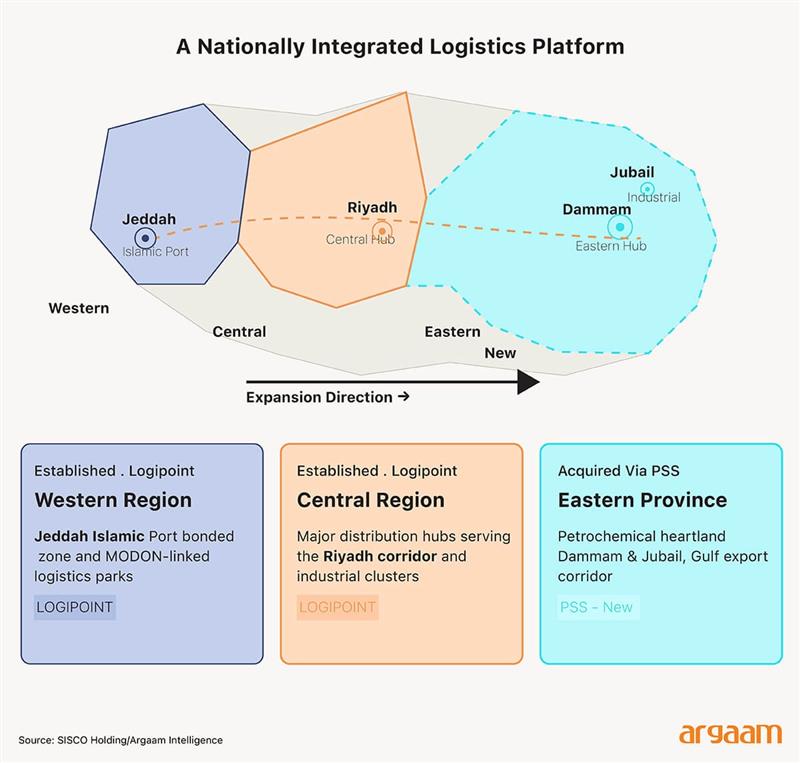

Without understanding what SISCO HOLDING already holds, and where it holds it, the significance of what PSS brings to the table cannot be properly assessed. In this context, PSS is not simply an addition to the portfolio; it is the completion of a geographic logic.

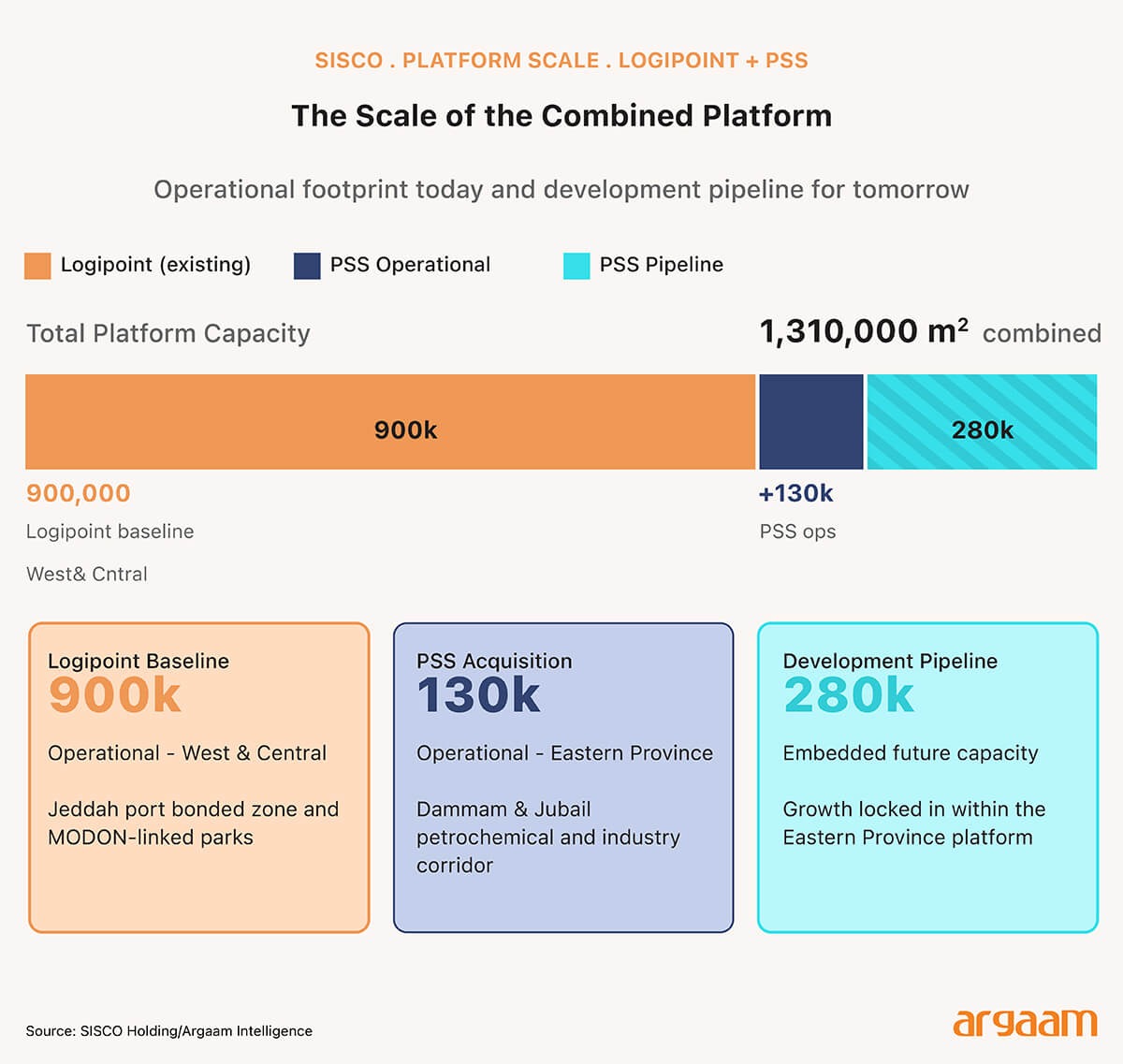

LogiPoint, SISCO HOLDING’s logistics arm, already holds a dominant position in the Western and Central regions, managing approximately 900,000 m² of logistics real estate concentrated around key port and industrial hubs, including the Jeddah Islamic Port Bonded zone and major MODON-linked logistics parks.

PSS provides an immediate and highly important footprint in the Eastern Province, adding over 130,000 m² of operational warehousing across Dammam and Jubail, alongside a substantial development pipeline of approximately 280,000 m².

The Eastern Province is not simply another geography — it is the industrial and energy heartland of Saudi Arabia, home to the Kingdom's petrochemical complex, its heaviest manufacturing clusters, and its principal export infrastructure along the Arabian Gulf.

With operational warehousing across Dammam and Jubail — two of the most freight-intensive cities in the Kingdom — PSS delivers an immediate, income-generating presence in a market that LogiPoint's Western and Central dominance could not reach.

Together, the combined portfolio creates a truly national logistics network spanning Saudi Arabia’s primary import gateways, industrial clusters and export corridors.

This significantly enhances SISCO HOLDING’s ability to deliver integrated, end-to-end logistics solutions while reinforcing its position as one of the few players in the Kingdom with a fully integrated, asset-backed logistics platform at scale.

Why LogiPoint's Growth Is Structurally Sound

As of writing this analysis in mid Feb 2026, full-year audited financials for LogiPoint in 2025 have not yet been published, however, first-quarter performance indicates strong underlying momentum.

Revenue increased by approximately 22.9% year-on-year, supported by improving operating fundamentals. Most notably warehouse occupancy rising to around 90%, a high utilisation level for premium logistics assets that reflects robust tenant demand and limited vacancy risk.

Pricing dynamics also remained favourable. Average rental rates increased by approximately 8.2% year-on-year to around SAR 450 per sqm, demonstrating clear pricing power amid tight supply conditions in high-quality logistics space.

LogiPoint does not simply lease warehouse space — it bundles additional services such as customs handling, freight management, and value-added logistics on top of that space, allowing it to charge more per transaction than rent alone would justify.

The logistics segment of SISCO HOLDING, which includes Logipoint, recorded revenue of approximately SAR 98.3 million in the first nine months of 2025, representing around 10% year-on-year growth compared with roughly SAR 89.5 million in the same period of the prior year.

Broader market data reinforces these trends. Warehouse occupancy across major Saudi logistics hubs remained above 90% during 2024–2025, while rental growth continued across key markets, reflecting structurally strong demand, constrained supply and ongoing industrial expansion.

ℹ︎

LogiPoint's Growth Fundamentals

1) Demand Is Proven, Not Assumed

2) Pricing Power Is Real (Tenants are paying more because they have no comparable alternative.)

3) The Business Model Extracts More Than Real Estate Rent

4) The Tailwind Is Sector-Wide, Not Company-Specific

Revenue outlook for PSS

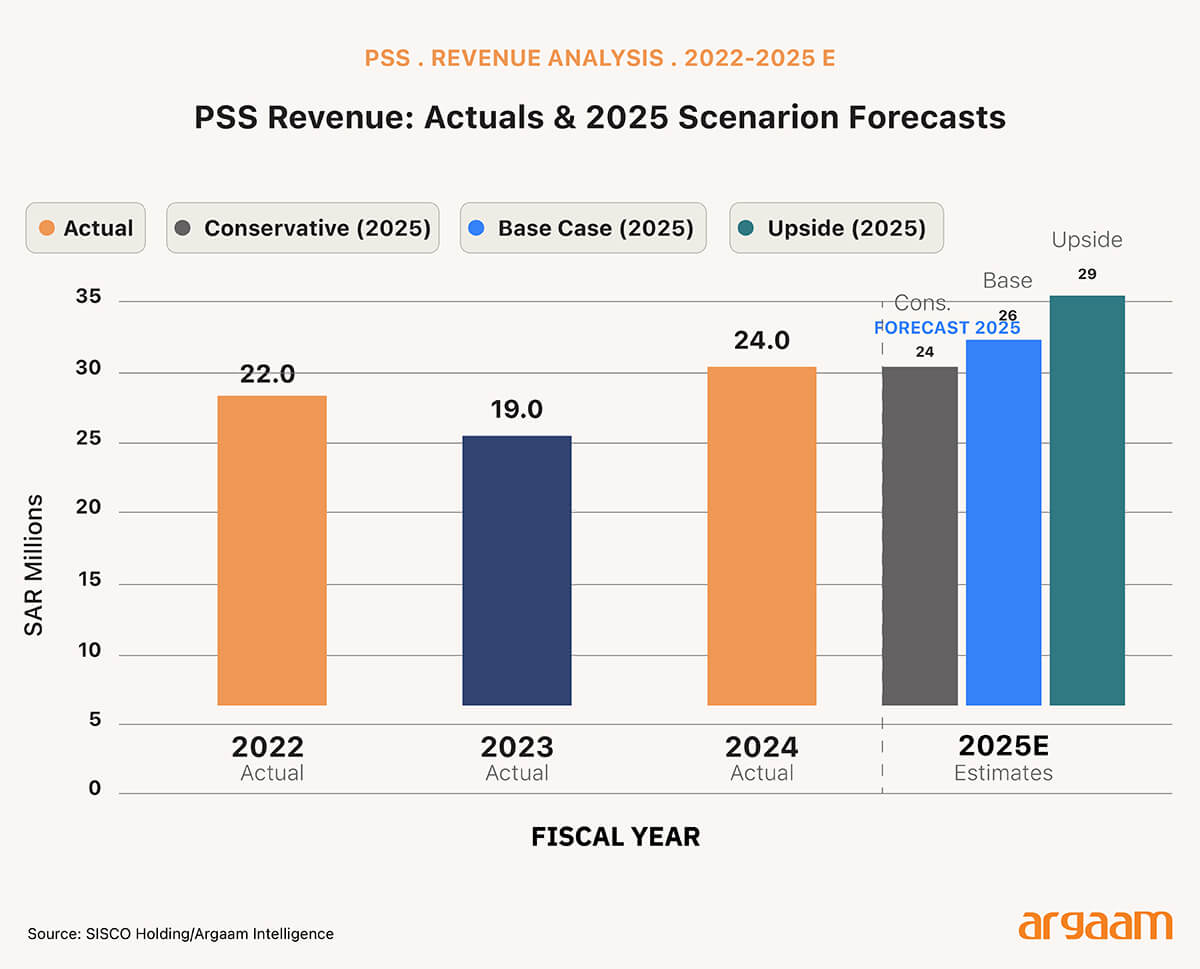

Publicly disclosed financial information on the target (PSS) remains limited. SISCO HOLDING’s transaction disclosures provide only high-level revenue figures for the most recent three fiscal years (2022–2024), with no detailed breakdown of profitability or margins.

PSS recorded a revenue decline in 2023, though no detailed explanation has been provided for this. That said, this kind of short-term fluctuation is common among smaller logistics operators and does not necessarily signal a structural problem.

In this segment, revenues can move up and down depending on when new leases start, when existing contracts come up for renewal, whether rents are being reset to market rates, and how quickly newly built warehouses fill up with tenants. These are timing-driven factors rather than indicators of underlying weakness.

Based on prevailing market conditions and in the absence of major disruptions, PSS’s revenue outlook for 2025 is expected to reflect modest growth.

A reasonable base-case aligned with industry growth rates would imply year-on-year growth of approximately 5–15%, translating to revenues of around SAR 25–27 million.

Under a more conservative scenario, revenue could remain broadly stable at SAR 24 million, while tighter market environment characterized by strong demand and improving utilisation could support an upside case of SAR 28–30 million.

Although PSS’s EBITDA margins have not been publicly disclosed, the acquisition announcement describes the business as highly profitable and scalable.

The inclusion of performance-linked earn-outs tied to financial targets for 2026–2027 further indicates management’s confidence in the company’s profitability and growth trajectory, supporting our conclusion that PSS is already operating on a profitable basis.

For context, logistics warehousing companies that own and operate physical assets typically generate EBITDA margins of around 15–18% once their operations reach a stable, mature state. This is consistent with what LogiPoint's financials suggest.

LogiPoint reports gross margins of approximately 60–65%, but once selling, general and administrative costs of around 40–45% are accounted for, the implied EBITDA margin lands in that same mid-teens range.

In other words, LogiPoint's underlying cost structure is broadly in line with what one would expect from a well-run, asset-backed logistics operator of its type.

➢ Transaction assessment: valuation and long-term value creation

To inform the valuation analysis, SISCO HOLDING paid SAR 132.6 million upfront to acquire a 51% stake in PSS. Scaling this proportionally implies that 100% of PSS is worth approximately SAR 260 million in total equity value.

The transaction also includes performance-based earn-outs of up to SAR 40.8 million. However, these contingent payments are excluded from our multiple analysis as they are forward-looking and dependent on future performance.

Applying sector-typical EBITDA margin assumptions to the reported 2024 revenue of SAR 23.6 million, or an estimated 2025 base-case revenue of approximately SAR 26 million, and using equity value as a proxy for enterprise value, results in a high implied valuation multiple.

Even under relatively optimistic margin scenarios consistent with logistics real estate benchmarks, the transaction implies an EV/EBITDA multiple of approximately 50–60x.

✦ Note: the EV/EBITDA multiple is asking: how many years of operating profit would it take to justify the total price paid for this business?

For context, logistics sector transactions are typically assessed on an EV/EBITDA with asset-light logistics, third-party logistics, and fulfilment operators generally transacting in the ~8–12× EV/EBITDA range.

✦ Note Fulfilment operators are companies that specialise in the end-to-end process of receiving, storing, packing, and dispatching orders on behalf of other businesses — typically e-commerce retailers.

More automation-intensive or value-added logistics platforms may command modestly higher multiples. Recent comparable transactions include acquisitions by Bpost of Staci and GXO Logistics of Wincanton, both executed at approximately 12x EV/EBITDA.

However, direct comparison should be interpreted cautiously. First, the referenced transactions involved significantly larger platforms where scale and more mature earnings bases naturally result in lower observable multiples.

PSS looks expensive on paper if you judge it purely by its current earnings — but that is the wrong lens. The business is still in a growth and build-out phase, meaning its warehouses are not yet fully occupied and its development pipeline has not yet converted into revenue.

SISCO HOLDING is not paying for what PSS earns today — it is paying for what PSS will earn once the pipeline is built out and the assets are fully utilised.

A standard EV/EBITDA calculation cannot capture that forward value, so the multiple looks stretched even though the price may be entirely rational when viewed through a long-term asset ownership lens.

Concluding Thoughts

Value creation hinges on occupancy improvement, rental rate optimisation, and cross-platform service integration — levers that are executable but execution-dependent.

The transaction's strategic premium is justified by structural demand tailwinds rather than current earnings. The phased ownership structure reflects a broader shift in Saudi M&A toward performance-linked consideration and managed ownership transitions, which de-risks pricing while preserving management alignment and compounding long-term value.