In the context of the ongoing Iran conflict, distinguishing short-term market volatility from structural economic impact is essential for investors and dealmakers in the GCC.

While heightened uncertainty may slow transaction timelines and increase risk premiums, history shows that dealmaking rarely stops altogether.

This article examines how the Iran conflict could influence M&A dynamics across the GCC, focusing on potential shifts in valuation expectations, deal structuring and due diligence practices.

Drawing on lessons from past geopolitical disruptions, we assess the likely resilience of the region’s dealmaking environment and the implications for investors and corporate acquirers.

Valuation Implications

Major geopolitical shocks, particularly military conflicts, can raise sovereign risk premiums in emerging markets by approximately 45–180 basis points, as investors demand greater compensation for heightened uncertainty and potential macro-financial stress.

✧ Note: Sovereign risk premium is the extra return/interest rate that investors demand to lend money to a country's government, compared to lending to a country safe from geopolitical tensions.

When buying a company or concluding an M&A deal in a risky country, investors need to know: What return do I need to make this investment worth it?. This formula answers that question.

COE=RfR+β×ERP+CRP

Where:

COE = Cost of Equity: What return do investors demand for putting their money into this company? The higher the risk, the higher return they demand.

RfR = Risk-Free Rate: The minimum return an investor expects even with zero risk.

β (Beta) × ERP (Equity Risk Premium) Beta measures how volatile this specific company is compared to the market. ERP is the extra return investors demand for investing in stocks generally rather than safe bonds.

CRP = Country Risk Premium The extra return demanded specifically because the company operates in a risky country.

When a country becomes riskier, investors charge more to invest there. This extra charge gets added directly into the return any company in that country must promise investors to attract their money.

In M&A markets, higher risk premiums typically translate into higher discount rates and lower transaction multiples. Investors often apply valuation discounts of 5–10% during periods of elevated global geopolitical risk, particularly when conflicts affect markets broadly but only indirectly impact the region.

This discount can widen to 10–20% when conflicts are regionally concentrated, directly affecting the target market, supply chains, or operating conditions.

✧ Note: These valuation effects are most pronounced when geopolitical disruptions are persistent or structurally significant. By contrast, short-lived or localized events may generate volatility but often do not materially affect underlying valuations.

Importantly, geopolitical instability impacts sectors unevenly. In the short term, cyclical industries such as hospitality & tourism, leisure, real estate and aviation often experience declines in valuation multiples.

By contrast, sectors tied to cybersecurity & defence, supply chain resilience, food security, and energy logistics may also face temporary operational disruptions, but over the longer term they tend to be more resilient, and in some cases, valuations can even increase as heightened strategic importance attracts capital and supports stronger risk adjusted returns.

Granular M&A valuation data from earlier conflicts, including the First Gulf War and the Iraq War, is largely unavailable, as deal reporting at the time lacked the detail of modern transaction databases.

However, equity market performance can serve as a useful proxy for valuation shifts, since changes in sector-level market pricing often influence private market expectations and transaction multiples.

Historically, GCC and global equity markets have experienced short-term dips (around 10–15%) during major conflicts but tend to recover within a year and often deliver strong gains thereafter.

Market performance, however, can vary across countries and sectors depending on investor sentiment, economic structure and index composition.

Recent market movements illustrate this divergence. Over the first week of the conflict in the Middle East, Dubai’s equity index fell roughly 9%, while Abu Dhabi declined by around 3–4% and Kuwait slipped approximately 0.3%.

UAE markets have been particularly affected given their heavier exposure to cyclical sectors such as real estate, aviation and tourism, which are more sensitive to geopolitical disruptions.

By contrast, Saudi Arabia’s Tadawul All Share Index gained roughly 2–5%, supported by stronger oil prices and the market’s heavier weighting toward energy and materials stocks.

M&A deal activity and deal structuring

While valuations may remain under pressure, dealmakers are expected to navigate the market carefully, reflecting a “proceed with caution” approach to M&A activity.

At the same time, investors must balance this caution with opportunism, as periods of market dislocation can create attractive entry points that may not persist once conditions stabilize.

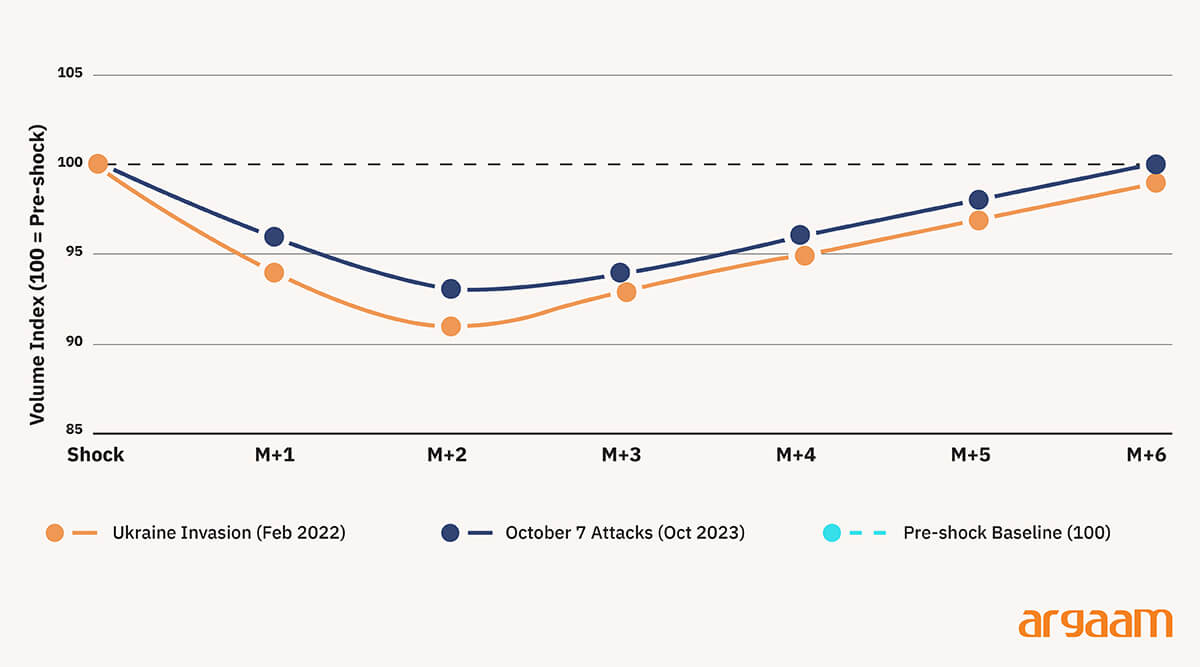

M&A volumes typically decline in the six months following major geopolitical shocks.

However, historical events such as Russian invasion of Ukraine and the October 7 attacks indicate that the slowdown is generally modest, with deal activity falling by less than 10%, suggesting a temporary pause rather than a sustained contraction in transaction activity.

✦ Note on the chart:

◆ Both shocks caused an immediate drop — deal volumes fell within the first 1–2 months after each event, with the Ukraine invasion showing a slightly sharper decline than the October 7 attacks.

◆ Neither decline exceeded 10% — both lines stayed above the 91–93 index range, confirming the slowdown was modest relative to the pre-shock baseline of 100.

◆ Recovery was swift in both cases — by Month 6, deal activity in both events had largely returned toward the baseline, confirming a temporary pause rather than a prolonged market contraction.

Outbound versus Inbound and deal restructuring

Recent announcements suggest that dealmaking has remained resilient despite rising geopolitical tensions. In the past week, a consortium backed by the Qatar Investment Authority agreed to acquire AES Corporation in a $10.7 billion transaction.

while Aluminium Bahrain, controlled by the kingdom’s sovereign fund, moved to acquire Aluminium Dunkerque, the European Union’s largest primary aluminum smelter.

Ultimately, much will depend on the conflict’s duration, but for now, outbound deals from the region are expected to outpace inbound activity.

As deal flow continues despite geopolitical uncertainty, investors are increasingly focused not just on whether transactions happen, but on how they are structured to mitigate risk.

We expect heightened geopolitical risk will prompt parties to reassess contractual protections and evaluate how evolving conditions may affect deal assumptions.

Buyers will increasingly demand flexible deal structures — such as delayed payments and performance-based pricing — to manage disagreements over company value, especially when future revenues or profits could be hurt by regional conflict and disrupted supply chains.

The same thing happened during COVID-19. When nobody could predict how businesses would perform, buyers and sellers stopped agreeing on fixed prices — instead, they structured deals where the final payment depended on how the business actually performed after closing. This approach was used in roughly 35% of all deals in 2020, far higher than normal.

While today's geopolitical tensions are very different from a global health crisis, both situations share one thing in common — deep uncertainty about the future.

Transaction documentation may also increasingly incorporate provisions designed to address geopolitical exposure.

Traditional force majeure clauses may be complemented by conflict-specific triggers, such as shipping disruptions, cyberattacks or infrastructure vulnerabilities linked to regional tensions.

Outlook and Opportunities in the GCC

Different investor groups are likely to respond in distinct ways as market conditions evolve. Private equity sponsors typically adopt a more cautious approach during periods of heightened uncertainty, delaying transactions or favouring structured investments.

Unlike cautious investors, major companies with strong finances often see uncertainty as an opportunity rather than a threat. When markets are nervous and valuations fall, they move quickly to buy competitors, take control of their supply chains, or acquire businesses in sectors critical to their operations.

We anticipate that sectors such as logistics, energy services, digital infrastructure, industrial manufacturing, and defence and security will continue to attract strategic investment, given their critical role in securing supply chains and supporting long-term economic resilience.

Sovereign wealth funds, insulated by substantial fiscal reserves, are uniquely positioned to deploy capital precisely when others retreat — converting market dislocation into strategic advantage.

Their counter-cyclical mandate allows them to acquire dual-use technologies and critical capabilities at compressed valuations, while simultaneously anchoring inbound investment aligned with long-term national transformation agendas.

The broader implication is significant. While geopolitical friction may extend deal timelines and compress near-term activity, the GCC's structural advantages — deep liquidity, diversified revenue bases and state-backed investment mandates — create a dealmaking environment that is fundamentally resilient.

For investors with conviction and capital, the current environment does not signal retreat. It signals selective, high-conviction deployment into markets where long-term fundamentals remain intact despite short-term noise.

Conclusion:

The real risk in today's environment is not that deals fail to close — it is that sellers accept artificially depressed valuations under the pressure of uncertainty, locking in permanent losses from what may prove to be a temporary dislocation.

Historical precedent consistently shows that geopolitical risk premiums embedded in valuations during periods of acute stress tend to overshoot, correcting sharply once clarity returns. Founders who understand this asymmetry — and have the financial runway to wait — hold significant negotiating leverage.

The question is not whether to transact, but whether the price being offered today genuinely reflects long-term business value or simply the market's current anxiety.