United Pharmacies' acquisition of Kunooz for over SAR 100 million is not an isolated transaction — the company's CFO has confirmed two additional deals in the pipeline, one expected to be the largest in the sector's history, with the combined strategy targeting a market share increase from 10% to 13% by end of 2026.

Saudi Arabia's pharmacy retail market is consolidating fast. The three largest chains — Nahdi, Al-Dawaa, and United Pharmacies — have reached a size where their networks, procurement leverage, and capital reserves are effectively barriers that smaller operators cannot replicate.

For those mid-tier chains, the strategic options have narrowed: sell now at a reasonable valuation, or risk becoming irrelevant as the gap widens and the price drops.

Market Landscape of Pharmacy Retail in Saudi Arabia

Saudi Arabia represents the largest pharmacy retail market in the GCC and is among the fastest-growing globally. Industry estimates place the market at approximately USD 12–14 billion, with a projected compound annual growth rate (CAGR) of 6–8% over the coming years.

The Kingdom has more than 9,000 pharmacy outlets nationwide, yet despite its scale the market remains highly fragmented, with a significant share still operated by independent players (Expertmarketresearch).

The market is dominated by two national champions that together control roughly half of pharmacy retail.

Nahdi Medical Company holds the leading position, operating more than 1,100 pharmacies and accounting for roughly 30–35% market share.

Al Dawaa Medical Services ranks second with approximately 900 locations nationwide, representing around 20–25% market share.

Below these leaders sits a long tail of mid-tier chains and thousands of independent operators, many of which face structurally weaker purchasing power, thinner margins and limited digital capabilities.

As a result, these smaller players represent the primary targets for consolidation and remain the central driver of ongoing M&A activity across the Saudi pharmacy retail sector.

Transaction Overview: Strategic Bolt-On to Accelerate Scale

United Pharmacies Company (UPC) is one of Saudi Arabia's oldest pharmacy retail chains, operating as a mid-tier national player with a concentrated presence in major urban centres.

Kunooz Pharmacies runs a broader healthcare retail model that spans pharmacy sales, wholesale pharmaceutical distribution, cosmetics and personal care, and medical supplies — making it a more diversified asset than a standard pharmacy chain.

The deal involved the full acquisition of Kunooz's pharmacy network for a consideration exceeding SAR 100 million. Before the transaction, UPC operated approximately 500 stores, with its heaviest concentration in Riyadh, Jeddah, the Makkah–Taif corridor, and Medina, plus smaller clusters in Asir and the Eastern Province.

Kunooz adds roughly 90–110 locations, more than half of which sit within the Riyadh metropolitan area — precisely where UPC is already strongest.

That geographic overlap is the deal's core logic.

In pharmacy retail, density within a single city drives more value than scattered national presence: it lowers last-mile delivery costs, strengthens supplier negotiating leverage, and makes it easier to consolidate back-office and logistics infrastructure.

Riyadh, as UPC's largest market, offers the most immediate return on that densification. Secondary clusters in Jeddah, Makkah and Medina provide further room for footprint rationalisation, while other regions represent incremental rather than strategic gains.

What the deal does not do is close the gap with the market's two dominant players. Nahdi and Al-Dawaa continue to operate networks that dwarf UPC's combined post-acquisition footprint — meaning this transaction consolidates UPC's position within the mid-tier rather than repositioning it as a national champion.

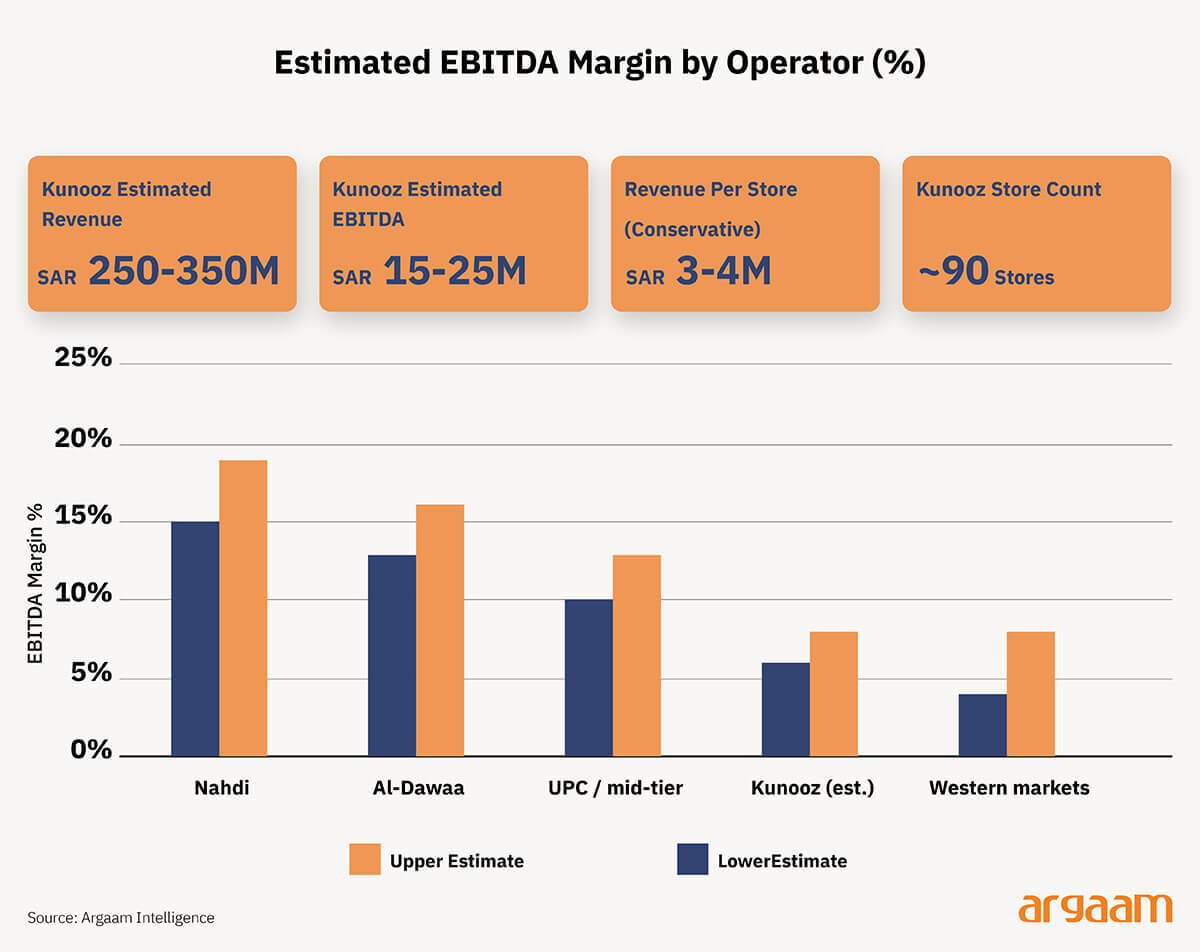

Estimating Kunooz Financials

Financial information for Kunooz Pharmacies has not been publicly disclosed. We therefore estimate its financial profile using revenue per store benchmarks typical for pharmacy retail in Saudi Arabia. Store productivity varies meaningfully by location, brand strength and product mix.

While flagship urban pharmacies can generate in excess of SAR 8 to 10 million annually, smaller regional chains, which more closely reflect Kunooz’s network characteristics, typically operate at more moderate productivity levels.

Applying a conservative benchmark of approximately SAR 3 to 4 million in annual revenue per store to Kunooz’s reported network of roughly 90 locations implies estimated annual revenue in the range of SAR 250 million to SAR 350 million.

In the absence of publicly disclosed financial information, these figures should be regarded as illustrative estimates derived from sector benchmarking rather than confirmed company data.

Profitability for smaller pharmacy chains is generally lower than for national leaders due to weaker procurement leverage, limited private label penetration and higher relative operating costs.

Listed Saudi pharmacy operators provide a useful benchmark for the upper end of sector profitability. Nahdi Medical Company, the market leader, has historically generated EBITDA margins in the mid to high teens, while Al-Dawaa Medical Services Company typically operates in the low to mid teens range.

In comparison, mid-tier and regional chains commonly operate several percentage points below these levels. Based on sector benchmarks, Kunooz most likely operates within an EBITDA margin range of approximately 6 to 8% in a conservative case, implying estimated EBITDA of roughly SAR 15 million to SAR 25 million.

As with the revenue assumptions, these figures are indicative rather than definitive and reflect typical performance levels for sub-scale regional pharmacy networks in the absence of publicly disclosed financial information.

Despite these more modest margins typical of smaller retail operators, the Saudi pharmacy sector generally benefits from structurally favorable economics.

Profitability is supported by strong front-shop contribution from cosmetics and OTC products, limited reimbursement pressure, comparatively lower labor costs, and relatively higher per-store productivity.

As a result, margins tend to be more resilient and sustainable relative to Western markets, where retail pharmacy EBITDA margins typically average approximately 4–8%.

Implied Valuation and Benchmarking

Based on our estimates, United Pharmacies likely paid somewhere between 4x and 7x Kunooz's annual EBITDA — meaning the purchase price implies a valuation of roughly four to seven times the business's operating earnings. This is a typical range for smaller bolt-on acquisitions in Saudi pharmacy retail.

For context, the market's two dominant players trade at significantly higher multiples. Nahdi and Al-Dawaa are typically valued at 8x to 11x EBITDA, reflecting their scale, brand strength, and margin advantage.

The same premium is visible internationally — Walgreens and CVS have historically traded in a similar 9x to 11x range. The Kunooz deal sits below these benchmarks, which is expected.

Smaller regional chains with limited financial disclosure and weaker operating metrics attract a valuation discount relative to national leaders.

That discount is the price United Pharmacies pays for the uncertainty — but the strategic logic holds: the acquisition adds scale, expands distribution reach, and creates procurement efficiencies that would have taken years to build organically.

Concluding Thoughts

The Kunooz acquisition is expected to deliver value quickly, primarily because the two businesses already operate in the same product categories and geographies.

This is not a diversification play — it is a density play. Adding roughly 90–110 Kunooz locations to UPC's existing network creates immediate opportunities to consolidate supply chains, renegotiate supplier contracts from a stronger volume position, and reduce per-unit logistics costs across overlapping routes.

The margin upside is real but measured Kunooz likely enters the combined entity at an EBITDA margin of 6–8%. As integration progresses and procurement savings flow through, margins could reasonably move toward the high single digits or low double digits — not a transformation, but a meaningful step-up that compounds over time as the network scales further.

The broader signal is structural the Kunooz transaction is one data point in a longer consolidation cycle that is reshaping Saudi pharmacy retail. The market remains deeply fragmented, with thousands of independent operators and mid-tier chains that lack the purchasing power, digital infrastructure, and capital base to compete effectively against national leaders.

These operators are natural acquisition targets, and they tend to transact at significant discounts to listed peers — creating a repeatable opportunity for scale-driven consolidators to buy earnings cheaply, integrate efficiently, and close the valuation gap over time.

UPC's disclosed pipeline of two additional deals, one described as the largest in the sector's regional history, suggests the company is executing precisely this playbook.