The importance of maintaining valuation discipline in GCC M&A deals is exemplified in two notable transactions that took place in 2025.

In the first transaction, adherence to fundamental valuation principles appears to have limited downside risk and supported a more robust strategic rationale

By contrast, the second deal, which was priced at a significant premium due to its focus on AI and data centers, raises questions around the sustainability of such valuations.

While strategic sectors like AI and data infrastructure often command higher valuations, there is a growing concern that this premium may be driven more by inflated expectations rather than intrinsic value.

As investors in our region and around the world increasingly question whether we are experiencing another financial bubble destined to burst, the risk of future value erosion becomes even more pronounced.

Elm and Thiqah deal Overpriced or Justified?

As one of the largest deals in GCC of 2025 already took place, it becomes imperative to revisit the transaction early in 2026.

This transaction should create a national Information and Communication Technology leading entity combining Elm’s digital and cybersecurity expertise with Thiqah’s transformation services, expanding market reach, driving cross-selling, and supporting Saudi Arabia’s economic and technological goals.

Argaam Intelligence stresses in this analysis a critical aspect that warrants careful consideration; namely, the lack of comprehensive disclosure surrounding Thiqah’s financial position.

The absence of detailed financial information, including enterprise value metrics and net debt details, introduces a layer of opacity that complicates for M&A experts the valuation assessments and the real evaluation of potential synergies.

Addressing this gap in transparency in future M&A deals in the kingdom is essential for a thorough understanding of the deal’s strategic and financial implications, ensuring that all stakeholders can accurately assess the value created and the long-term success of the acquisition.

Elm is a publicly listed Saudi digital solutions and information technology provider (market cap ~ SAR 57 billion) with a broad portfolio spanning digital transformation, cybersecurity, data services, consulting, and business process outsourcing, and has a significant presence in government digital transformation projects.

Thiqah, based in Riyadh, is an ICT and business services firm specialising in smart technology solutions for business services, advisory services and managed solutions across both public and private sector clients.

Thiqah’s financial details and net debt position are not fully disclosed in public filings, therefore we can only we can only infer equity value. Enterprise Value is the most appropriate metric for assessing acquisition pricing as it reflects the true economic value of the businesses.

Relying solely on equity value in an M&A transaction can be misleading, as it fails to capture the company’s financial leverage and liquidity position.

Without clear visibility into enterprise value, stakeholders face difficulties in evaluating whether the purchase price aligns with the company's true economic worth.

Investors and experts rely on standardized metrics in M&A deals, mainly EV/Revenue, EV/EBITDA to benchmark transactions against sector norms and evaluate whether pricing is supported by future growth and profitability assumptions.

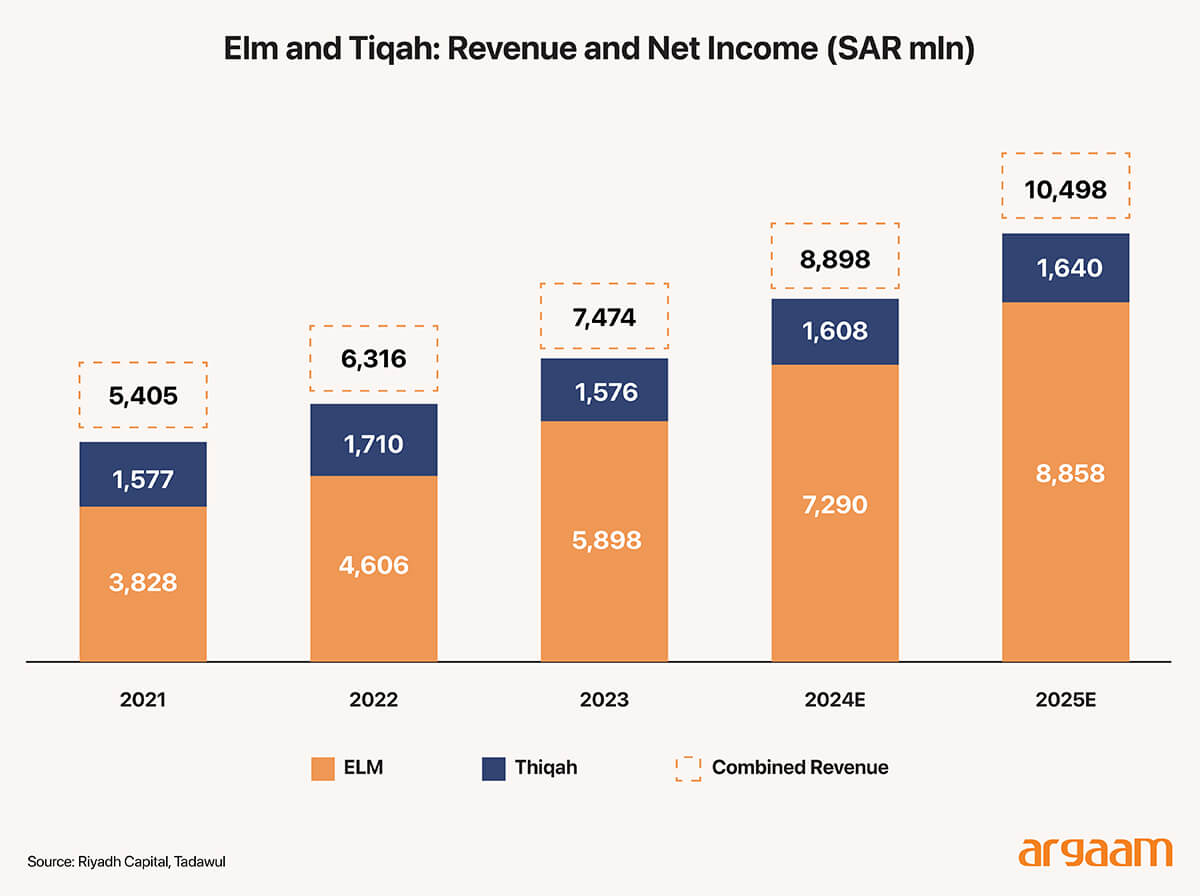

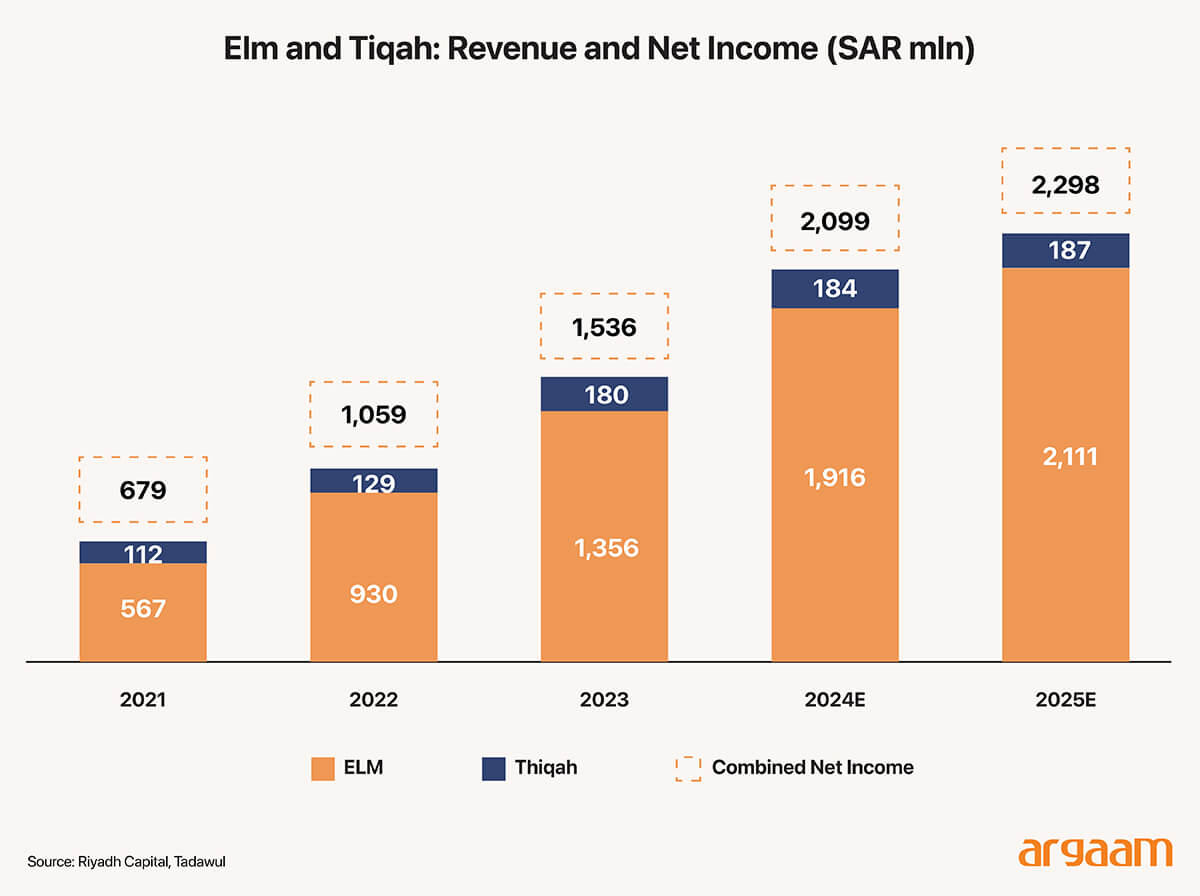

As a lot of these assumptions are inferred rather than confirmed, they introduce an additional layer of risk when assessing whether the SAR 170 million revenue contribution in Elm’s Q3 2025 results supports the implied valuation levels and long-term profitability profile.

(Click here to read the latest Elm’s announced financials/Q3 2025)

Thiqah’s Purchase Price in Context

We aim to evaluate whether the acquisition deal of Thiqah was priced fairly by independently assessing its valuation metrics in relation to industry benchmarks.

Based on the estimated equity value of SAR 3.4 billion, which serves as a rough proxy for the company's total enterprise value, and the FY23 revenue figure of approximately SAR 1.6 billion obtained from a reliable source, we can estimate the company's EV/Revenue multiple to be around 2.0x. This multiple provides a simple way to assess the company's valuation relative to its revenue.

This multiple remains fairly stable when updated for FY24, assuming a conservative revenue growth of about 2% from FY23 to FY24.

To give some context, companies in the broader IT services industry usually sell for a multiple of about 2 to 5 times their revenue, with the middle range typically around 2.5 to 3.5 times.

Higher valuations are usually given to businesses that grow quickly on their own (over 20% annually), have a lot of steady or repeatable income, retain more than 95% of their clients, have profit margins above 25%, and can convert earnings into cash efficiently—indicating they operate in an asset-light way.

Against this backdrop, and considering Thiqah’s scale, relatively modest growth profile, and lower margin characteristics the acquisition valuation appears to sit towards the lower end of prevailing sector benchmarks, suggesting the transaction was priced fairly.

⇢Valuation Limits Under Disclosure Gaps

It is important to note that the conclusions above remain constrained by the level of available disclosure. The absence of essential data—such as net debt and the precise total valuation of “Thiqa”—necessitates relying on indicative metrics rather than fully developed valuation models.

Even so, using these indicators (when benchmarked against sector standards) is sufficient to form an initial professional judgment about the reasonableness of the deal’s pricing, without claiming to reach a definitive or conclusive valuation.

✦When is a price considered fair?

Describing a deal as “fair” does not necessarily mean it is low risk, just as labeling another deal “expensive” does not make it strategically wrong.

The essential distinction lies in how much the paid price relies on:

●Existing, operational assets

●Versus future expectations that have yet to materialize

The greater the weight of unproven expectations in the valuation equation, the higher the inherent risk embedded in the deal.

G42 and Khazna Deal AI Acquisition at a Premium

The 2025 transaction between G42 and Khazna Data Centers represents one of the most significant infrastructure-led technology investments in the Middle East.

Under the deal, G42, Abu Dhabi’s leading AI and advanced technology group, acquired the remaining 40% stake in Khazna, a hyperscale-focused data centre platform originally formed as a joint venture between G42 and e& (formerly Etisalat Group).

Khazna is the region’s largest data centre operator and currently commands an estimated ~73% share of the UAE data centre market. Evaluating the deal by Argaam Intelligence, e& sold its 40% stake in Khazna to G42 for $2.2 billion, implying a total equity value for the company of approximately $5.5 billion.

While Khazna has not publicly disclosed net debt figures, it recently announced a $2.6 billion financing facility from First Abu Dhabi Bank (FAB). Additional debt facilities may exist. Assuming most or all of this debt is drawn and reflected on the balance sheet, enterprise value likely exceeds $8 billion.

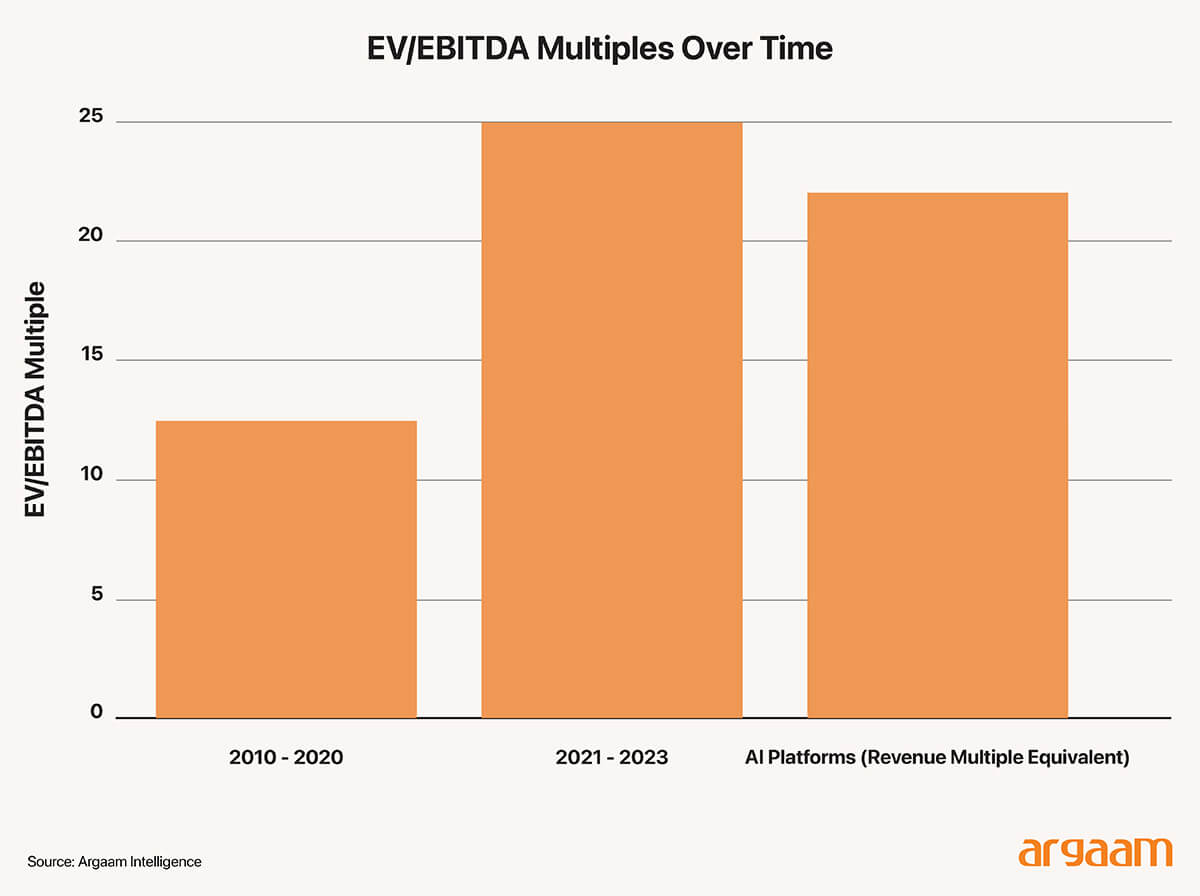

Over the past decade, the enterprise value (EV) of data centre companies was typically 10 to 15 times their earnings before interest, taxes, depreciation, and amortization (EBITDA).

This reflects stable cash flows as data centers are still being viewed as essential, foundational facilities that provide critical services similar to traditional utilities such as electricity, water, or gas.

From 2021–2023, hyperscale and growth-focused assets, such as data centres and cloud computing companies, saw multiples rise to 20–30x EV/EBITDA, driven mainly by demand and heightened Private Equity competition.

More recently, AI-optimized platforms are commanding revenue multiples in excess of 20x Revenues and price-per-MW metrics in the range between $8-$15m reflecting power scarcity (to operate energy-intensive data centres), future development capacity, and unique AI platform capabilities.

Looking at U.S. publicly listed peers, Equinix and Digital Realty are trading at enterprise values of approximately $90 billion (~10x EV/Rev, ~24x EV/EBITDA) and $70 billion (~12x EV/Rev, ~27 EV/EBITDA) respectively.

Note Adhering to disciplined valuation principles in GCC transactions helps investors and acquiring companies avoid overpaying for target firms, reduce the risks associated with mispricing, and secure attractive returns relative to the expected long‑term risks.

Equinix operates ~270 facilities globally with multi-gigawatt capacity (Equinix fillings), while Digital Realty operates 300+ facilities globally, also with multi-gigawatt capacity.

Direct comparisons are challenging because exact MW per facility are not publicly disclosed, and Khazna is currently more regional in focus.

Comparable M&A transactions in the data-center sector include: ●Vantage Data Centers: $9.2 billion minority equity raise (~35 campuses with total planned & existing capacity >2.6 GW) (Vantgae Data Centres) ●AirTrunk: ~$16.1 billion acquisition (acquired by a consortium led by Blackstone), ~30x EBITDA (~11 hyperscale data centers across Asia Pacific, ~800 MW+ committed capacity (Airtrunk)

On a simple capacity-weighted basis, AirTrunk’s ~$16 billion acquisition translates to roughly $11.2 million per MW of platform capacity ($16B / 1.44 GW). By comparison, assuming Khazna’s enterprise value exceeds $8 billion, this maps to approximately $12 million per MW ($8B / 0.65 GW).

Note On a simple "capacity-weighted basis" refers to a method of measurement or calculation where each data point—such as a valuation, price, or index—is weighted directly by the capacity associated with it, without applying additional adjustments or complex weighting schemes.

In this context, capacity typically represents the amount of power (e.g., in megawatts) that a power plant, vessel, or platform can generate or hold.

While this analysis is illustrative and does not adjust for other valuation drivers such as revenue mix, contract structure, or profitability, it indicates that Khazna is effectively priced at a premium.

In our view, this premium carries inherent risk, as it may be driven by optimistic expectations of future growth that are inherently speculative given the rapid and unpredictable evolution of AI technology.

It is worth noting that concerns are growing about the hundreds of billions of dollars Big Tech has pledged to spend on AI infrastructure.

Concluding thought:

Maintaining disciplined valuation practices in GCC deals helps investors and corporate acquirers to avoid overpaying for targets, mitigate risks associated with mispricing, and secure attractive risk-adjusted returns over the long run.

More this Weekend

Riyadh vs Dubai Real Estate: A Comparative Analysis of Demographic-Driven Investment Risk-Return Profiles

Riyadh and Dubai do represent two fundamentally distinct real estate investment models, differentiated by their demographic compositions and resulting risk-return characteristics. Permanent citizen populations generate predictable, compounding housing demand with lower volatility.

Blending Saudi Philanthropy with Fiscal Strategy to Reduce National Debt

Saudi Arabia has the opportunity to redefine the role of its historic or specialized charity funds conceptually and pragmatically. Through the conceptual framework, we redefine for charity outcomes as ‘assets’ focused on value creation and long-term benefits to society without profit motives.

Analyzing Overproduction Trends and Their Impact on the Petrochemical Industry

Saudi Arabia's petrochemicals and cement industries are currently exhibiting signs of overcapacity, which may indicate a potential disconnect between supply and demand. In the petrochemicals sector, recent financial performance has transitioned toward substantial losses, reflecting structural challenges related to excess production.