|

Saudi Arabia's mobility sector is currently experiencing a pivotal phase, characterized by shifts in business models and market dynamics. While established traditional car rental companies continue to maintain stable revenue streams, the financial sustainability of fleet ownership is increasingly challenging.

🚘 Why Fleet Ownership is Becoming a Liability

Lumi Rental Co., Saudi Arabia's largest listed rental company, reported net profit of SAR 180.3 million in 2024, an increase of 12% y/y compared to SAR 160.6 million in 2023 (Argaam - Lumi Rental Co. 2024 Financials, 2025).

📊

Lumi & Theeb Profitability Trends (2023 vs 2024)

Theeb Rent a Car demonstrated stronger profit growth momentum in its nine-month results, reporting SAR 131.54 million in net profit (January-September 2024), up 23.5% from SAR 106.54 million in the same period of 2023. The critical insight lies under this headline figure: profit growth was primarily driven by a 39% surge in long-term lease revenues, while short-term rental revenue actually declined 3% y/y (Argaam - Theeb Rent a Car 9M 2024 Financials, 2024)—a defensive shift away from high-margin daily rentals toward lower-margin corporate lease contracts for margin stability. This strategic repositioning does reveal underlying weakness in the core rental business model. Both companies face identical structural headwinds: persisting SAIBOR pressures at approximately 5.5-6% translating to fleet financing costs of 8-9% annually, which directly compress net margins while capping growth potential. So, we believe that this business model of car rentals is profitable and generates stable cash flow, making it attractive to dividend-focused investors. However, growth is capped by capital intensity, rising financing costs, and the defensive shift toward long-term lease contracts. These are mature, low-growth models suited to conservative institutional investors—not growth or venture investors.

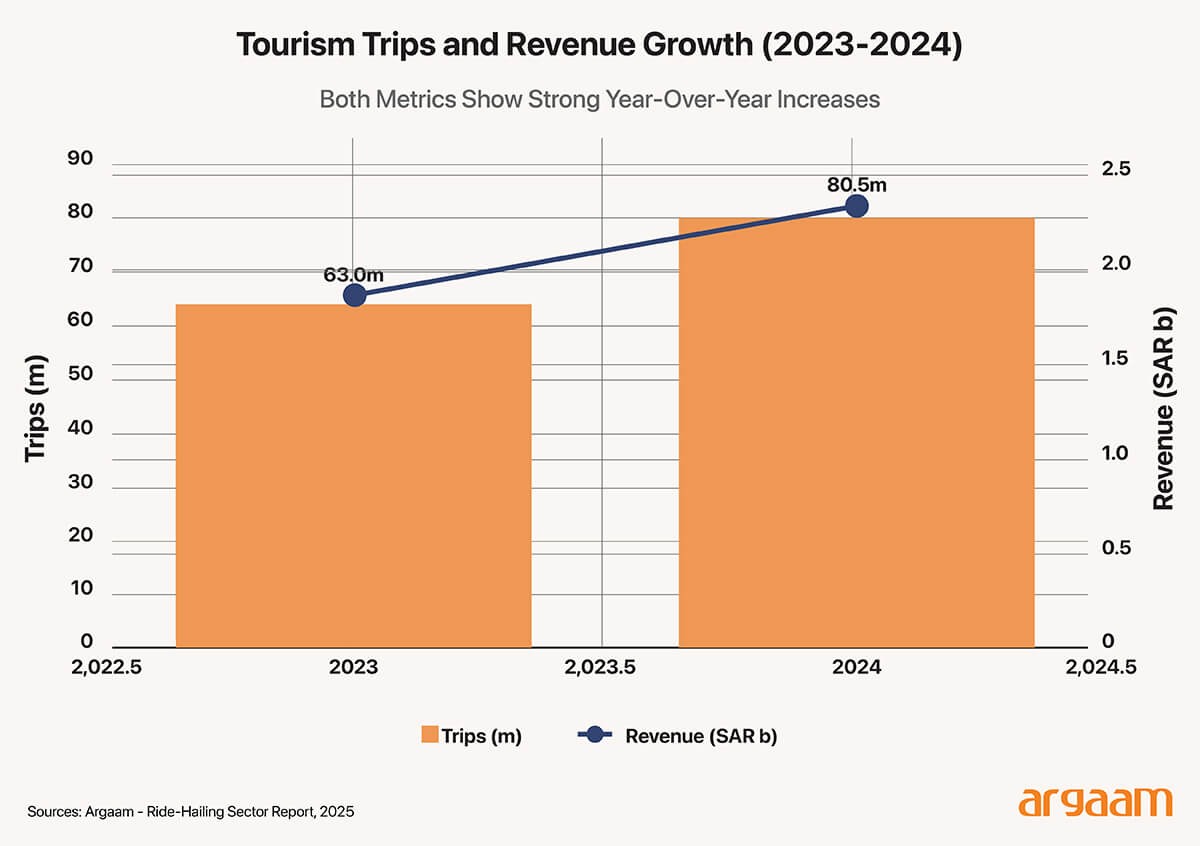

Ride-hailing's volume trap On the surface, ride-hailing do look unstoppable. The Transport General Authority (TGA) reported 80.5 million trips completed in 2024, up 26% y/y from 63.9 million in 2023 (Argaam - Ride-Hailing Sector Report, 2025). Sector revenue reached SAR 2.3 billion, an increase of 22% y/y, and the number of registered drivers grew to approximately 332,100 (Argaam - Ride-Hailing Sector Report, 2025).

But here lies the critical economic flaw: this is a volume game with insufficient unit economics. Dividing SAR 2.3 billion in sector revenue by 80.5 million trips yields a revenue-per-trip of only SAR 28.6. Assuming a 20-25% take rate (the global standard for Uber/Careem), platforms keep approximately SAR 5.7-7.2 per trip. After server costs, payment processing, driver incentives, and corporate overheads, net margins approach single digits. It’s important to note that larger operations can be more profitable, while market concentration becomes harder to maintain as markets become more fragmented and competitive. With 45 licensed digital ride-hailing platforms operating in Saudi Arabia, no single player dominates the market. Uber and Careem have significant market presence, however they do not publish Saudi-specific financials— Careem's figures are consolidated into Uber's accounts on a MENA-wide basis (Following Uber's acquisition of Careem in March 2020, consolidated MENA-wide reporting - Uber Investor Relations, 2025), making Saudi-specific financial analysis difficult. Jeeny, which markets itself as the fastest-growing ride-hailing app in the MENA region (OpenVC.app - Jeeny Investor Profile, 2025), operates as one of MENA's core platforms.

Why asset-light car sharing offers superior ROI Ejaro, is a peer-to-peer car rental platform founded in 2019 that raised SAR 12.3 million (USD 3.3 million) in a Pre-Series A round in January 2024 (Waya Media - Ejaro Raises USD 3.3 Million in Pre-Series A Funding Round, 2024). What makes Ejaro fundamentally different from Lumi and Theeb is clear: Ejaro owns zero vehicles. The platform acts as a marketplace where individual car owners list their vehicles for daily or hourly rental. Ejaro takes a commission (estimated 20-25%) and the host (car owner) retains the bulk of revenue. The implications for return on invested capital (ROIC) is indeed staggering. While Lumi spends billions of riyals on fleet acquisition and carries billions more in debt, Ejaro's SAR 12.3 million capital is for developing technology, forming insurance partnerships, marketing, and ensuring compliance, not for buying or replacing cars or physical assets. Ejaro's commission structure translates to gross margins approaching 20-30% before operating costs. However, the decisive advantage lies in capital efficiency: Ejaro generates these margins with zero capex and zero fleet debt, whereas Lumi and Theeb must continuously finance expansion of fleet, creating debt obligations that substantially erode net returns on invested capital. Each new host on the platform adds inventory at zero cost to the company.

Important Clarification Platform gross margins (ekar, Ejaro) reflect commission revenue before platform operating expenses (customer acquisition, technology, compliance). Fleet operator figures represent net margins after all operating costs and capital charges. While the comparison shows asset-light platforms achieve higher commission-level margins, true net profitability does vary by company and market conditions.

A frequently overlooked advantage of Ejaro is its strategic partnerships with Saudi Arabia's leading insurance companies. Rather than building insurance capabilities in-house, Ejaro has partnered with Tawuniya (a major insurance company in Saudi Arabia), as well as Najm and Absher, thereby transferring liability risk from the platform to established insurers—a massive de-risking for early-stage investors.

ℹ︎

Future Signals (2025–2027)

● P2P regulatory trends ● Evolution of financing rates (SAIBOR) ● Market concentration in ride‑hailing ● Consumer behavior (ownership vs. sharing) As a concluding note, the race for Saudi mobility leadership is not being won by who owns the most cars. It is being won by who owns the technology, the marketplace, and the unit economics. This conclusion aligns with the findings of the report “Which Sectors Are the Most Competitive in the Saudi Market?” based on the Herfindahl–Hirschman Index (HHI), which showed that market structure and the degree of concentration often determine the boundaries of competition even before firms’ behavior does. In this context, the mobility‑sector analysis confirms that differences in business‑model outcomes are not driven solely by operational efficiency, but also by the structural characteristics of the market and its capacity to absorb competition and generate sustainable returns on capital. |

|

|

|

|

|

Argaam.com Copyright © 2026, Argaam Investment, All Rights Reserved |