Despite the growing visibility of buy now, pay later (BNPL) options in Saudi Arabia’s offline retail landscape, the model is unlikely to pose a structural challenge to the credit cards’ market.

The apparent expansion of BNPL offline, with some unofficial ratios estimated at 40% of all BNPL transactions, reflects neither superior payment efficiency nor a wholesale shift in consumer preference, but rather its ability to reach segments that have historically sat outside the core credit card market.

While platforms such as Tamara have made inroads among younger and first-time credit users, their growth remains shaped by tighter regulatory constraints, narrower monetisation channels, and balance-sheet-intensive economics (since the BNPL providers depend heavily on managing and using a lot of its own money or assets—like loans or credit they give out—on their own balance sheet).

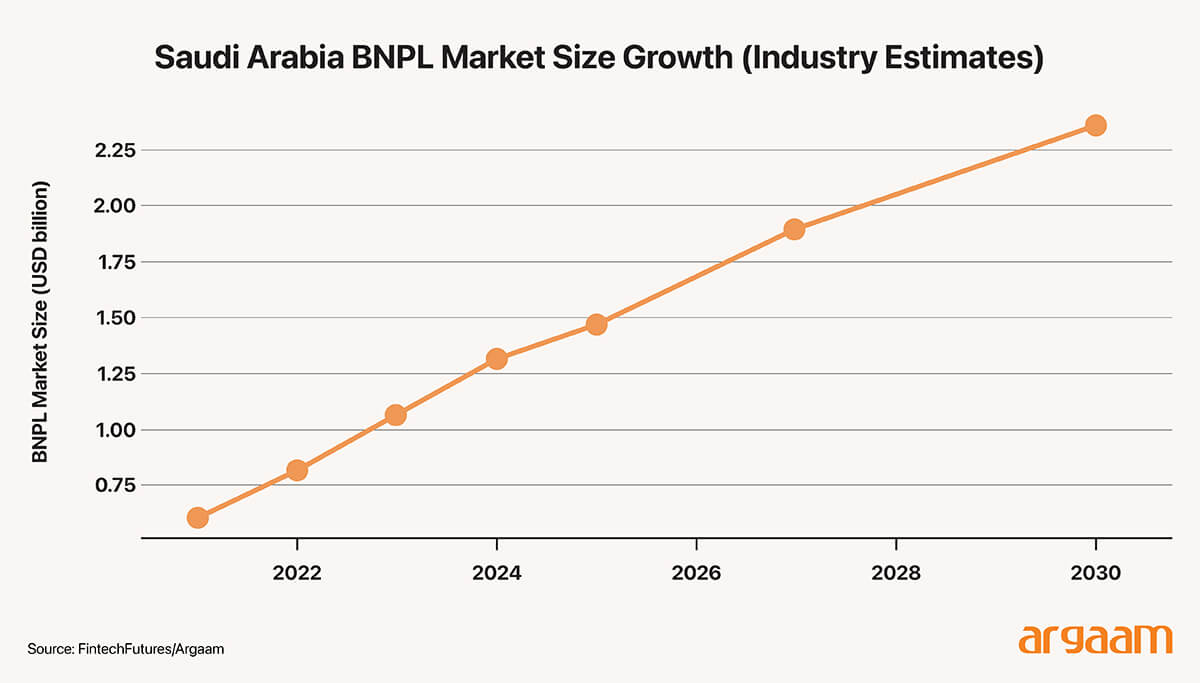

Yet the perception that BNPL is encroaching on credit card territory is understandable. Industry research indicates that the BNPL payment market in Saudi Arabia is on track to reach approximately US$1.48 billion by the end of 2025, following several years of robust growth.

Historical estimates suggest the sector grew at a ~23% compound annual rate between 2021 and 2024, and it is forecasted to continue expanding at around a 9.7% CAGR through 2030, potentially reaching roughly US$2.36 billion by the end of the decade.(Fintech futures,2025)

Also, the model’s growing offline presence — particularly in discretionary retail categories such as electronics, fashion and lifestyle goods — has further reinforced the impression that BNPL is gaining ground in areas traditionally associated with credit cards.

Coexistence under differentiated constraints is the intended outcome

Before we delve deeper into our analysis, we will review the regulatory system in the kingdom to understand the different modes in which both BNPL and credit cards operate. Any assessment of BNPL’s competitive impact must begin with regulation.

In Saudi Arabia, credit cards operate within a mature and internationally aligned regulatory framework that permits consumer-facing charges, flexible credit limits, and revolving balances subject to banks’ internal risk models.

Card issuers are allowed to price for risk through monthly rate, annual fees and penalty structures, enabling credit cards to function as scalable, multi-purpose credit instruments across virtually all consumption scenarios.

BNPL, by contrast, is governed under a markedly tighter perimeter. Saudi regulators classify BNPL explicitly as a financing activity rather than a payment service, subjecting providers to licensing requirements, credit exposure limits and leverage caps.

Consumer-facing fees are prohibited, credit limits are constrained, and product design remains closely supervised. These rules are not incidental; they reflect an explicit policy choice to prevent short-term instalment products from evolving into lightly regulated substitutes for revolving credit.(SAMA,2023)

The result is a structural asymmetry. While credit cards are designed to absorb risk across a diversified revenue base, BNPL providers in Saudi Arabia must operate with narrower monetisation channels and balance-sheet exposure that scales directly with usage.

(Scales directly with usage" means that the monetization—i.e., the revenue generated by BNPL providers—varies proportionally with the amount of consumer activity or transactions.)

means that when Buy-Now-Pay-Later (BNPL) companies grow, their increased sales don't just make their existing business more efficient (which is what operating leverage refers to).

Instead, growth requires them to spend more money upfront to fund new purchases and to set aside more funds as a safety net in case some customers don't pay back.

This regulatory architecture shapes not only BNPL’s economics, but also the boundaries within which it can compete.(SAMA,2025)

Importantly, this asymmetry does not imply regulatory hostility toward BNPL. Rather, it signals a calibrated approach: allowing BNPL to expand as a controlled, scenario-specific credit tool while preserving credit cards as the systemically dominant infrastructure for consumer credit.

Within this framework, substitution is neither assumed nor encouraged; coexistence under differentiated constraints is the intended outcome.

|

Dimension |

Credit Cards (Saudi Arabia) |

BNPL (Saudi Arabia) |

|

Regulatory classification |

Consumer credit/ payment instrument |

Financing Activity |

|

Licensing Requirement |

Licensed banks |

Licensed finance companies |

|

Consumer-facing fees |

Permitted (interest, annual fees, penalties) |

Largely prohibited |

|

Interest / profit charging |

Allowed (interest-based) |

Restricted (Shariah-Complaint structures only) |

|

Credit limit determination |

Bank internal risk models |

Explicit regulatory caps |

|

Leverage/ capital constrains |

Subject to bank capital rules |

Explicit leverage limits |

|

Revenue structure |

Diversified (consumer + merchant) |

Primarily merchant-funded |

|

Balance sheet exposure |

Indirect, revolving credit |

Direct, usage-linked exposure |

|

Product flexibility |

High (multiple use cases) |

Low to moderate |

|

Regulatory objective |

Systemic consumer credit infrastructure |

Controlled, scenario-specific credit access |

Source: Argaam

As a specific example, Tamara explicitly states that it does not impose any late payment fees on overdue installments, in line with its Shariah-compliant design.

While delayed payments may lead to account suspension or adverse credit reporting, no monetary penalty is charged for lateness.(Tamara,2025)

By contrast, credit cards issued by licensed banks operate under a materially different cost structure.

According to the official terms and conditions of Al Rajhi Bank’s signature credit cards, cardholders are subject to annual fees, monthly profit charges (2.5%) on outstanding balances, foreign transaction fees, cash withdrawal fees, minimum payment requirements, and other service-related charges.

These charges form an integral part of the credit card business model and directly affect the cost of delayed or partial repayment. (Alrajhi Bank,2025)

The regulatory constraints facing BNPL providers become more consequential once their two-sided market dynamics are taken into account — particularly in offline retail.

Unlike credit cards, which operate on a largely one-sided adoption model once issued, BNPL platforms must simultaneously attract consumers and merchants to sustain usage.

BNPL’s Tactical Approach to Market Growth

This dynamic helps explain why offline BNPL expansion tends to concentrate in specific discretionary categories — such as electronics, fashion and lifestyle retail — rather than diffuse evenly across everyday consumption.

These categories offer higher ticket sizes and clearer incentives for instalment use, allowing BNPL providers to justify merchant fees despite uneven coverage. By contrast, in low-value, high-frequency transactions, the two-sided coordination problem becomes more acute, favouring payment instruments with near-universal acceptance.

In this context, BNPL’s offline growth should be understood less as a direct assault on credit card dominance and more as a targeted attempt to establish localised pockets of viability.

Instead of trying to challenge or replace credit card dominance across the entire retail landscape, BNPL mechanisms focus on establishing strong footholds in particular sectors and markets.

Without sufficiently dense merchant networks, offline BNPL struggles to translate visibility into sustained usage — reinforcing the structural limits identified in both regulation and firm-level financials.

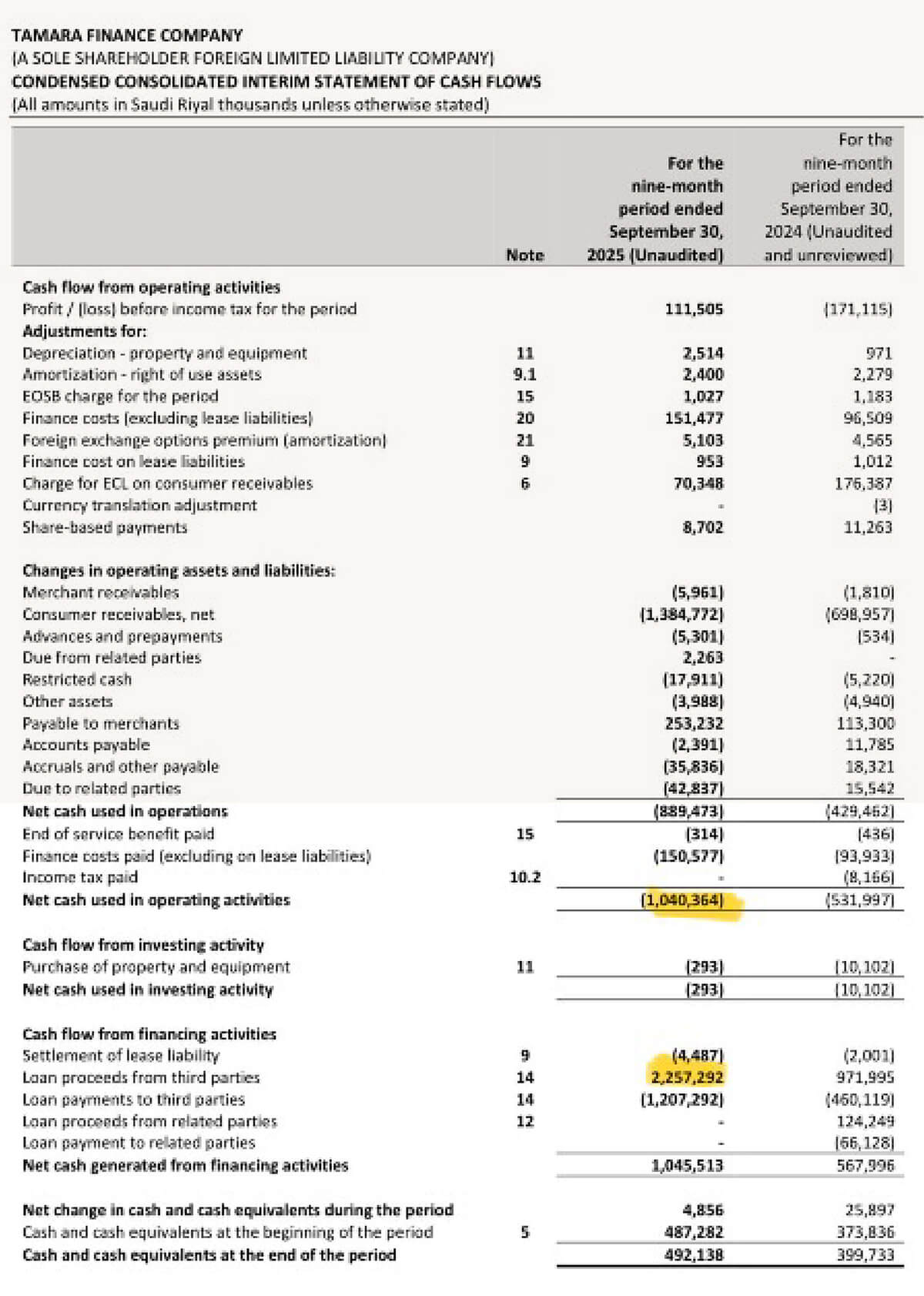

The structural constraints facing offline BNPL are clearly reflected in the financials of Tamara. A comparison between the first and third quarters of 2025 highlights a pattern of rapid balance-sheet expansion accompanied by persistent capital intensity, reinforcing the limits identified at the regulatory and market-structure levels.(Tamara,2025)

Tamara's financial numbers show that their business is growing quickly, especially in terms of the amount of money they are managing or lending.

However, this rapid growth requires a lot of money and resources to support it, which makes the business expensive to run. These challenges are not just internal but also come from rules and market conditions outside the company.

So, Tamara is expanding fast, but it's doing so in a way that is costly and limited by regulations and how the market is set up.

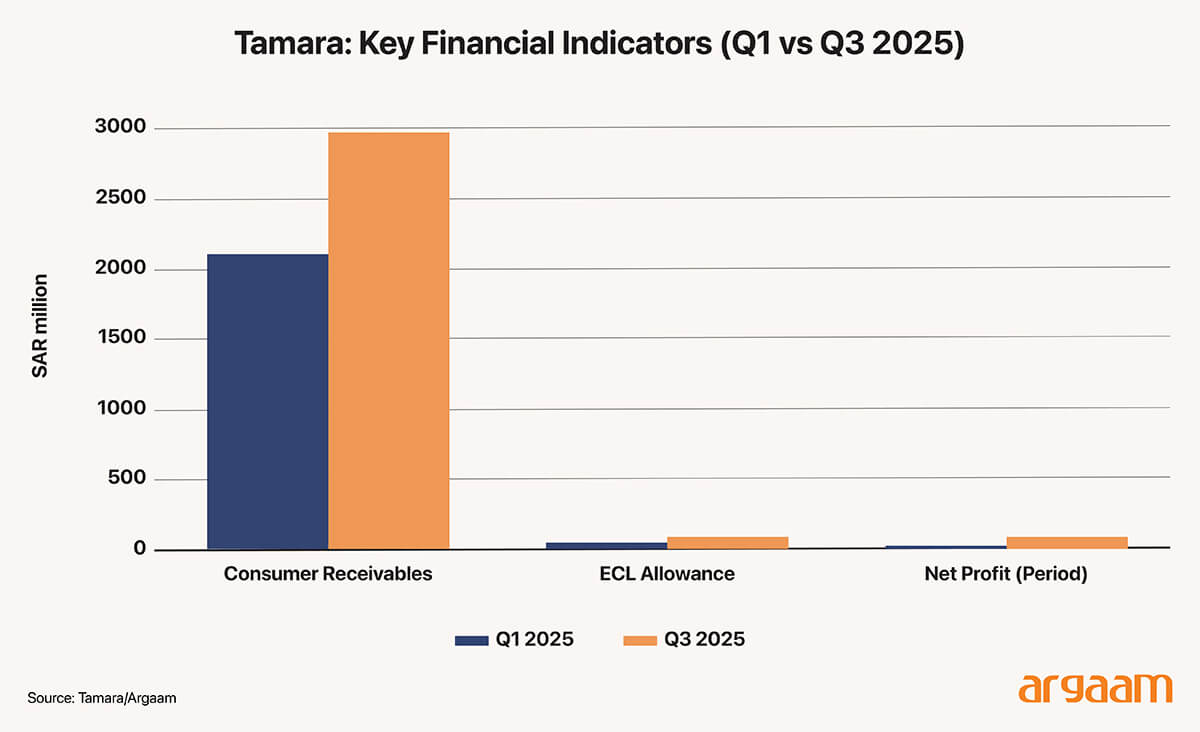

Between Q1 and Q3 2025, Tamara’s net consumer receivables increased from approximately SAR 2.1 billion to SAR 3.0 billion, representing growth of over 40% within nine months.

This growth can be analysed when understanding the inner financial works of any BNPL provider: when customers make more BNPL purchases, the financial risk for the lender grows directly with those transactions, rather than just acting as a temporary or off-the-record arrangement.

Essentially, each new BNPL transaction increases the lender’s actual financial commitments upfront, rather than just being a behind-the-scenes facilitation of payments.

Unlike card networks, where incremental usage does not materially expand issuer balance sheets, BNPL growth at Tamara requires continuous funding to support receivables.

As volumes rise, so too does the company’s need for external financing and liquidity management. Credit risk has scaled alongside receivables.

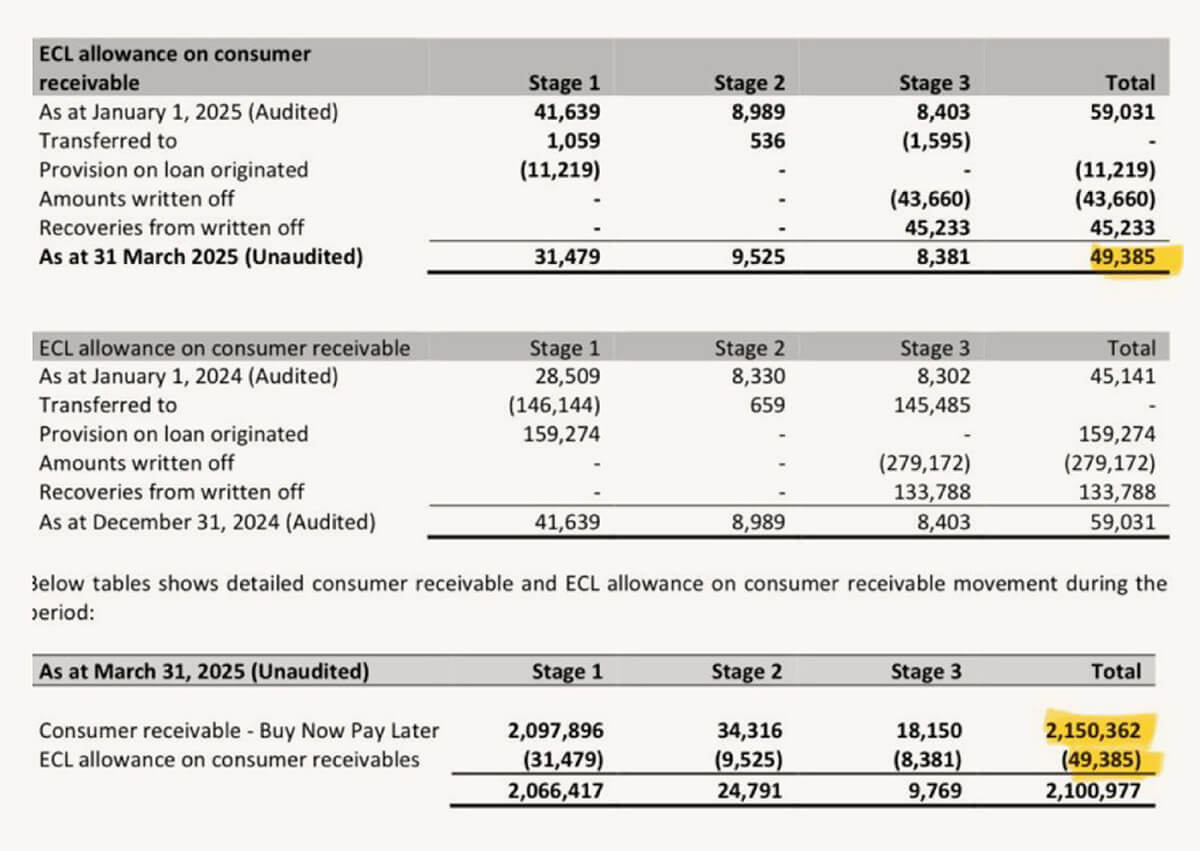

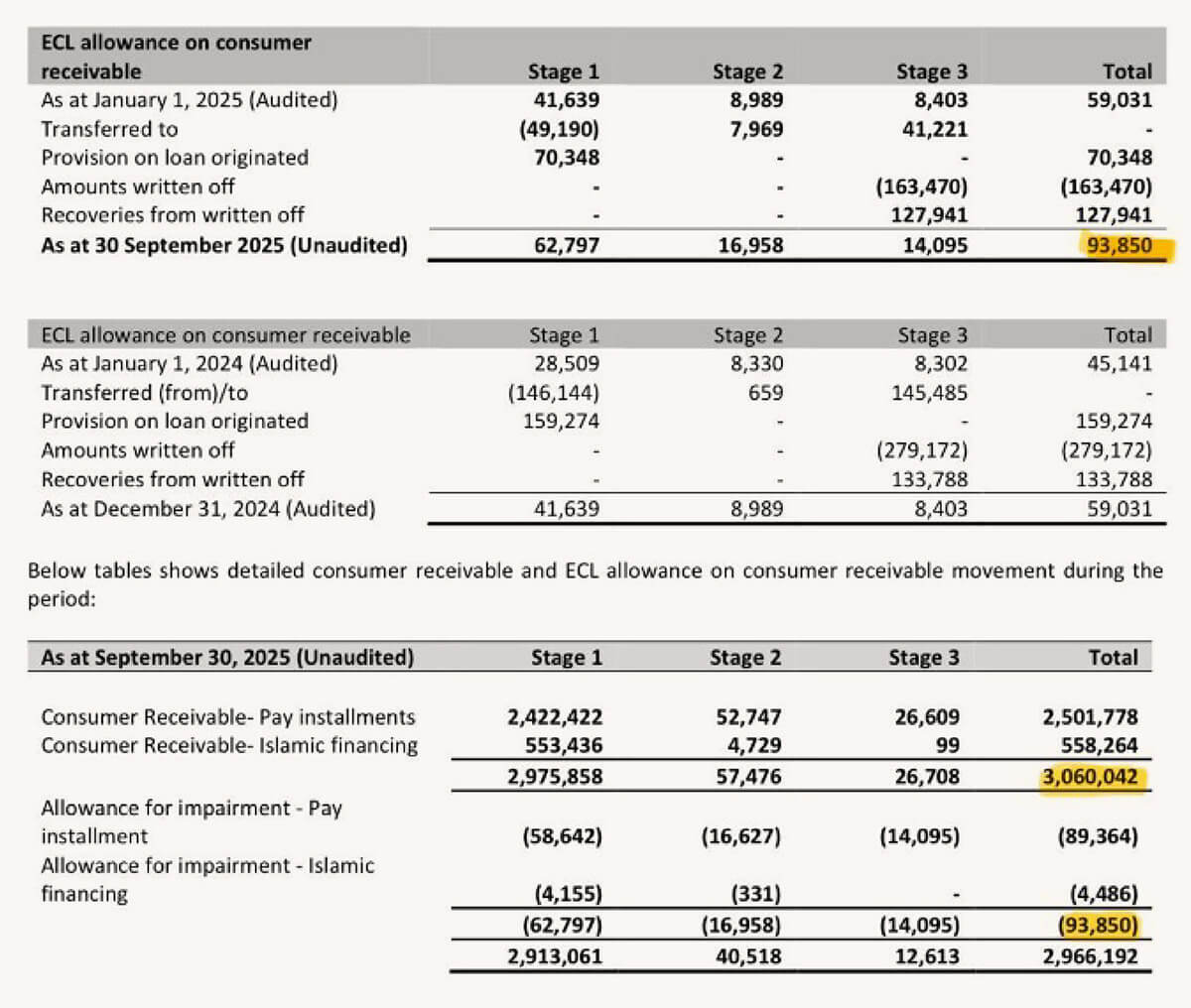

Tamara’s expected credit loss (ECL) (which’s unpaid debt) allowance increased from roughly SAR 49 million in Q1 to nearly SAR 94 million by Q3, raising the ECL coverage ratio from around 2.3% to above 3%.

Consumer uptake drives merchant acceptance, while merchant coverage in turn determines whether BNPL is perceived as a viable everyday payment option.

This interdependence is especially pronounced in physical retail environments. Offline transactions are less forgiving of friction than online checkout flows, and consumer willingness to choose BNPL at the point of sale depends heavily on habitual availability rather than active consideration.

If BNPL is not consistently accepted across commonly visited stores, its value proposition weakens rapidly, reducing both usage frequency and merchant incentive to maintain integration.

As a result, scale in offline BNPL is not merely an advantage but a precondition. Merchant acquisition costs are incurred upfront, while consumer usage materialises only if acceptance reaches sufficient density within a given retail ecosystem.

Where this threshold is not met, BNPL platforms face a negative feedback loop: limited acceptance suppresses consumer usage, which in turn undermines the commercial rationale for merchants to continue offering the option.

This dynamic helps explain why offline BNPL expansion tends to concentrate in specific discretionary categories — such as electronics, fashion and lifestyle retail — rather than diffuse evenly across everyday consumption.

These categories offer higher ticket sizes and clearer incentives for instalment use, allowing BNPL providers to justify merchant fees despite uneven coverage.

By contrast, in low-value, high-frequency transactions, the two-sided coordination problem becomes more acute, favouring payment instruments with near-universal acceptance.

In this context, BNPL’s offline growth should be understood less as a direct assault on credit card dominance and more as a targeted attempt to establish localised pockets of viability.

Without sufficiently dense merchant networks, offline BNPL struggles to translate visibility into sustained usage — reinforcing the structural limits identified in both regulation and firm-level financials.

The structural constraints facing offline BNPL are clearly reflected in the financials of Tamara. A comparison between the first and third quarters of 2025 highlights a pattern of rapid balance-sheet expansion accompanied by persistent capital intensity, reinforcing the limits identified at the regulatory and market-structure levels.(Tamara,2025)

Between Q1 and Q3 2025, Tamara’s net consumer receivables increased from approximately SAR 2.1 billion to SAR 3.0 billion, representing growth of over 40% within nine months.

This expansion closely tracks transaction growth, indicating that BNPL usage translates almost one-for-one into on-balance-sheet exposure rather than off-balance-sheet facilitation.

Unlike card networks, where incremental usage does not materially expand issuer balance sheets, BNPL growth at Tamara requires continuous funding to support receivables. As volumes rise, so too does the company’s need for external financing and liquidity management.

Credit risk has scaled alongside receivables. Tamara’s expected credit loss (ECL) allowance increased from roughly SAR 49 million in Q1 to nearly SAR 94 million by Q3, raising the ECL coverage ratio from around 2.3% to above 3%.

This trend suggests that while underwriting models may improve incrementally, credit losses have not been structurally decoupled from growth.

For offline BNPL in particular, this linkage is significant. As transaction volumes increase across physical retail environments, risk dispersion remains limited, and provisioning requirements rise proportionally — constraining operating leverage.

On the income statement, Tamara reported improved profitability over the same period, with net profit reaching approximately SAR 92 million for the first nine months of 2025, compared with SAR 26 million in Q1 alone. However, this accounting improvement has not translated into operating cash generation.

Over the nine-month period, Tamara recorded negative operating cash flow exceeding SAR 1 billion, driven primarily by receivables growth.

To sustain expansion, the company relied heavily on external funding, raising over SAR 2.2 billion in new long-term financing, while simultaneously servicing existing obligations.

This divergence between reported profitability and cash flow underscores a core characteristic of the BNPL model: growth remains capital-dependent rather than self-financing.

Taken together, these figures illustrate that Tamara’s expansion has been achieved through balance-sheet deepening rather than structural efficiency gains.

In offline settings — where merchant acquisition costs are higher and transaction frequency is less predictable — this model becomes increasingly sensitive to scale thresholds.

Without sufficiently dense merchant networks and sustained consumer usage, incremental growth risks amplifying funding and provisioning pressures faster than it generates economic returns.

Far from enabling frictionless substitution of credit cards, Tamara’s financials point to a model that converges toward traditional consumer finance in its capital requirements, even as its consumer-facing experience remains distinct.

Taken together, the evidence suggests that BNPL’s offline expansion in Saudi Arabia is highly context-dependent rather than universal. In everyday, low-value and high-frequency transactions — such as groceries, transport and routine services — credit cards and contactless payment instruments remain structurally advantaged.

Their near-universal acceptance, minimal transaction friction and revolving credit functionality make them better suited to habitual offline consumption, where speed and coverage matter more than instalment flexibility.

BNPL, by contrast, performs best in selective offline scenarios where transaction values are higher and instalment use is more salient, such as electronics, fashion and lifestyle retail.

Even within these categories, however, expansion is constrained by regulatory limits on credit exposure and funding leverage.

As the financials of leading providers such as Tamara illustrate, growth in physical retail translates directly into balance-sheet intensity rather than scalable operating leverage, placing a natural ceiling on the pace and breadth of offline rollout.

Crucially, the offline user segments most responsive to BNPL differ from the core customer base of credit cards. Industry research indicates that BNPL adoption in Saudi Arabia is concentrated among younger consumers, digital-native users and first-time credit participants, many of whom do not yet meet traditional card eligibility thresholds. (Global Data,2025)

This cohort is better characterised as a pool of potential future cardholders rather than existing users being displaced. As such, BNPL’s offline traction reflects early-stage credit inclusion more than competitive substitution.

Viewed through this lens, BNPL’s role in Saudi Arabia’s offline economy is less about challenging credit card dominance and more about complementing a rapidly modernising financial ecosystem.

By extending controlled, short-term credit to under-served segments and discretionary use cases, BNPL broadens payment choice without undermining the infrastructure of traditional consumer credit.

Its greater competitive potential therefore lies not in offline displacement, but in online commerce, where frictionless integration and behavioural effects can be deployed at scale.