Market structure and competition analysis are crucial for evaluating the competitiveness of economic sectors. Since the assessment of competition requires accurate quantitative tools, the Herfindahl–Hirschman Index (HHI) stands out as one of the most important global benchmarks for measuring market concentration.

This report provides a comprehensive overview of the index, its calculation methodology, advantages and disadvantages, along with practical applications across eight sectors of the Saudi market for the period 2020–2024.

ℹ︎

What has changed in reading competition?

● Expansion of the Saudi market ● Increase in mergers ● Quiet rise in concentration within some sectors

The result:

Assessing competition is no longer a theoretical exercise, but a gateway to understanding: ● Pricing ● Entry opportunities ● Monopoly risks

1)What is the HHI? The Herfindahl–Hirschman Index (HHI) is a statistical measure used to gauge market concentration by summing the market shares of all companies within a sector.

It is a fundamental analytical tool for regulatory authorities in the US and Europe to study competition and assess the impact of mergers and acquisitions. HHI=∑(Si)2 Si represents the market share of each company.

ℹ︎

Why do we use the HHI as an analytical lens?

Because the index doesn’t answer who is the largest?

But rather how much space is left for everyone else? ● It measures the concentration of market power ● It is sensitive to structural changes ● It is used globally by regulators

Example: If a market has three companies with shares of 30%, 40%, and 30%, then: HHI = (302) + (402) + (302) = 900 + 1600 + 900 = 3400

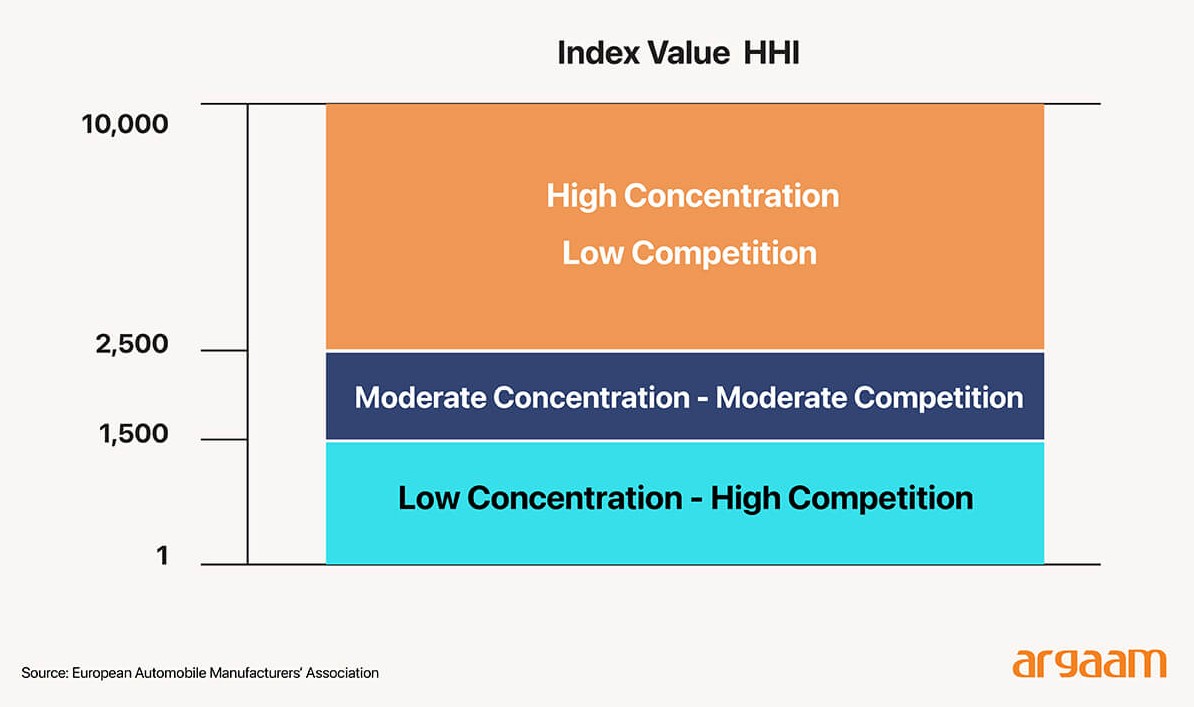

● The index gives more weight to larger companies, making it sensitive to increases in the dominance of one or more firms. ● The minimum value is 1 point, occurring when the market is evenly distributed among 100companies with 1% each. ● The maximum value is 10,000 points, representing a fully monopolized market.

2) Implications of the Index Value

3) Methodology for Calculating Market Share

Given the diversity of economic sectors in Saudi Arabia, the most appropriate measure of market share was used for each sector, reflecting the actual size of activity:

Sector

Market Share Measure

Reason for Choice

Companies Included

Cement

Sales Volume

Sales reflect the actual business size

All 17 cement companies

Motor insurance

Gross Written Premiums

Global standard for company size

All 24 listed insurers except Saudi Reinsurance

Banking

Total Assets

Reflects real financial size and strength

All 10 listed banks

Healthcare

Revenues

Reflects operational size and beneficiaries

10 listed healthcare companies

Supermarkets & Hypermarkets

Revenues

Sector activity depends on sales volume

Al Othaim, Farm Superstores, BinDawood, Savola Group (retail), and Lulu Retail

Milling

Revenues

Sector activity depends on sales volume

First Mills, Fourth Milling, Arabian Mills, and Modern Mills

Medical Insurance

Gross Written Premiums

Global standard for company size

All 21 listed insurers except Saudi Re, LIVA, CHUBB Arabia, and Wataniya Insurance

Telecom (Mobile Services Only)

Revenues

Global regulatory standard

stc, Etihad Etisalat, Zain KSA (mobile only)

Note: Revenues were calculated from Saudi operations only for companies with international exposure.

4) Why the HHI?

1)Measuring Competition Strength: HHI helps determine the competitiveness of a sector. Closely matched market shares indicate high competition, while concentration among few firms indicates weak competition.

2) Assessing Monopoly Risk: Regulators use the index to identify sectors vulnerable to monopolistic practices or price manipulation.

3)Understanding the Impact of Mergers & Acquisitions: HHI is used before and after mergers to evaluate the effect on competition, guiding regulatory approval or rejection.

Example: If two companies with 30% and 20% market shares merge, the index may increase significantly, signaling potential market risk.

4)Supporting Investor and Policymaker Decisions: For investors: Provides insight into risk and potential returns.

For policymakers: Identifies the need for regulatory measures or market structure review.

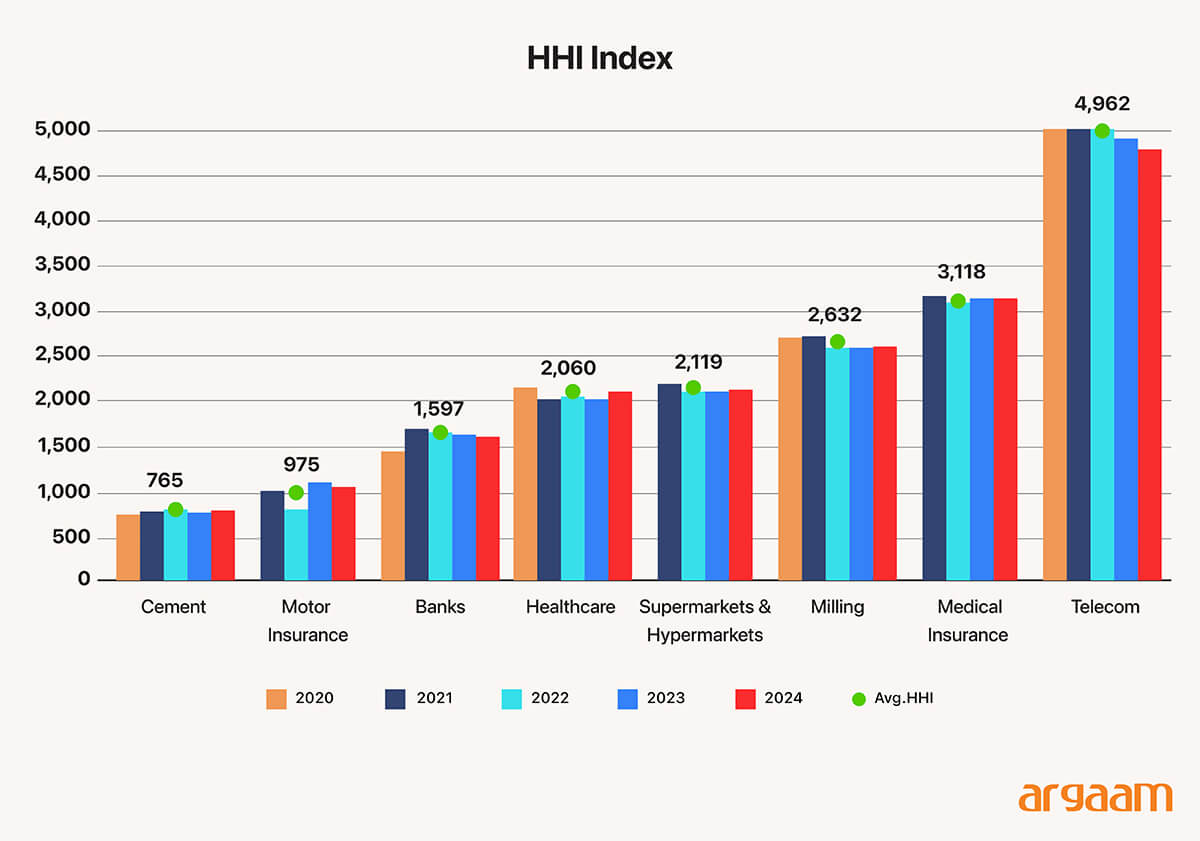

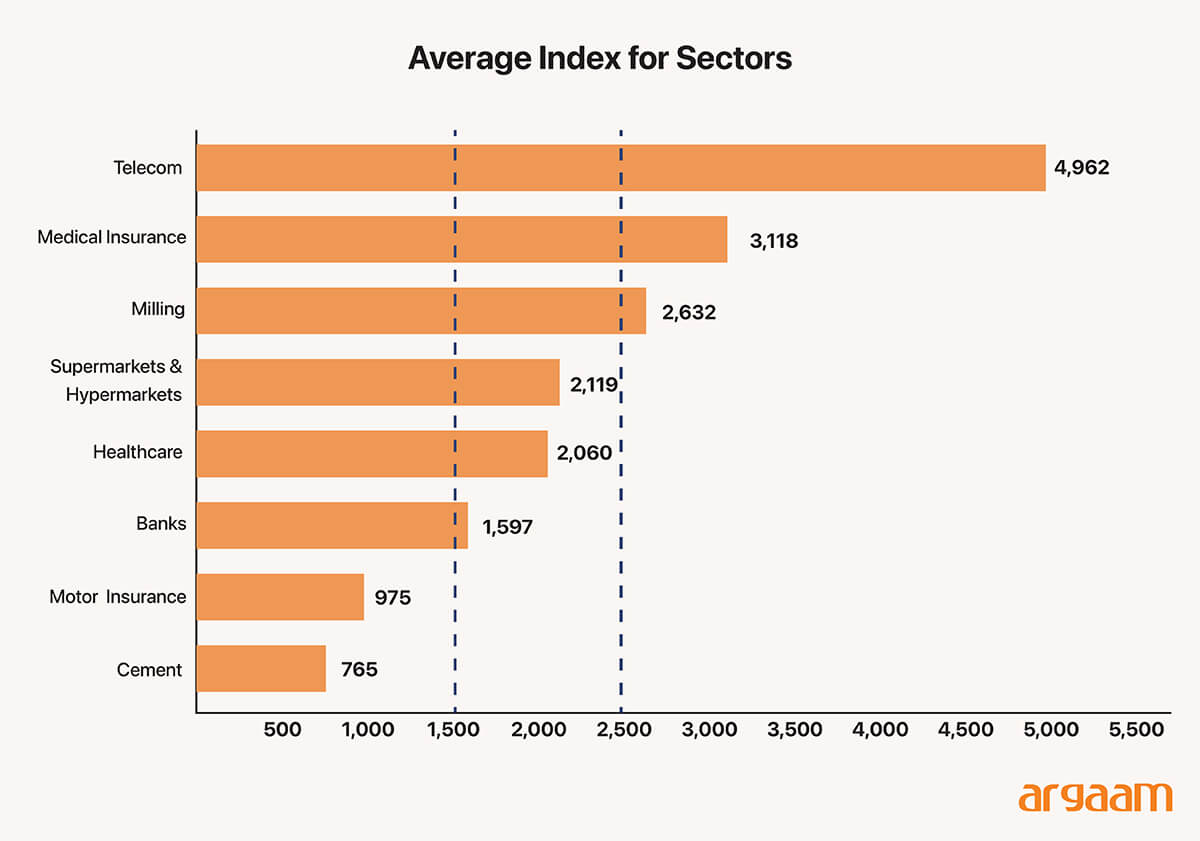

5)Practical Examples from the Saudi Market (2020–2024)

The following chart illustrates the level of competition across various sectors of the Saudi market — cement, insurance (motor and medical), banking, healthcare, supermarkets & hypermarkets, mills, and telecom.

And its evolution from 2020 to 2024, based on company data such as revenues, sales volume (cement), gross written premiums (insurance), or total assets (banking) to calculate market share.

Using the average HHI for each sector during the study period, the cement and motor insurance sectors show low concentration – indicating high competition. Three sectors exhibit medium concentration – reflecting moderate competition – namely banking, healthcare, and supermarkets & hypermarkets (with banks being very close to the lower limit of the medium concentration range).

Meanwhile, the mills, medical insurance, and telecom sectors display high concentration – indicating weak competition.

First High Competition and Low HHI indicator

Smart read High competition means that growth is not achieved through market share, but through efficiency and cost discipline. Growth becomes difficult… and profitability remains under constant pressure.

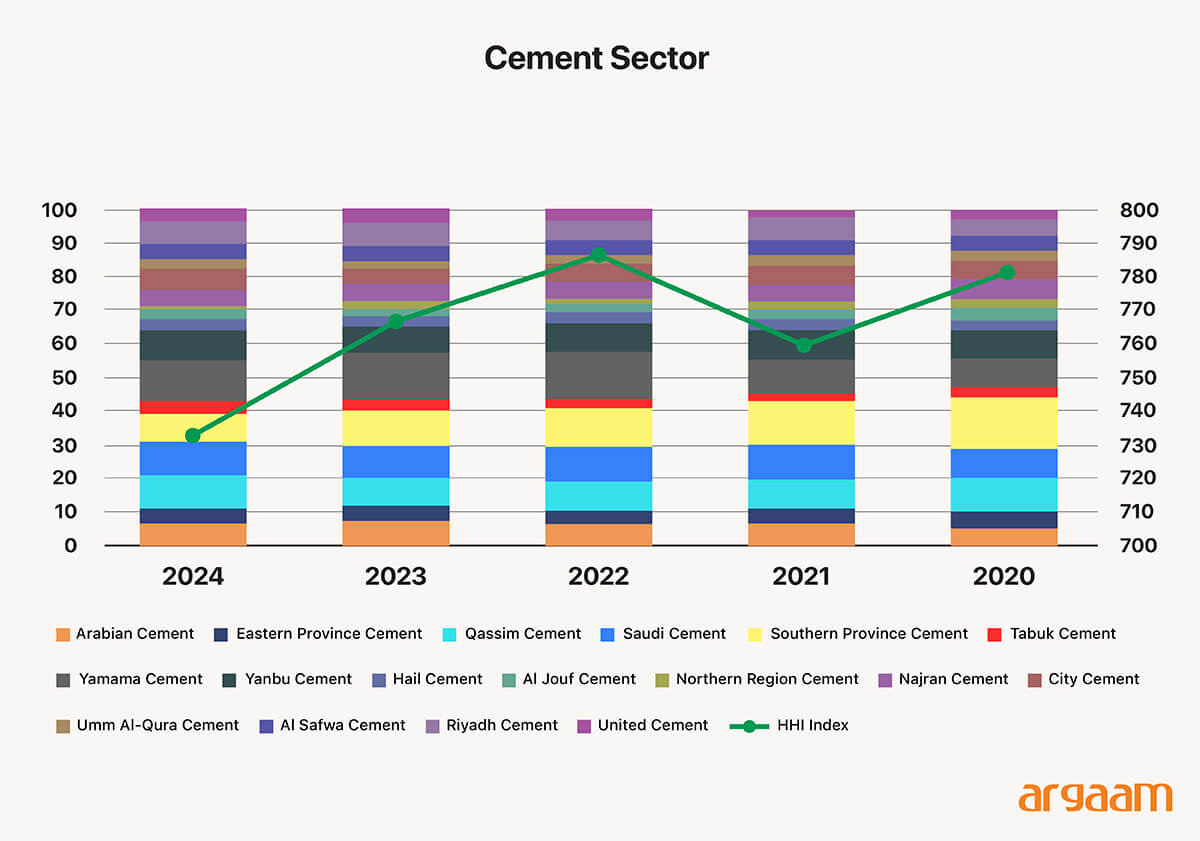

Cement Sector

Low Concentration – High Competition

According to the index, the cement industry in Saudi Arabia emerged as the most competitive sector, with 17companies operating in the market, including 14 listed on the Saudi Exchange (Tadawul).

Only two companies accounted for more than 10% of domestic cement sales in 2024; namely, Yamama Cement Co. and Saudi Cement Co., with market shares of 12% and 10%, respectively.

This reflects intense competition, which is clearly evident in the distribution of market shares across the sector players.

The HHI further confirms this strong competitive environment, with the index standing at 781 points in 2024, compared with an average of 775 points over the study period.

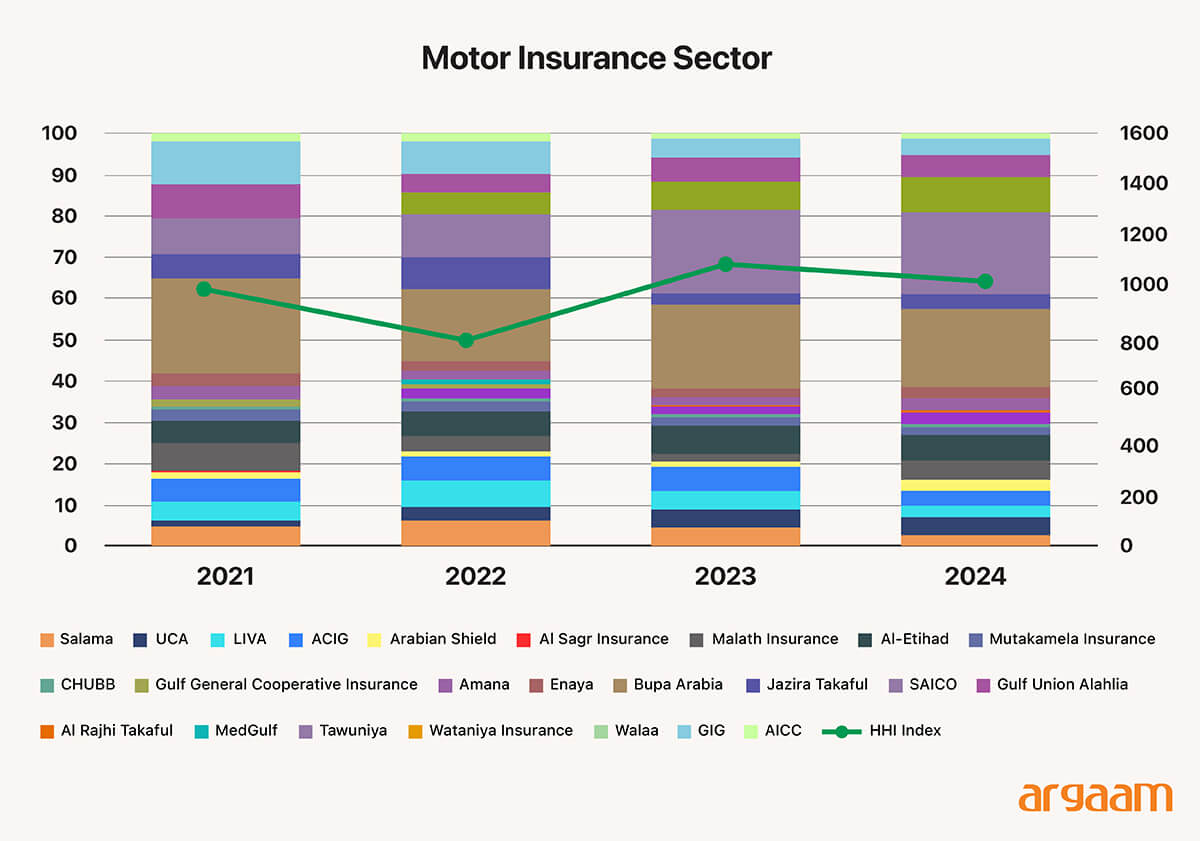

Motor Insurance Low Concentration – High Competition

The motor insurance sector is highly competitive, with 24 companies listed on Tadawul.

The Company for Cooperative Insurance Tawuniya leads the market with a 20% share of total gross written premiums (GWPs) in 2024, followed by Al-Rajhi Company for Cooperative Insurance Al Rajhi Takaful with a 19% market share.

Wataniya Insurance Co. ranked next with an 8.5% share, followed by Al-Etihad Cooperative Insurance Co. at 6%, while the remaining companies held market shares of no more than 5% each.

The sector’s HHI stood at 1,026 points in 2024, with an average of 975 points over the study period, indicating low market concentration and, consequently, a high level of competition.

Second Moderate Competition and Moderate HHI

Smart read The market can quickly slip into higher concentration with any additional merger.

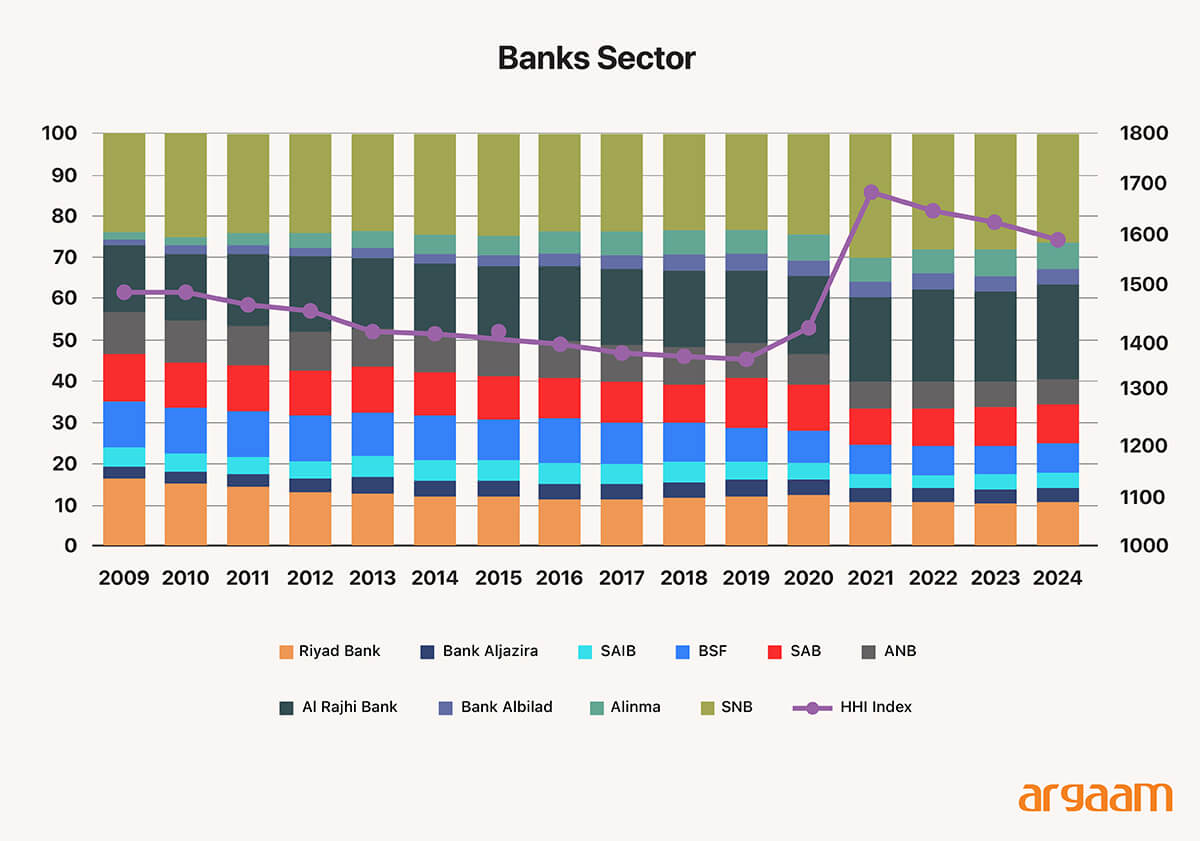

A total of 10 banks are listed on the Saudi Exchange, with combined assets reaching SAR 4,210 billion at the end of 2024.

Based on market share calculated using total assets,Saudi National Bank (SNB) leads the sector with a market share of 26%, followed by Al Rajhi Bank at 23%, and Riyad Bank at around 11%. The remaining banks hold market shares that do not exceed 10% each.

The HHI reflects relatively fierce competition within the sector, with the index reaching 1,595 points in 2024 and averaging 1,597 points over the study period -a level close to 1,500- which represents the upper threshold of low concentration.

It is worth noting that the index remained below 1,500 points throughout 2009 - 2020.

However, following the completion of the merger between Saudi British Bank (SABB) and Alawwal Bank in March 2021, as well as the merger between National Commercial Bank and Samba Financial Group in January 2022, market shares in the banking sector changed markedly.

In 2021, SNB market share rose from 24% in 2020 to 30%, increasing sector concentration and pushing the HHI up from 1,428 points in 2020 to 1,687 points in 2021, as illustrated in the following chart.

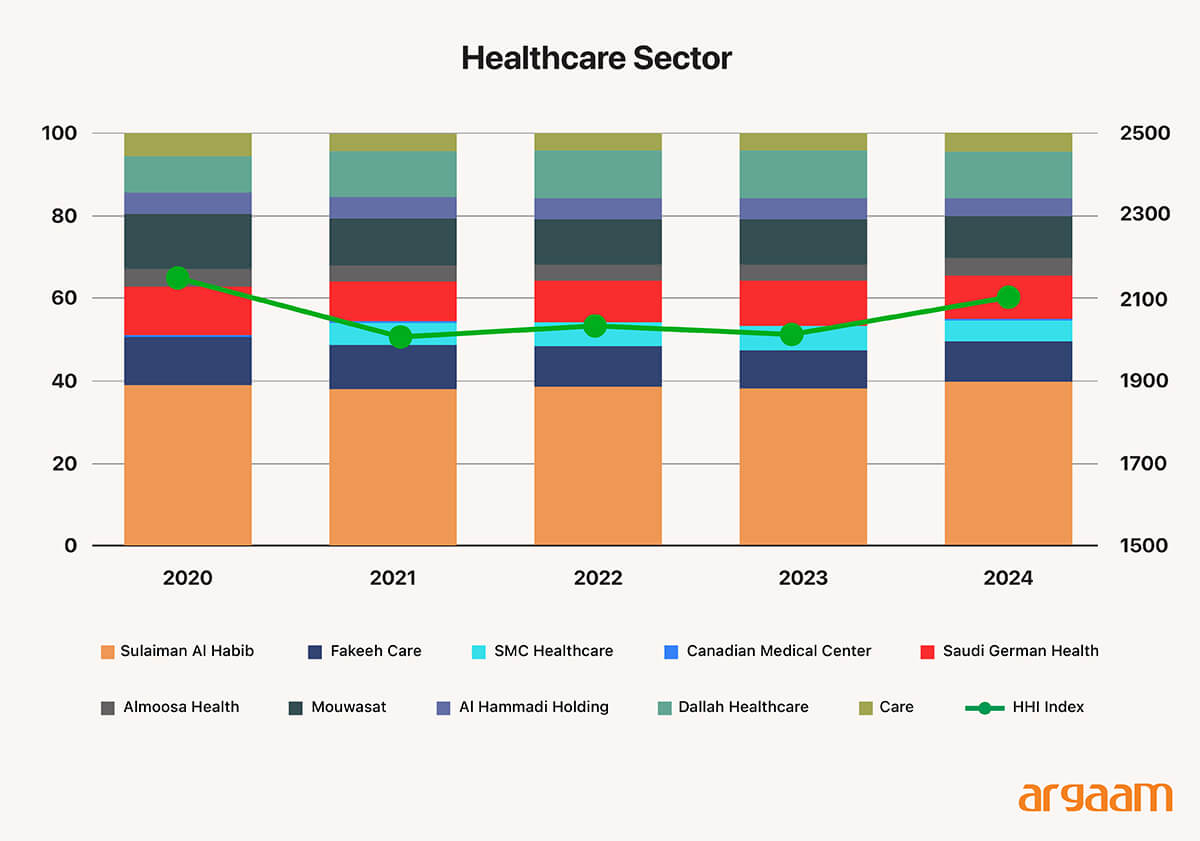

The healthcare sector in Saudi Arabia is similar to the insurance and banking sectors in terms of market concentration, as it exhibits moderate concentration and, therefore, moderate competition.

The sector comprises 10 companies listed on the Saudi Exchange. Dr. Sulaiman Al Habib Medical Services Group leads the market, dominating around 40% of sector revenue in 2024, followed by Dallah Healthcare Co. with an 11% market share.

Dr. Soliman Abdel Kader Fakeeh Hospital Co. (Fakeeh Care), Middle East Healthcare Co. (Saudi German Health), and Mouwasat Medical Services Co. each hold market shares of around 10%.

This reflects relatively high concentration within the sector, as a single company controls 40% of revenue, while four other companies collectively account for a similar share. The remaining five companies in the sector generate no more than 5% each of total sector revenue.

The HHI for the healthcare sector stood at 2,100 points in 2024, with an average of 2,060 points over the study period, indicating a tendency toward moderate concentration and moderate competition.

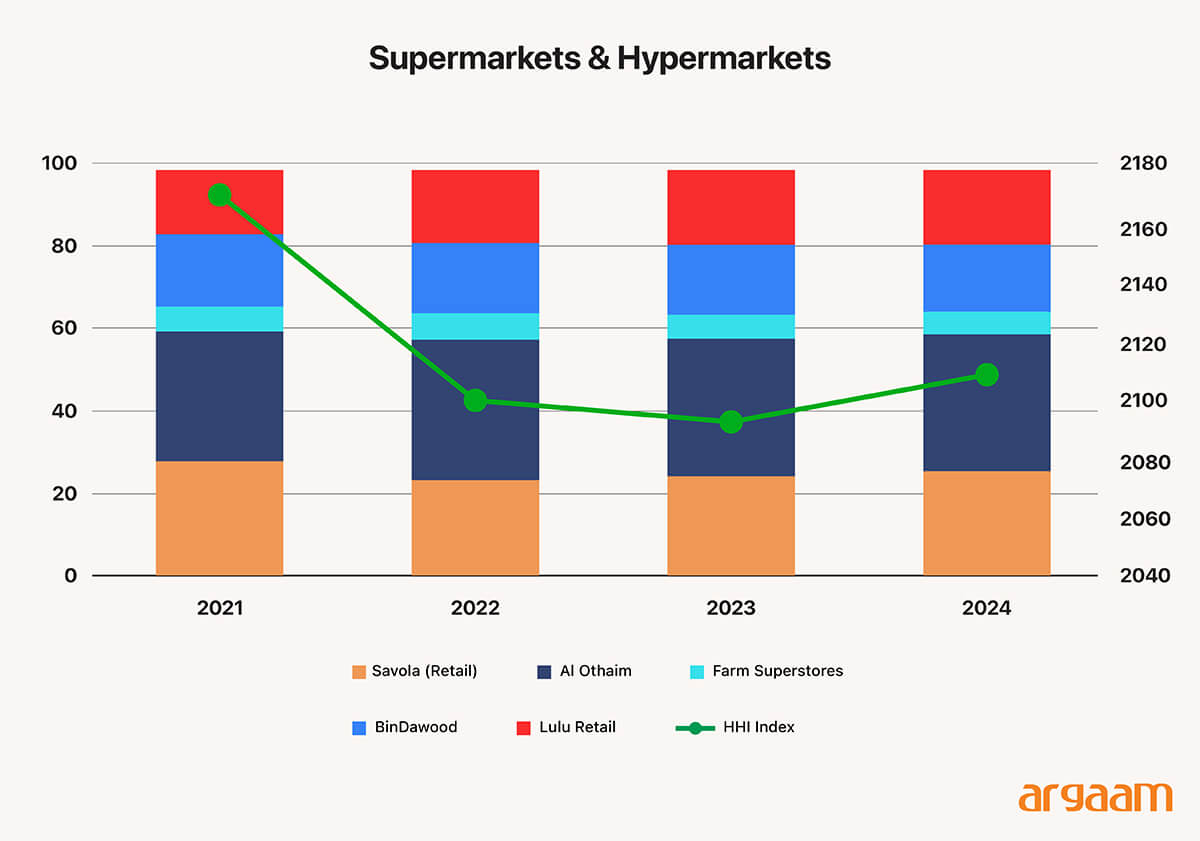

The industry comprises three companies with retail as the core business activity; namely, Abdullah Al Othaim Markets Co., Saudi Marketing Co. (Farm Superstores) and BinDawood Holding Co.

However, revenue generated by Savola Group’s retail segment as well as revenue from Lulu Retail in Saudi Arabia were also included to present a more comprehensive view of this industry.

In 2024, Al Othaim accounted for 34% of total revenue, followed by Savola Group’s retail segment with a 26% share. Lulu Retail ranked next with an 18% share, while BinDawood Holding held a 16% share. Farm Superstores accounted for 6% of total revenue.

The sector’s HHI reached 2,109 points in 2024, with an average of 2,119 points over the study period, indicating a tendency toward moderate market concentration and moderate competition.

Third Weak Competiton and High HHI

Smart read Strong performance may reflect a protected infrastructure rather than true competitive superiority.

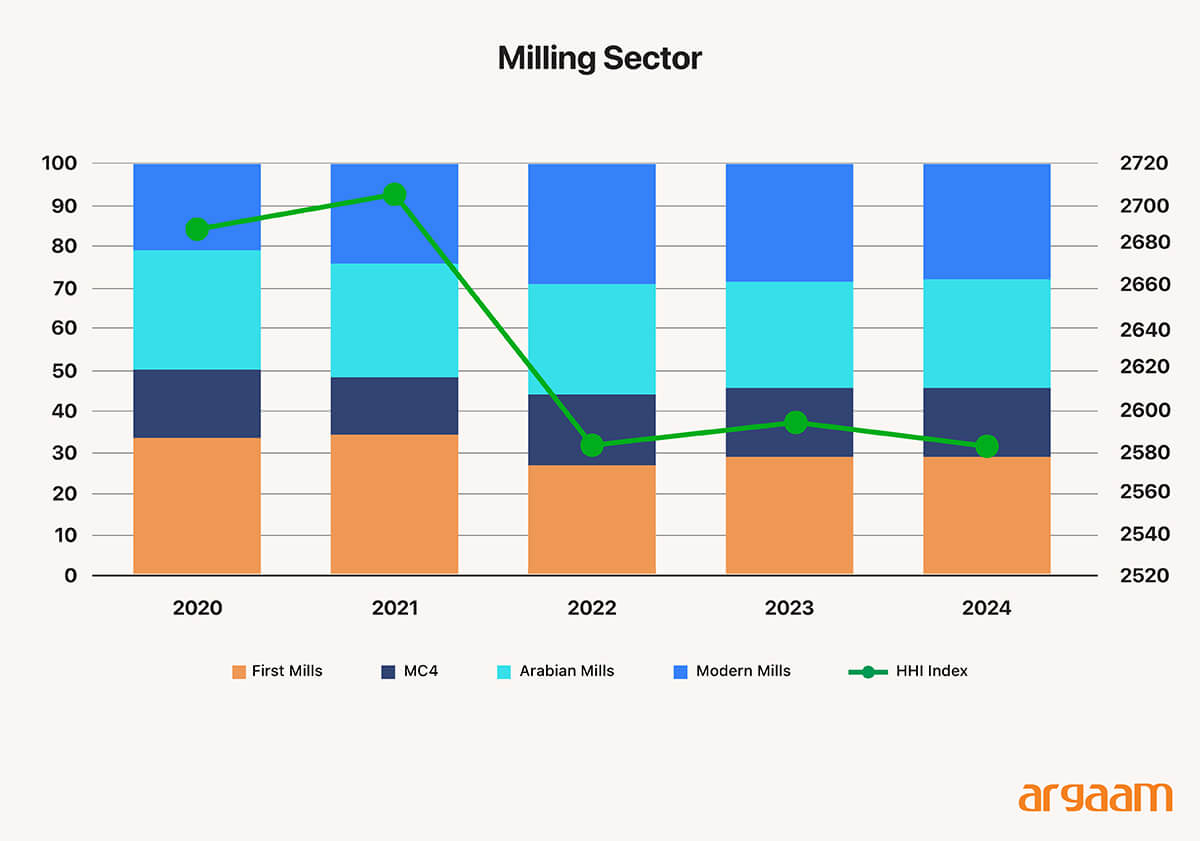

Milling Sector High Concentration – Weak Competition

The milling sector consists of four companies: First Milling Co. (First Mills), Fourth Milling Co. (MC4), Arabian Mills for Food Products Co. (Arabian Mills) and Modern Mills for Food Products Co. (Modern Mills).

First Mills took over a 29% share of the sector’s revenues in 2024, followed by Arabian Mills and Modern Mills, each with a 27% share. MC4 ranked fourth with an 18% share of total sector revenues.

HHI indicates a high level of concentration and weak competition in the sector, with the index reaching 2,583 points in 2024, compared with an average of 2,632 points over the study period.

The index also reflects a notable shift from 2020, when it stood at 2,690 points, declining to 2,583 points in 2024 following a loss in revenue share by First Mills and Arabian Mills in favor of the other two firms.

This redistribution of market shares could potentially push the HHI below the 2,500-point threshold, which would reclassify the sector as moderately concentrated and imply a more competitive market structure.

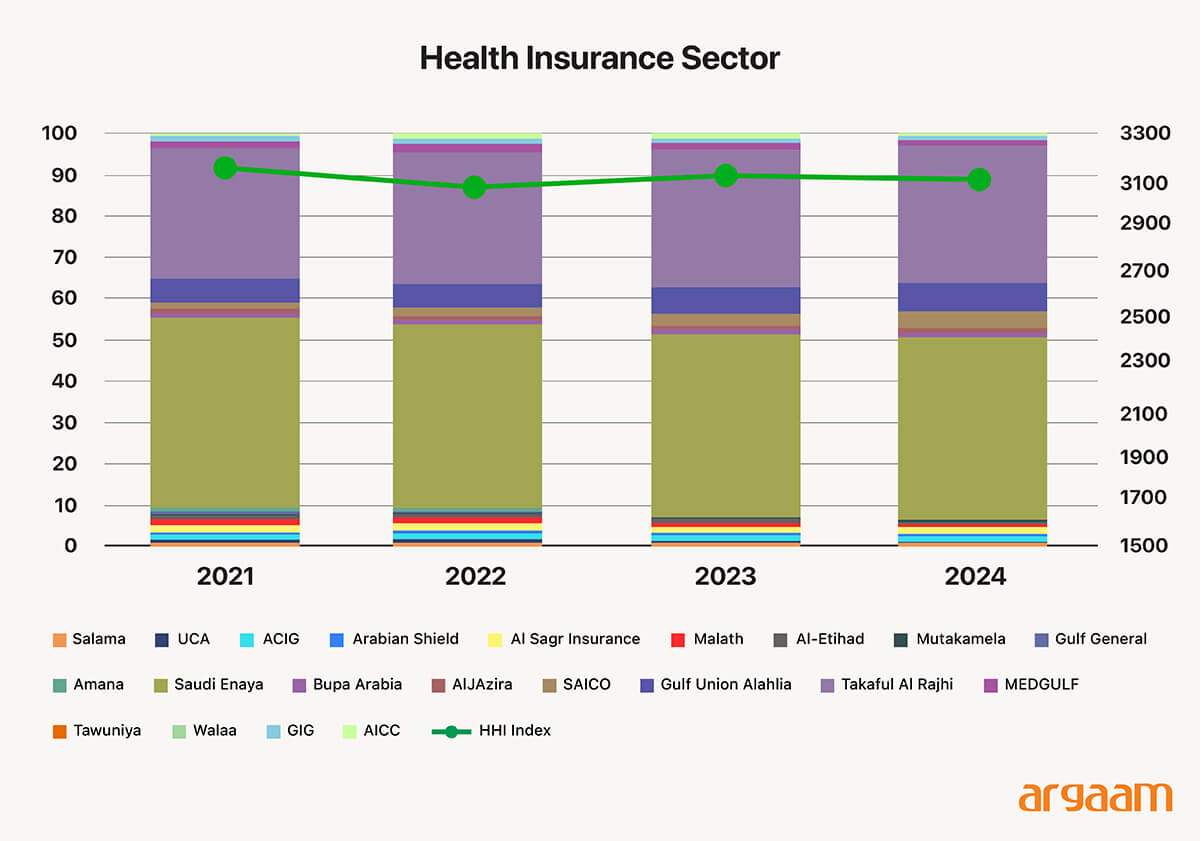

Health Insurance Sector High Concentration – Weak Competition

The health insurance sector comprises 20 companies listed on the Saudi Exchange.

Bupa Arabia for Cooperative Insurance Co. led the market with a 44% market share of total gross written premiums (GWPs) in 2024, followed by The Company for Cooperative Insurance (Tawuniya) with a 33% market share, and The Mediterranean and Gulf Insurance and Reinsurance Co. (MEDGULF) with 7%. The remaining companies each held individual market shares that do not exceed 5%.

The sector’s HHI reached 3,118 points in 2024, which is also the average over the study period. This level indicates a highly concentrated market structure, reflecting weak competitive intensity within the sector.

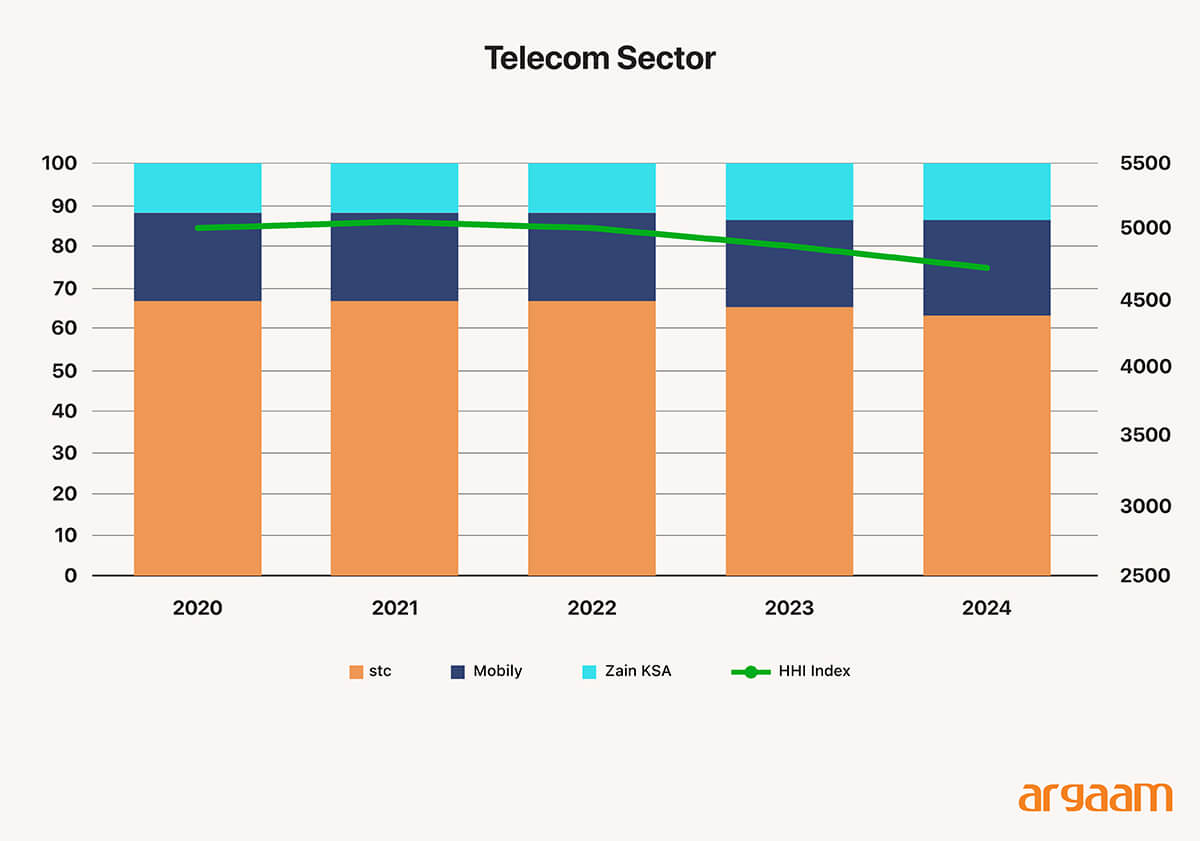

Telecom Sector (Mobile Services in Saudi Arabia) High Concentration – Weak Competition

The mobile telecommunications sector in Saudi Arabia comprises three operators. stc Group held the leading market position, accounting for approximately 63% of total sector revenues in 2024. It was followed by Etihad Etisalat Co. (Mobily) representing 23% of the sector revenues, while Mobile Telecommunication Company Saudi Arabia (ZAIN KSA) took over a 13% share of total revenues.

HHI indicated a high level of market concentration and weak competition, with the index reaching 4,779 points in 2024, compared to an average of 4,962 points over the study period.

This high concentration is driven by the combined dominance of stc and Mobily, which together account for 86% of total sector revenues generated within the Kingdom.

It is worth noting that telecommunications sectors in most countries worldwide are typically characterized by high market concentration, reflecting the limited number of operators within each country and the substantial capital investments required for new entrants to enter the market.

ℹ︎

Where do investors or policymakers go wrong?

● Confusing a profitable sector with a competitive one

● Assuming performance is driven by efficiency rather than by massive or protected infrastructure ● Overlooking the impact of small mergers

Sixth: Advantages and Disadvantages of the HHI

Advantages of the HHI

● High Accuracy: It takes into account all firms operating in the market, not only the key players. ● Greater Weight Assigned to Large Firms: Because market shares are squared, dominant firms are reflected more clearly.

Example: A company with a 40% market share has a weight of 1,600 in the index, which is equivalent to the combined impact of four companies each holding a 20% market share.

● Easy to Calculate and Interpret: It can be readily applied to any sector and across any time period. ● Sensitive to Market Changes: Any increase or decrease in the market share of a large firm is immediately reflected in the HHI value. ● Internationally Recognized Benchmark: Adopted by major regulatory authorities and used in more than 60 countries.

Disadvantages of the HHI

● Relies Solely on Market Share: Does not account for product quality, pricing, innovation, or barriers to market entry. ● Ignores Competitive Conduct: A market may be highly concentrated, yet firms compete intensely. ● Over-Sensitivity to Large Firms: Squaring market shares may overweight the dominance of large players. ● Does Not Reflect Indirect Competition: Example: Delivery apps compete with restaurants, but this competition is not reflected in the index due to the large number of firms involved. ● Potentially Misleading in Certain Cases: In sectors that naturally have a limited number of firms (such as telecom sector), the index may indicate high concentration even when competition is relatively strong.

ℹ︎

What are the indirect effects?

Rising concentration does not always appear as an immediate problem, but it: ● Gradually weakens innovation ● Raises entry barriers ● Shifts competition from the market to regulation

✦

Market signals to watch

● Any merger within moderately concentrated sectors

● Changes in the market shares of major companies

● Indirect regulatory interventions

Conclusion

The HHI reveals significant variation in the degree of competition across Saudi market sectors: Low Concentration (High Competition): Cement and motor insurance sectors. Moderate Concentration (Moderate Competition): Banking, healthcare, and supermarkets & hypermarkets sectors. High Concentration (Low Competition): Milling, health insurance, and telecom sectors.

The HHI remains an important tool for understanding market structure, provided it is used alongside other indicators that capture competitive behavior and structural market factors.

The importance of examining market structure becomes clear when linking the findings of this analysis to Argaam Intelligence’s reports—specifically the business‑model analysis of the mobility sector in Saudi Arabia—which shows how market concentration and competitive intensity directly shape unit economics and returns on capital in labor‑ and operations‑intensive service sectors.

More this Weekend

The Limits of BNPL in Saudi Arabia: Growth Without Disruption

Despite the growing visibility of buy now, pay later (BNPL) options in Saudi Arabia’s offline retail landscape, the model is unlikely to pose a structural challenge to the credit cards’ market.The apparent expansion of BNPL offline, with some unofficial ratios estimated at 40% of all BNPL transactions, reflects neither superior payment efficiency nor a wholesale shift in consumer preference, but rather its ability to reach segments that have historically sat outside the core credit card market.

The Impact of Saudi’s New Sugar Tax: Opportunities and Challenges for Industry Leaders PepsiCo and Almarai

Saudi Arabia’s upcoming shift to a tiered excise tax on sugar-sweetened beverages (SSBs) from January 2026 marks a pivotal moment with far-reaching consequences. This policy overhaul, replacing a longstanding 50% flat tax, promises to reshape consumption patterns, redefine industry strategies, and reshape government revenue streams.

A Comparative Analysis of Three Car Rental and Ride-Sharing Business Models in Saudi Arabia

Despite the growing visibility of buy now, pay later (BNPL) options in Saudi Arabia’s offline retail landscape, the model is unlikely to pose a structural challenge to the credit cards’ market.The apparent expansion of BNPL offline, with some unofficial ratios estimated at 40% of all BNPL transactions, reflects neither superior payment efficiency nor a wholesale shift in consumer preference, but rather its ability to reach segments that have historically sat outside the core credit card market.