Saudi Arabia’s upcoming shift to a tiered excise tax on sugar-sweetened beverages (SSBs) from January 2026 marks a pivotal moment with far-reaching consequences.

This policy overhaul, replacing a longstanding 50% flat tax, promises to reshape consumption patterns, redefine industry strategies, and reshape government revenue streams.

Yet, beneath these anticipated shifts lies a complex, often unpredictable, variable: the price elasticities of demand for SSBs.

At the heart of this analysis is a pressing, often overlooked question: how does the sensitivity of consumers to price changes—captured by the Price Elasticity of Demand—intertwine with the very fabric of the beverage industry?

Could the degree of consumer responsiveness dictate not only how much revenue the government collects but also influence the strategic moves of beverage firms operating within a fiercely competitive landscape?

And crucially, what ripple effects might these economic forces have on public health outcomes, potentially altering the trajectory of non-communicable diseases and health disparities in the region?

Our analysis examines how the implementation of the new sugar tax could impact the financial strategy and strategic positioning of the two largest companies in the soft drinks and flavoured milk in Saudi Arabia: PepsiCo and Almarai.

The study considers how each company’s adaptation to the tiered sugar tax may enhance or challenge their financial resilience.

Saudi’s Second-Generation Tax Model

Saudi Arabia will implement a new tiered excise tax on sugar-sweetened beverages (SSBs) from January 2026, replacing the existing 50% flat excise tax that has been in place for several years.

Under the new system, sugar-sweetened beverages will be taxed according to the amount of sugar per 100 millilitres, rather than a uniform percentage of product value.

Beverages containing less than 5 grams of sugar per 100 ml will be exempt from excise tax, while products with sugar content between 5 and 7.99 grams per 100 ml will be subject to a levy of SAR 0.79 per litre.

Drinks exceeding 8 grams of sugar per 100 ml will face the highest rate of SAR 1.09 per litre. (Zakat, Tax and Customs Authority)

This approach brings Saudi Arabia closer to the “second-generation” sugar tax models already adopted in several international markets, where taxation is used not only as a revenue instrument but also as a behavioural policy tool.

The Critical Role of PED in Saudi’s Sugar Tax Success

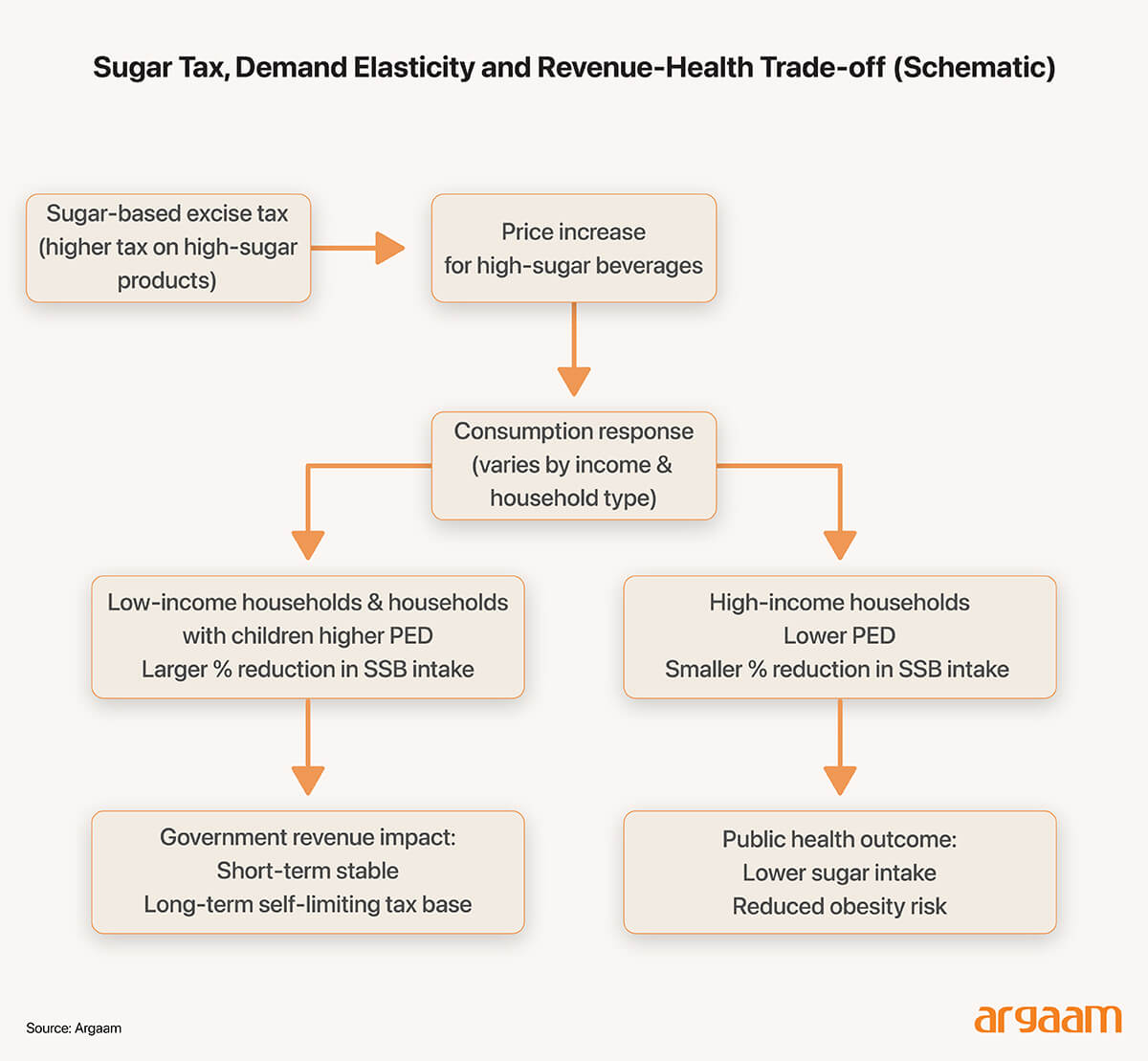

The impact of the new tiered sugar tax on consumption patterns, firm pricing strategies, and government revenue hinges critically on the price elasticity of demand (PED) for sugar-sweetened beverages (SSBs).

The PED measures how much the amount of the sugary drink people buy changes when the price goes up or down.

So, it measures the percentage change in quantity demanded resulting from a one percent change in price, and it fundamentally shapes how much of the excise burden can be passed on to consumers versus absorbed by producers.

If the PED is high (more negative), it means that when prices increase, people buy a lot less of these drinks. Conversely, if prices drop, they buy a lot more.

So, an elasticity of -2 means that for a 1%increase in price, the quantity demanded decreases by 2%. Accordingly, if the price rises by 10%, people will buy about 20% less.

Empirical evidence from other emerging economies consistently shows that demand for SSBs tends to be moderately elastic: for instance, econometric analyses in Latin America estimate PED values of approximately -1.06 for carbonated soft drinks and -1.16 for broader SSB categories, indicating that a 10% price increase is likely to reduce consumption by approximately 10–12%.(PMC,2015)

Importantly, elasticity is not uniform across all beverage types and consumer contexts.

In Brazil, estimates for ready-to-drink sugary beverages are around -1.19, while prepared SSBs exhibit far higher elasticity of up to -3.38, reflecting greater sensitivity to price changes when close substitutes or consumption alternatives are available.

Additional cross-country studies suggest that elasticity can vary significantly by income and market structure, with lower-income households often showing stronger responsiveness to price changes. (PMC,2023)

This variation in how different people respond to prices means that the way the tax affects who pays and how much they pay will vary across groups.

Where demand is relatively elastic—such as in segments with multiple low-sugar or substitute options—consumers are more likely to reduce quantities or shift to lower-taxed products, limiting firms’ ability to fully pass on increased costs.

Conversely, in categories with lower elasticity—such as habitual household purchases with fewer substitutes—the potential for firms to transfer a greater share of tax burden to consumers increases, and tax revenues may remain more stable.

Therefore, how well the sugar tax works—both for raising money and encouraging people to change their habits—depends on the combination of the official tax rates and how different groups of people actually respond to the prices of various beverage types.

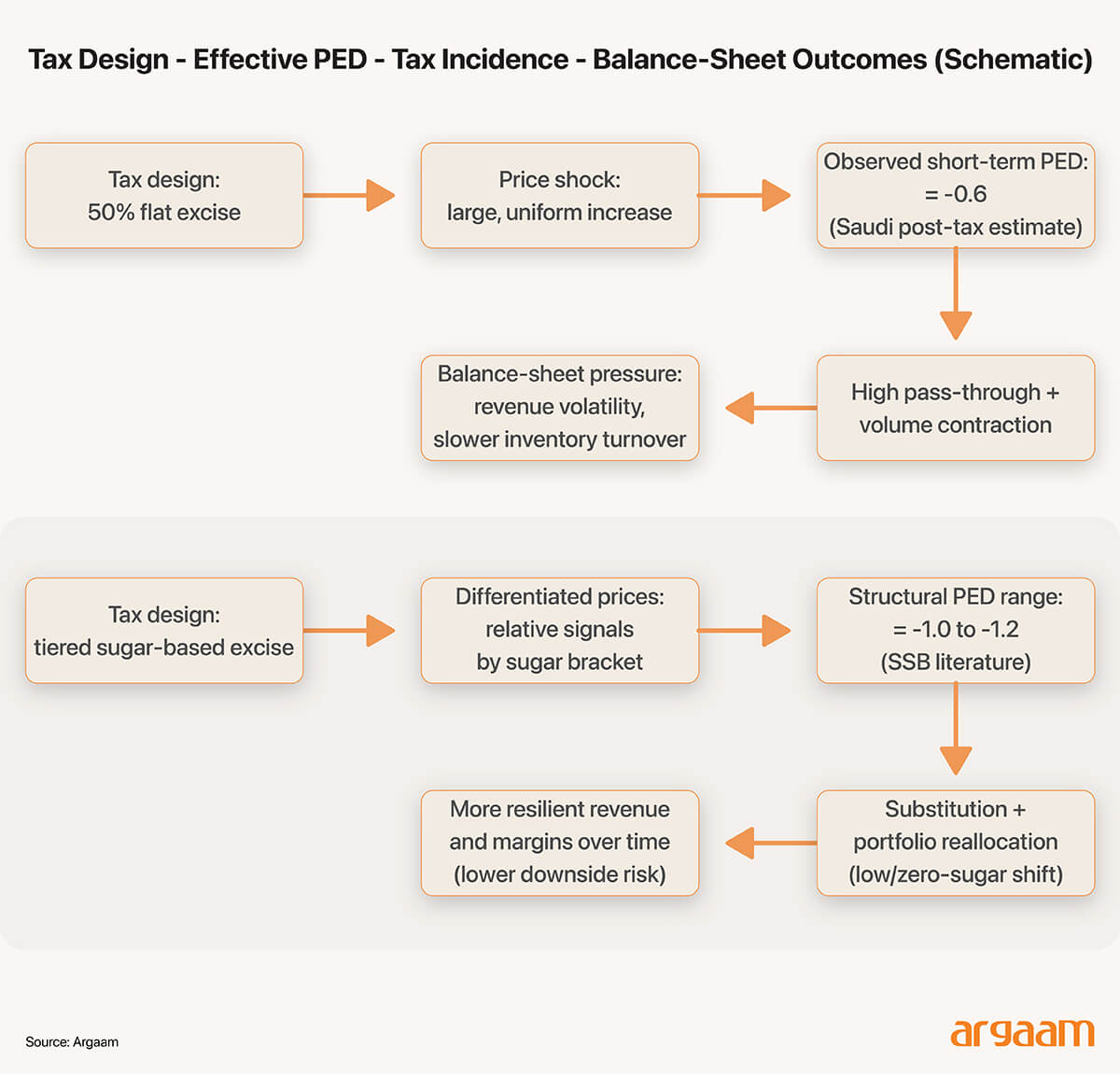

Eroding Revenues Despite Higher Prices under the old tax flat-rate system: PepsiCo as a case study

As a major player in the Saudi beverage market, the change in SSBs tax is of great significance to PepsiCo. Under the previous flat tax regime, empirical evidence suggests that carbonated soft drinks in Saudi Arabia experienced substantial price pass-through—exceeding 100% in some cases—accompanied by a significant contraction in sales volumes.

A price elasticity of demand for carbonated beverages of approximately –0.6 during the post-tax period, indicating that while firms were able to transfer a large share of the tax burden to consumers under the old tax system, the resulting volume decline constrained revenue growth. (Tufts University,2020)

From a balance-sheet perspective, this implied a trade-off for PepsiCo. Higher unit prices supported gross margins on a per-unit basis, but reduced sales volumes limited top-line expansion and exerted pressure on working capital efficiency through slower inventory turnover.

The uniform nature of the old 50% tax further restricted strategic flexibility, as both high- and low-sugar products were subject to the same tax treatment, limiting PepsiCo’s ability to mitigate excise exposure through portfolio reallocation.

The Tiered Tax System is a Game-Changer for Revenue Stability and Margin Strength

The new tiered sugar tax alters this dynamic in a way that is likely to be relatively favourable for PepsiCo compared with the flat-rate regime.

Given empirical evidence that demand for sugar-sweetened beverages is moderately elastic overall (with PED estimates around -1.0 to -1.2 as mentioned before), price increases on high-sugar products are likely to induce further volume reductions.

However, PepsiCo’s diversified product portfolio—including zero- and low-sugar variants that fall into lower or zero tax brackets—allows the firm to shift sales toward segments with lower effective tax incidence.

This reduces the need for aggressive price increases across the portfolio and supports volume stability in lower-taxed categories.

In balance-sheet terms, the tiered system may therefore lower downside risks to revenues and improve margin resilience relative to the 50% flat tax, despite potential short-term increases in operating expenses related to reformulation and marketing.

While capital expenditure on product adaptation could modestly increase in the near term, the ability to reallocate revenues toward lower-taxed products suggests a more sustainable earnings profile over time, implying a comparatively more favourable impact on PepsiCo’s balance sheet than under the previous uniform excise tax regime.

In contrast to PepsiCo, Almarai’s exposure to the new tiered sugar tax is shaped by a markedly different market position and product structure.

How Habitual Consumption Shields Al Marai’s Products from Tax Impact

As Saudi Arabia’s largest dairy producer, Almarai’s sweetened beverage portfolio is concentrated in flavoured milk and milk-based drinks, which are predominantly consumed by households and children.

These products tend to exhibit lower price elasticity of demand than carbonated soft drinks, reflecting habitual consumption patterns and fewer close substitutes.

As a result, demand for sweetened dairy products is likely to be less responsive to price increases induced by excise taxation.

Under the previous 50% flat excise tax, Almarai’s exposure was relatively contained, as dairy-based beverages were not the primary target of the policy and price adjustments could be absorbed within a broader fresh dairy portfolio.

However, the shift to a sugar-content-based tax introduces a more direct linkage between sugar intensity and tax liability, increasing effective exposure for sweetened milk products with limited scope for immediate substitution.

Given lower demand elasticity, Almarai may be able to pass through a larger share of the tax burden to consumers in the short term, supporting nominal revenues.

From a balance-sheet perspective, this pricing power may come at the cost of longer-term risks.

Higher retail prices could gradually erode volumes in price-sensitive household segments, while reformulation efforts to reduce sugar content may require additional operating expenditure and adjustments to production processes.

Compared with PepsiCo’s diversified beverage portfolio, Almarai’s narrower product mix implies lower strategic flexibility, potentially increasing earnings volatility and balance-sheet sensitivity under the new tiered excise regime.

Almarai, Saudi Arabia’s largest dairy producer, offers a range of sweetened liquid dairy products such as flavored milks that are widely consumed in household and child nutrition contexts.(Almarai,2025)

Under the new tiered sugar tax, these products—many of which exceed the 8 g/100 ml sugar threshold—will be subject to the highest excise rate, creating distinct demand responses compared with multinational carbonated soft drinks.

Empirical evidence suggests that dairy-based sweetened beverages often exhibit lower price elasticity than carbonated soft drinks, particularly in segments consumed as everyday staples, implying that consumers are less responsive to price increases in these categories.(PMC, 2010).

This lower elasticity can enable producers to pass through a larger share of the tax to final prices without experiencing the same degree of volume contraction observed in more elastic segments.

However, while higher pass-through may support revenue stability in the short term, it can also compress demand over time if consumer substitution towards non-taxed or lower-tax alternatives accelerates, especially in price-sensitive households.

On the cost side, Almarai may face increased production expenses if it chooses to reformulate or invest in product diversification to reduce tax exposure—efforts that could require capital outlays and marketing investments.

With working capital tied up in inventory and distribution, the balance sheet impact may include pressure on net sales and receivables turnover.

Relative to the uniform 50% excise tax, the tiered design is unlikely to provide Almarai the same flexibility enjoyed by diversified beverage producers, potentially resulting in a comparatively more negative short-term effect on revenue growth and balance sheet resilience.

New Sugar Tiers Prioritize Health Over Tax Income

The revenue impact of Saudi Arabia’s new sugar-based excise will be shaped by the same PED and tax-incidence mechanisms discussed above.

Government receipts equal the effective tax per litre multiplied by the post-tax quantity sold.

Under the previous 50% flat excise, evidence from Saudi Arabia’s carbonated drinks market shows substantial tax pass-through and a sizeable drop in volumes after the implementation of the tax—consistent with demand that is not perfectly inelastic and therefore capable of eroding the tax base over time.

Compared with a uniform ad valorem rate, a sugar-linked design can initially stabilise revenues by concentrating the tax burden on higher-sugar products and creating incentives for manufacturers to move products into lower-tax brackets (reformulation) rather than simply raising prices.

ℹ︎

A uniform ad valorem rate means applying the same percentage tax to all products, regardless of their sugar content or other differences.

Over the medium term, however, revenues may become more self-limiting: if demand for high-sugar SKUs is elastic (as suggested by international SSB estimates around -1.06 for carbonated soft drinks), higher effective prices can accelerate substitution toward zero/low-sugar options and reduce sales in the highest-tax brackets—supporting the public-health objective but shrinking the taxable base.

An SKU, or Stock Keeping Unit, is a unique identifier for each distinct product offered by a retailer or manufacturer. It typically encompasses specifics such as brand, size, packaging, flavor, or other attributes that differentiate one product from another.

This matters because obesity remains a material policy concern. The obesity rate is reportedly of 23.1% among people aged 15+ and 14.6% among children aged 2–14 (with overweight prevalence higher still), underscoring the rationale for earmarking excise proceeds for prevention programmes.(GASTAT,2024).

Saudi media has similarly cited evidence that around 20% of adults are obese.(Arabnews,2025)

Distributionally, SSB taxes are often financially regressive because lower-income households and households with children tend to consume more sweetened beverages.

Yet they can be progressive in health terms if these groups are more price responsive.

Evidence from Italy’s proposed sugar tax modelling finds it reduces per-capita SSBs consumption for low-income households by 20.6% and sugar consumption by 26.7%, compared to 11.8% and 15.5% for high-income groups. (Food Policy,2024).

Recycling revenues into targeted health programmes for vulnerable groups (including low-income families with children) can mitigate regressivity.

More this Weekend

Saudi sectors ranked by competitiveness using HHI metrics

Market structure and competition analysis are crucial for evaluating the competitiveness of economic sectors. Since the assessment of competition requires accurate quantitative tools, the Herfindahl–Hirschman Index (HHI) stands out as one of the most important global benchmarks for measuring market concentration.

A Comparative Analysis of Three Car Rental and Ride-Sharing Business Models in Saudi Arabia

Saudi Arabia's mobility sector is currently experiencing a pivotal phase, characterized by shifts in business models and market dynamics. While established traditional car rental companies continue to maintain stable revenue streams, the financial sustainability of fleet ownership is increasingly challenging.

The Limits of BNPL in Saudi Arabia: Growth Without Disruption

Despite the growing visibility of buy now, pay later (BNPL) options in Saudi Arabia’s offline retail landscape, the model is unlikely to pose a structural challenge to the credit cards’ market.The apparent expansion of BNPL offline, with some unofficial ratios estimated at 40% of all BNPL transactions, reflects neither superior payment efficiency nor a wholesale shift in consumer preference, but rather its ability to reach segments that have historically sat outside the core credit card market.