This analysis, produced by Argaam Intelligence's Risk Navigator team, examines the economic benefits and risks of Saudi Arabia's potential participation in yuan-denominated oil settlement — a trend gaining measurable momentum in recent months.

Our assessment weighs the bilateral efficiency gains against the broader capital market sensitivities, offering policymakers a grounded framework for navigating what is ultimately a question of financial architecture rather than geopolitical alignment.

The petrodollar arrangement can be traced back to 1974, when Saudi Arabia agreed to price oil in US dollars and invest surpluses in dollar assets, in exchange for security guarantees from Washington. Saudi Arabia, however, now sells four times as much oil to China as to the US.

Beijing's managed, predictable policy posture contrasts sharply with Washington's controversial trade policies. This alongside the severe geopolitical tensions in the region due to the Iran war have made Chinese assets an increasingly rational hedge for global portfolios seeking non-dollar anchor points.

Major oil producers like Russia, Iran and Venezuela started already accepting payments in currencies other than the US dollar.

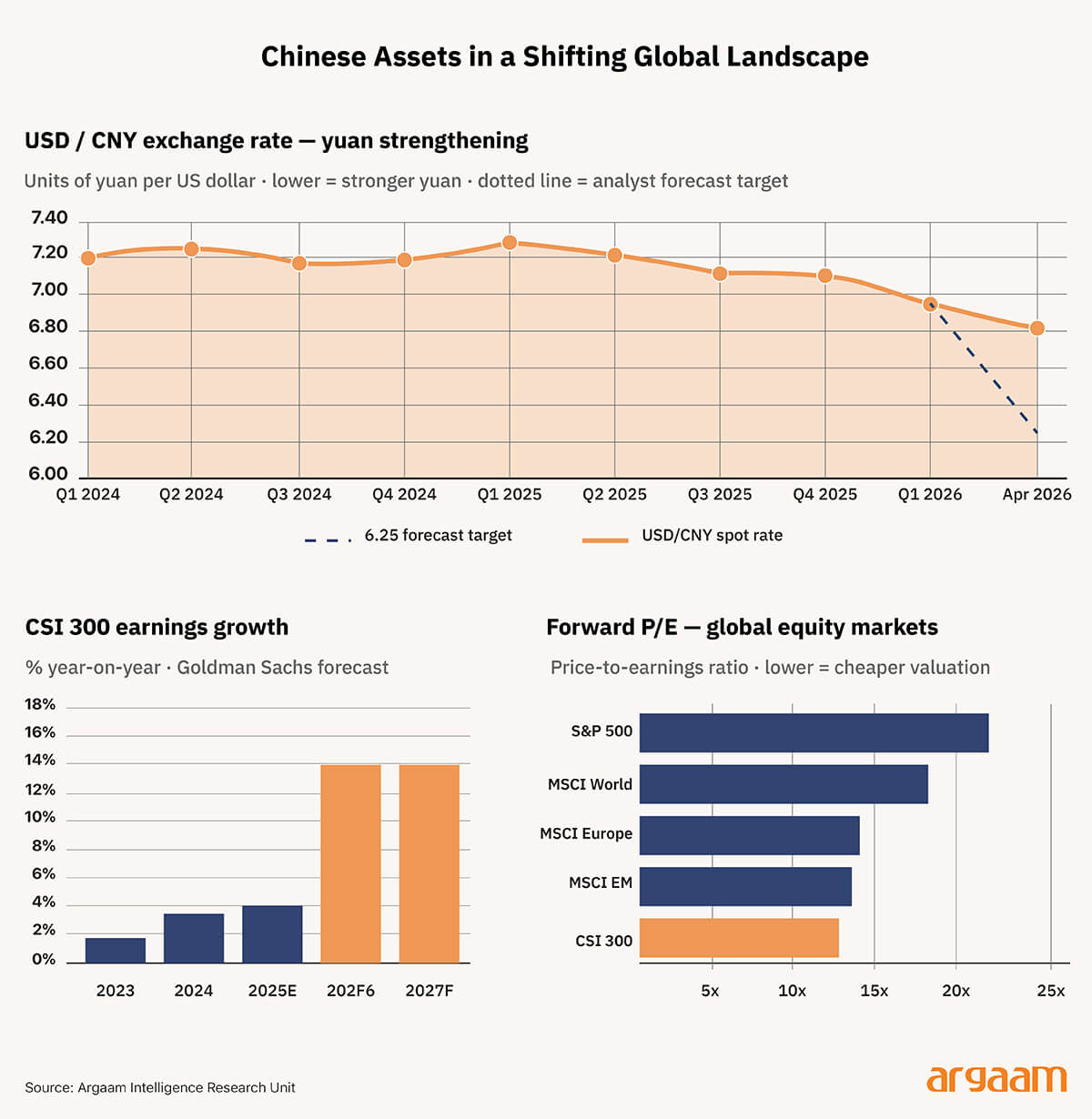

Global investment firms, chiefly Goldman Sachs Group Inc., have lifted their assessment of China’s equities market, citing compelling valuations since Chinese stocks are trading cheaply relative to their Price-to-Earnings (P/E) ratio and company profits are projected to grow strongly in H1 2026.

As Beijing allowed the yuan to breach the key 7-per-dollar level, market participants are also doubling down on the currency, with some predicting it to rise to as strong as 6.25 this year.

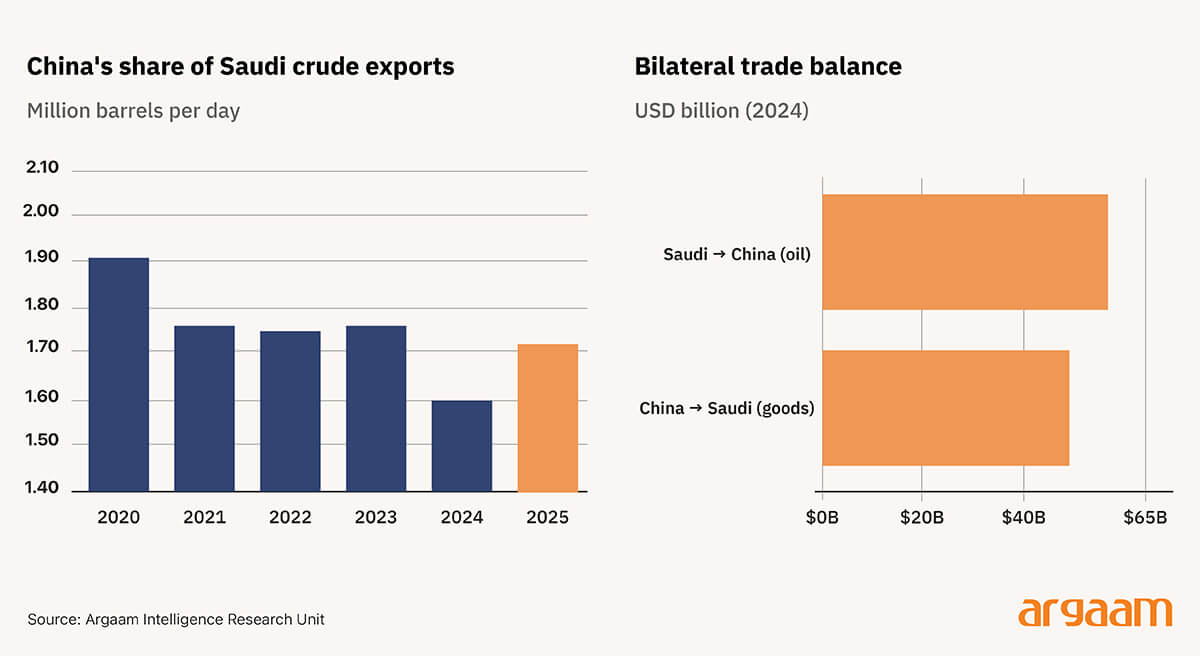

China imported 1.72 million barrels per day of Saudi crude in 2025, representing 21% of its total oil imports — making it by far Riyadh's largest single buyer.

China's total crude imports reached a record 11.6 million barrels per day in 2025, with the majority of its refining sector — including independent teapot refineries operating on thin margins — carrying costs, debts, and revenues entirely denominated in yuan.

For these buyers, dollar-priced oil is not merely an inconvenience; it is a structural balance sheet risk embedded into every cargo purchase.

This commercial reality creates asymmetric pressure. Saudi Arabia's pricing power has historically rested on a unified global benchmark — Brent or Arab Light differentials — denominated in dollars, allowing Riyadh to function as the market's swing producer with a single, transparent price signal.

Introducing even a partial yuan settlement tier creates two parallel pricing systems with different benchmarks, different clearing infrastructure, and different buyer incentive structures — forcing Saudi Arabia to simultaneously manage dollar-market credibility for Western institutional investors while maintaining yuan-corridor competitiveness for its largest volume customer.

How to avoid the ‘The Yuan Liquidity Trap’

Saudi-China bilateral trade reached $107.53 billion in 2024 — China's exports to the Kingdom totalling $50.05 billion against imports of $57.48 billion, predominantly crude oil.

This already surpasses Saudi Arabia's combined trade with the EU $75 billion and the United States $26 billion.

Saudi Arabia sells China roughly $57 billion worth of oil each year, and buys back roughly $50 billion worth of Chinese goods — machinery, electric vehicles, steel, and construction equipment.

The gap between the two figures is only $7.4 billion, which by the scale of a $107 billion trading relationship is remarkably small.

If Saudi Arabia agrees to accept payment for its oil in yuan rather than dollars, it does not end up sitting on a pile of Chinese currency it cannot use.

It can spend almost all of it immediately on Chinese imports it was already buying anyway to avoid what economists call ‘the Yuan liquidity trap.’

The second path to avoid the ‘yuan liquidity trap’ focuses on reinvestment. Saudi Arabia can buy Chinese government bonds.

Rather than holding idle yuan balances — which earn nothing and carry conversion friction — Riyadh parks them in Chinese government bonds earning today around 2%, with sovereign-grade security.

The yuan stays productive without leaving the Chinese financial system, which Beijing actively encourages. The risk, however, is that those returns — even at 2% — remain well below what Saudi Arabia earns deploying capital into Western private equity or infrastructure.

The yield on US 10 Year Note Bond Yield held steady at 4.38% on May 1, 2026.

The bond market offers stability and yuan utility, but not the growth returns Vision 2030's financing ambitions ultimately require. It is a treasury management tool, not a wealth generation strategy.

The BIS mBridge project, joined by SAMA in June 2024, is another option. It is a multi-central bank digital currency system enabling real-time, peer-to-peer cross-border payments without passing through traditional correspondent banking infrastructure.

The platform's other full participants include the People's Bank of China, the Hong Kong Monetary Authority, the Central Bank of the UAE, and the Bank of Thailand.

The mBridge allows Saudi Arabia to receive yuan payments for oil directly from Chinese banks without routing through dollar-based correspondent banking — meaning no US clearing infrastructure, no SWIFT messaging, and no dollar conversion required.

✧ Concluding remarks: The key risk ✧

Yuan settlement offers Saudi Arabia a genuine efficiency gain within its China trade corridor — but one that requires careful calibration. Saudi Arabia must strictly protect its traditional financial safety limits.

Keeping enough US dollars to maintain the riyal-dollar peg is the most vital goal. This fixed exchange rate provides the basic trust that foreign investors need.

The distinction between pragmatic bilateral adjustment and broader currency policy shift may seem technical, yet global capital markets are acutely sensitive to such signals.

The riyal peg to the dollar, fixed at 3.75 since 1986, functions as far more than an exchange rate mechanism. It is effectively a sovereign credibility contract with global capital markets.

With SAMA holding $415 billion in net foreign assets — 187% of the IMF's reserve adequacy metric — the peg is mechanically defendable. The risk is not arithmetic. It is behavioural.