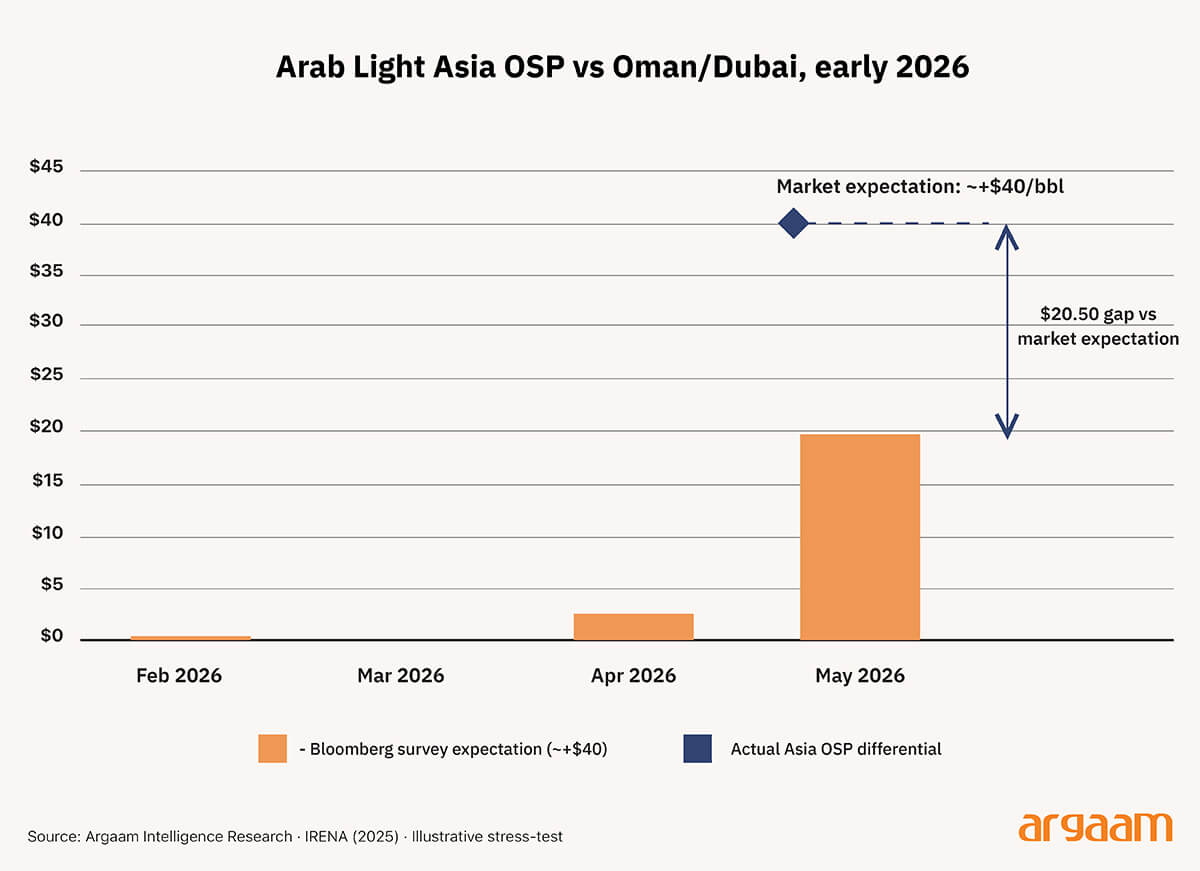

On April 6, Saudi Aramco set its Official Selling Price differential for Arab Light crude destined for Asian buyers at +$19.50 per barrel above the regional benchmark.

A Bloomberg survey of market participants, published seven days earlier, had established a pre-announcement consensus of approximately +$40 per barrel. The gap between the two numbers — $20.50 per barrel — is the starting point for this analysis by Argaam Intelligence.

At the volumes Saudi Arabia moves to Asia monthly, a $20.50 per barrel deviation from market consensus is not a pricing adjustment. It is a policy signal. The question this paper addresses is what that signal means, and for whom.

Aramco does not sell at a single world price. Its pricing architecture is regional — a monthly differential applied above a location-specific benchmark, set unilaterally by Aramco and absorbed by long-term contract buyers.

The regional benchmarks are straightforward: the average of Oman and Dubai crude assessments for Asia, ICE Brent for Northwest Europe, and the Argus Sour Crude Index for the United States. These benchmarks float with the market. The differential — the OSP — is what Aramco controls.

What the $20.50 Gap Actually Represents

The $20.50 figure requires precise framing to avoid misinterpretation. It is not a discount in the conventional sense. It is the distance between Aramco's chosen differential and the differential that prevailing spot market conditions would have supported.

The Bloomberg consensus of $40 per barrel reflects what traders and refiners believed Arab Light was worth on the open market at that moment — the price a buyer without a long-term contract would have paid for equivalent crude.

Aramco charged $20.50 less per barrel than the market said it could have. That gap did not disappear — it moved. Instead of flowing to Aramco as revenue, it stayed with Asian refineries as savings.

At the volumes Saudi Arabia ships to Asia every month, that is not a small concession. It is a deliberate decision to leave hundreds of millions of dollars on the table — and when a company with Aramco's pricing power does something like that, the reason is never simple generosity.

It represents a calculated repositioning within the geography of global crude flows — one whose internal logic is rooted in arbitrage mechanics rather than diplomatic signalling or production politics.

How the Arbitrage Mechanism Works: A Numeric Architecture

Aramco's monthly pricing system is not simply about setting a number. It is a carefully calibrated tool for extracting the maximum possible revenue from three structurally different buyer markets — Asia, Europe, and the United States — without pushing any of them to the point where they stop buying. What happened in May 2026 illustrates that logic.

Aramco prices Arab Light against different benchmarks in different regions. That single fact produces dramatically different revenue outcomes depending on where the crude is heading — not because Aramco charges different rates of generosity to different customers, but because the benchmarks themselves had diverged sharply.

In May 2026, the Oman/Dubai benchmark — the reference point for Asian buyers — had surged to approximately $170 per barrel. ICE Brent, the European reference, was trading at around $110.

That $60 gap between the two benchmarks was not normal. It reflected an acute supply disruption: when Hormuz-loading cargoes were suspended from the standard pricing mechanism, Gulf sour crude grades became artificially scarce in the assessment process, driving Oman/Dubai to an unusually high premium over Brent.

The result was that Asian buyers faced a landed cost of approximately $193 per barrel for Arab Light, while European buyers paid roughly $142 per barrel for the same crude.

That $50 difference was not a separate pricing decision by Aramco. It was simply the mechanical consequence of two benchmarks moving in opposite directions during a period of regional supply stress.

ℹ︎

◆ Note ◆ It should be noted that Bloomberg survey expectations reflect estimates from analysts and traders, not an official benchmark price or a contractually verifiable figure. The $20.50 gap should therefore not be read as a confirmed concession on Aramco's part, but rather as the distance between Aramco's actual pricing decision and the prevailing market expectations ahead of the announcement.

ℹ︎

◆ PS ◆ In this chart Those near-zero differentials mean that in February and March, Aramco was pricing Arab Light at almost exactly the same level as the Oman/Dubai benchmark — with virtually no premium on top. In March it was charging precisely par — not a cent above the benchmark. That is historically very low. And it tells us something important about market conditions in those months before the sharp move in May.

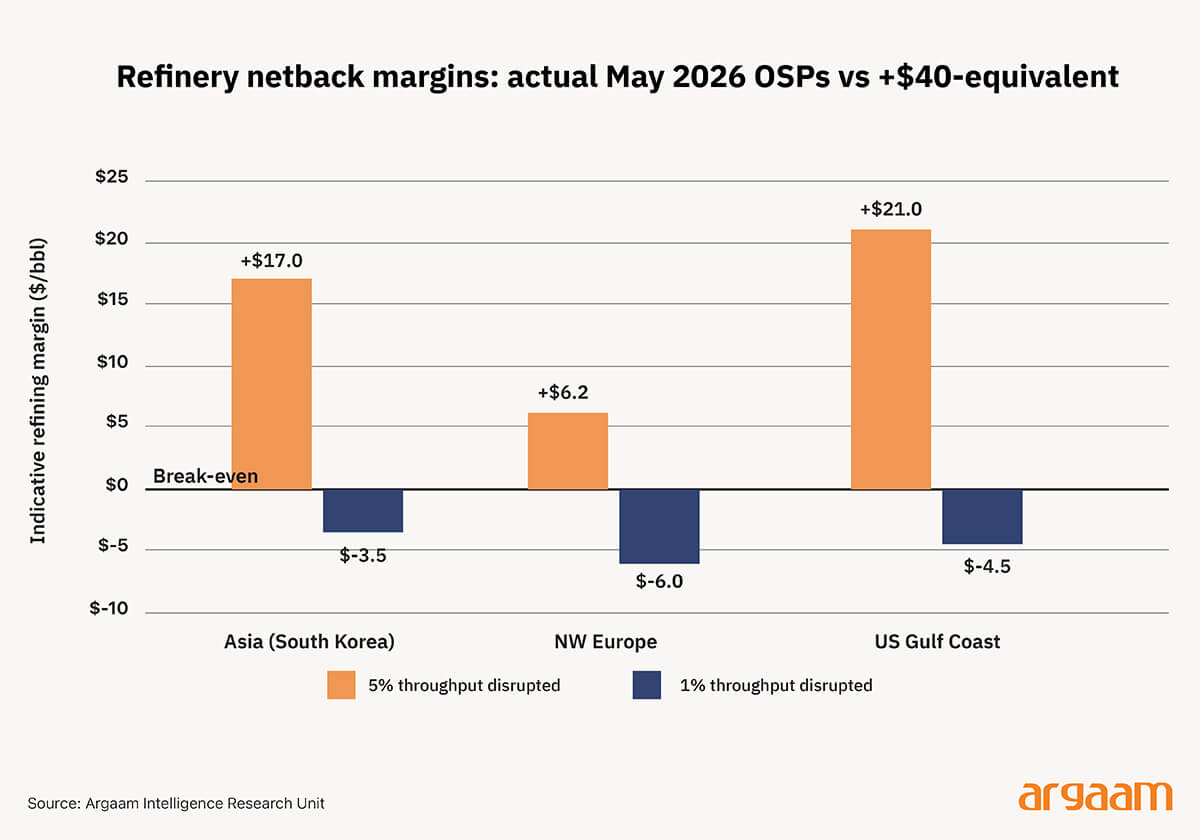

The Price That Keeps Refineries Running

The more analytically significant question is not what Aramco charged, but how close that charge came to the point where buyers would have stopped buying altogether.

This is where refinery economics become decisive. A refinery does not buy crude as an act of loyalty. It buys crude when processing that crude generates a positive margin — meaning the value of the refined products it produces exceeds the cost of the crude it purchased. When that margin turns negative, the refinery stops ordering.

Let’s Consider each region in turn.

1) At Aramco's actual differential of +$19.50 over the Oman/Dubai benchmark of $170, plus approximately $3.50 per barrel in freight, a South Korean refinery faced a landed cost of around $193 per barrel.

Against an indicative product value — what jet fuel, diesel, and other refined outputs were worth at that moment — of approximately $210 per barrel, the refinery earned a margin of roughly +$17 per barrel.

2) Now apply the market consensus differential of +$40 instead. Landed cost rises to $213.50 per barrel — above the $210 product value. The margin turns negative at approximately −$3.50 per barrel.

At that point, the rational response for any refinery is not to absorb the loss. It is to stop taking the barrels.

3) The European refiner, priced against Brent at $110 with a differential of +$27.85, faced a landed cost of approximately $142 per barrel. Against a product value of around $148 per barrel.

The margin was approximately +$6 per barrel — thin, but positive. A uniform application of a $40-equivalent differential would have eliminated that margin entirely.

4) The American refiner, working off an ASCI benchmark of around $110 with a differential of +$14.60 and freight of $6.50 per barrel, faced a landed cost of roughly $131 per barrel.

Against a product value of approximately $152 per barrel, the margin was around +$21 per barrel — the healthiest of the three, with meaningful buffer against a differential increase.

ℹ︎

◆ Note ◆ These margins are calculated on fixed assumptions for freight costs and refined product prices — assumptions that are subject to change in a highly volatile market. The figures should therefore be read as indicative benchmarks for the direction of refining economics, rather than definitive measurements of the margin achieved by any individual refinery.

What This Tells Us About the $19.50

The $20.50 gap between what Aramco charged and what the market expected was not a concession to Asian buyers. It was the answer to a precise engineering question: what is the highest differential we can charge before Asian refineries stop ordering?

The answer in May 2026 was $19.50. One dollar higher and margins would have begun compressing toward zero. At $40, they would have turned negative and term-contract volumes would have collapsed — not through renegotiation, but through simple non-ordering.

Aramco did not leave $20.50 per barrel on the table out of goodwill. It left it there because charging it would have destroyed the demand it needed to move six million barrels a day.

The $19.50 was not the price Aramco wanted to charge. It was the highest price the market's refinery economics would actually bear.

Three Markets, Three Arbitrage Positions

Aramco doesn’t set a single OSP — it sets a portfolio of differentials, each calibrated to the competitive structure of a distinct regional market, and the May 2026 split is among the most analytically instructive in the history of the pricing system.

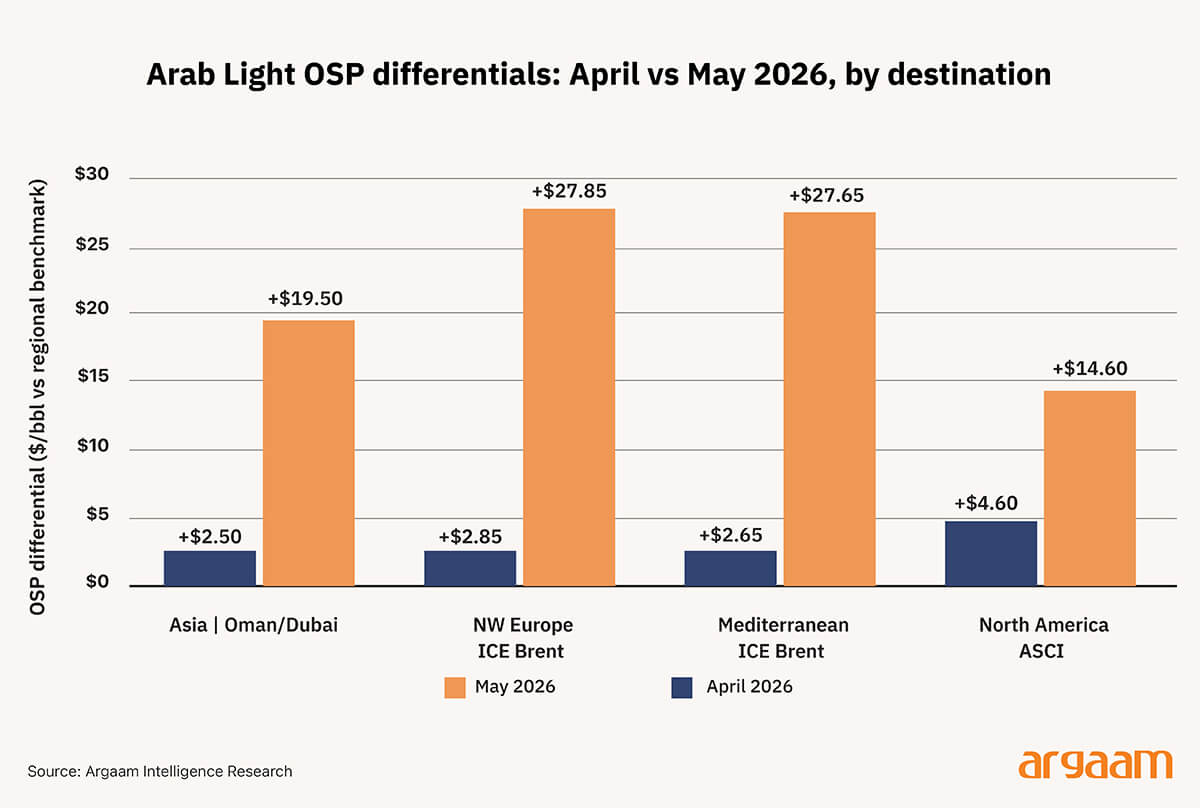

Asia received +$19.50 over Oman/Dubai — a $17 single-month increase from April's +$2.50, the largest one month jump in the history of the Arab Light Asia OSP, yet $20.50 below pre-announcement expectations.

Northwest Europe received +$27.85 over ICE Brent. And, North America received +$14.60 over ASCI — a roughly $10 increase that left US Gulf refiners with comfortably positive economics. The differential treatment isn’t arbitrary, it maps directly on to three structurally different competitive environments.

In North America, Saudi crude is a marginal supply source competing against US shale, Canadian heavy grades, and Latin American medium sours. The $14.60 ASCI premium maintains relationship contracts without seeking volume growth.

ℹ︎

◆ PS ◆ Northwest Europe and Mediterranean saw the largest absolute jumps, while North America saw the most modest increase — consistent with the US Gulf Coast's structurally more comfortable refinery margin position discussed earlier

In Europe, the structural reduction of alternative sour crude supply has created a captive premium environment; European refiners have fewer technical alternatives, and Aramco does accordingly extracts the highest absolute differential.

Asia is the volume backbone — term contract relationships with major Asian national oil companies are the foundation of Aramco’s long term revenue base.

The $19.50 is the level that balances higher returns from Asia with the need to keep buyers lifting barrels - it marks the practical ceiling for the OSP in May, not a cut price offer.

The execution risk embedded in this decision materialised within days. When Brent softened from around $110 toward the low $90s following ceasefire reports in early April, the fixed May OSP sat above a spot market that had moved sharply lower.

Saudi crude shipments to China halved to approximately 20 million barrels — the lowest on record — as buyers found ESPO Blend $16–22/bbl cheaper on a delivered basis.

This didn’t invalidate the arbitrage logic of the original decision, it showed that even at +$19.50 the decision carried execution risk, and that a +$40 OSP would likely have caused much more severe and prolonged damage to term contract relationships.