BinDawood Holding's recent acquisition of a 51% stake in Vaza Food Company for SAR 217.9 million was driven above all by the nature of a business model that has not merely grown quickly, but has sustained margins that outpace most of the established players in the food sector.

This combination is rare in the industry. Rapid growth typically comes at the expense of profitability — yet Vaza has expanded at pace while maintaining a net margin more than double the sector average. That is not a coincidence. It is a signal of genuine pricing power, as the numbers in this Argaam Intelligence analysis will show.

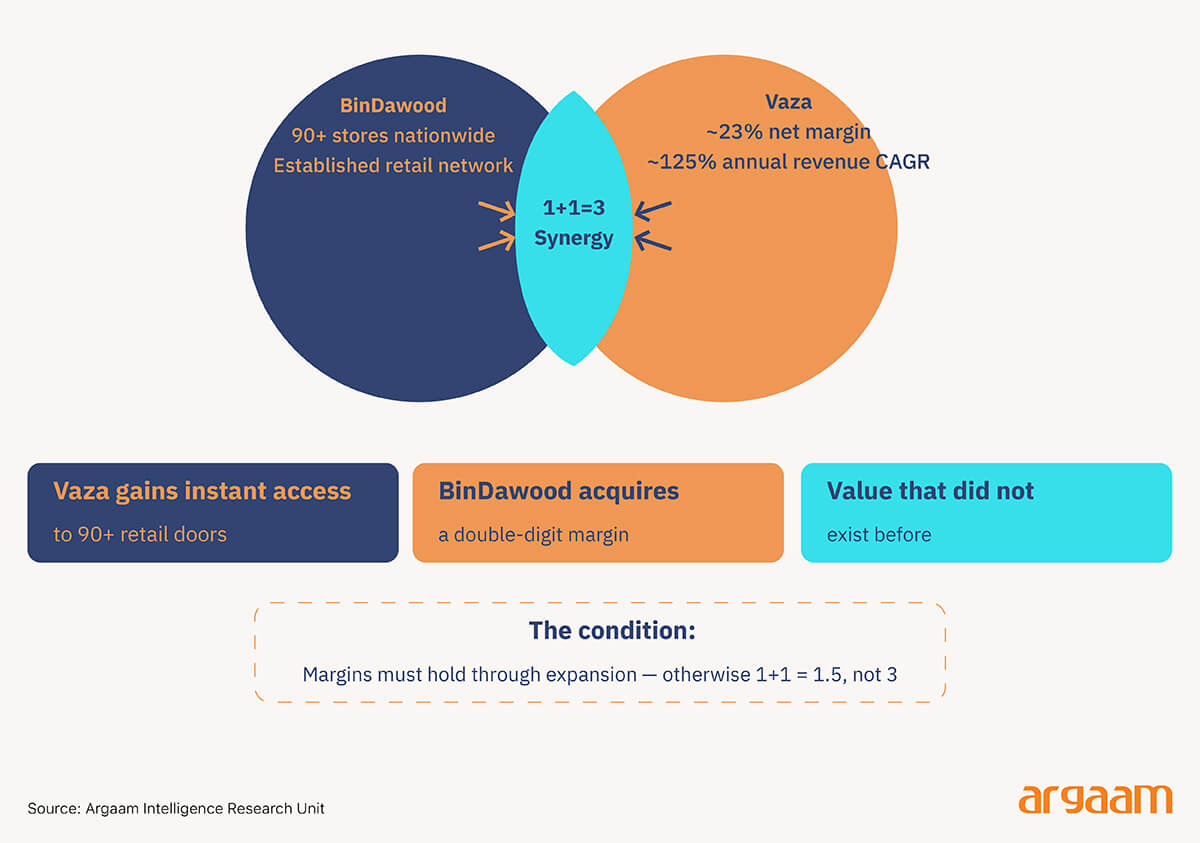

This is where the real value of the acquisition lies. BinDawood is not buying scale — it is buying a differentiated, high-margin business model and a recognised brand in the premium gifting confectionery market, and handing it a distribution platform capable of multiplying its reach.

If this equation succeeds in growing revenues without eroding margins, the deal will look considerably cheaper in the future than its headline price suggests today. That is precisely the bet BinDawood is making.

Vaza holds a premium product and a strong margin but lacks the breadth of distribution to realise its full potential. BinDawood holds the network but needs a product with higher value-add. Together, they give Vaza access to a customer base far larger than it could have reached alone.

Saudi Arabia ranks among the most significant markets for gifting confectionery and bakery products in the region — and it is a market where price plays a secondary role in the purchase decision.

What drives the consumer is brand, packaging, and perceived quality. In a market structured this way, the premium player with the widest shelf presence wins. That is the logic this deal is built on.

Positioning Vaza Food Company in the context of broader industry

Vaza operates within a premium and specialty segment of Saudi Arabia’s broader food and beverage market (~$35–40bn in 2025, based on industry estimates from sources such as Euromonitor and Statista), specifically across confectionery, bakery and gifting-driven consumption occasions.

The Saudi confectionery market is estimated at ~$1.7–1.9bn, of which chocolate represents a core ~$1.2–1.3bn segment, while adjacent categories such as cakes and pastries (~$1.2–1.4bn) and broader bakery (~$5bn+, based on Mordor Intelligence and industry reports) expand the relevant TAM for Vaza.

A significant share of demand within these markets is tied to gifting occasions, an area where Saudi Arabia represents one of the largest markets in the region. The gifting market typically offers higher value capture, driven by lower price sensitivity and a greater emphasis on brand, packaging, and perceived quality.

More broadly, this reflects a wider shift across food retail, where value is increasingly concentrated in premium, branded and experience-led segments rather than commoditised categories.

Vaza Food is well positioned to continue capturing market share, particularly when scaled through BinDawood Holding’s network, which can amplify visibility, merchandising capabilities, and route-to-market reach.

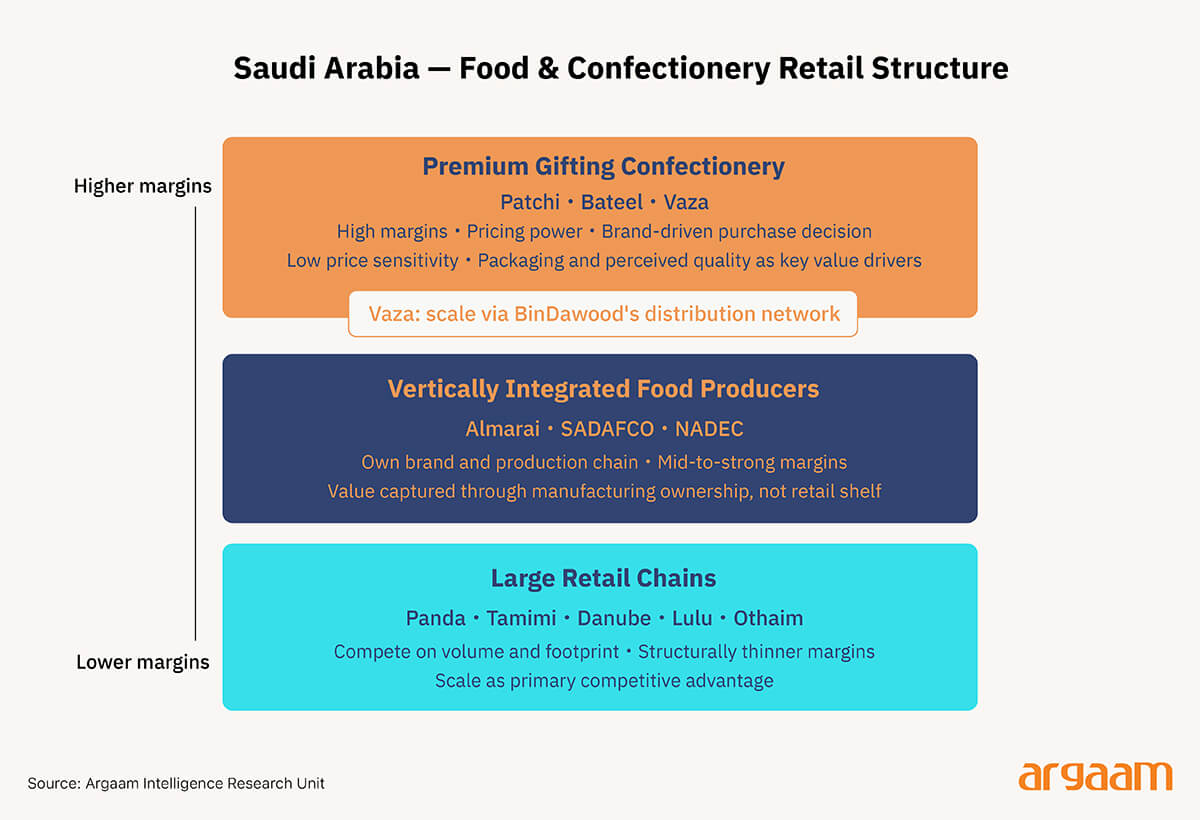

The Saudi food retail and confectionery market is broadly split between large-scale grocers such as Panda, Tamimi, Danube, Lulu and Othaim, which compete on scale but operate on structurally thinner margins, and vertically integrated branded players like Almarai, SADAFCO and NADEC, which retain more value through ownership of production and brands.

A smaller premium segment sits with gifting-led confectionery brands such as Patchi and Bateel, with Bateel increasingly incorporating café-led formats alongside its core gifting business.

Vaza sits closest to this latter category, though it is not directly comparable to established players such as Patchi and Bateel. Those businesses are more scaled and brand-led, while Vaza remains earlier-stage and more sub-scale, with differentiation centred on distribution-led scaling potential via BinDawood’s platform rather than standalone brand scale at this stage.

A Highly Attractive Financial Profile

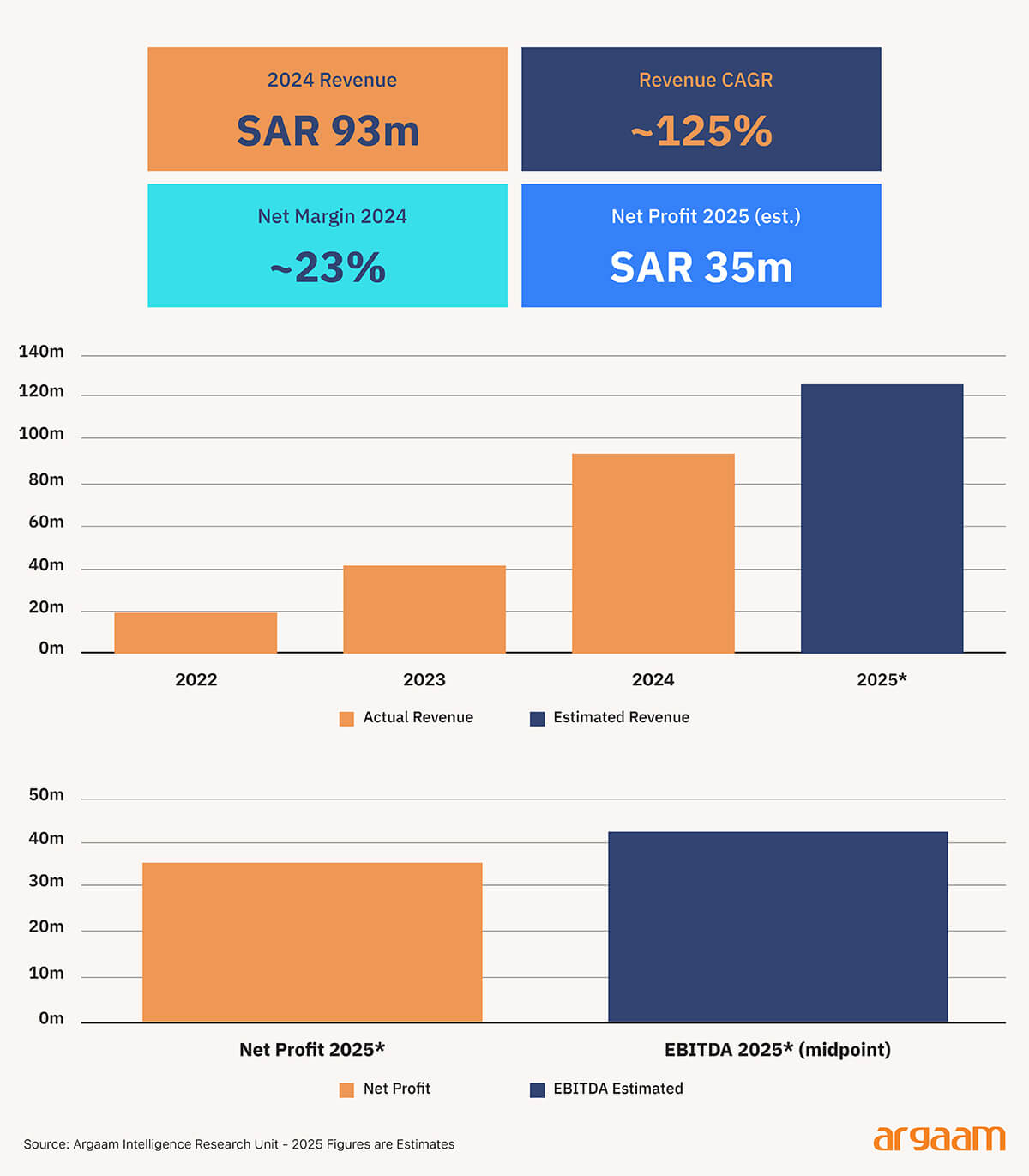

Vaza Food Company has delivered strong growth, with revenue increasing approximately fivefold between 2022 and 2024, reaching approximately SAR 93 million in 2024 (CAGR of ~125%).

This has been primarily driven by rapid store rollout and increasing brand penetration across the premium confectionery and gifting segments, with growth significantly outpacing larger, more mature food and confectionery players in the Saudi market.

Net profit margins have historically been in the range of ~22–32% (~23% in 2024), meaningfully above traditional food and beverage peers. For context, regional listed players such as Almarai (~10–12%) and SADAFCO (~13–16%) operate at lower margin levels (based on latest publicly disclosed financials).

Whilst detailed cost information is not disclosed, these elevated margins likely reflect a premium gifting-led product mix, a favourable gross margin structure, and an advantageous channel mix. However, given the early-stage nature of the business, parts of the cost base may not yet be fully normalised and may evolve as the business continues to scale.

Estimating 2025 Revenue and EBITDA for valuation purposes

Argaam Investments estimates net profit of ~SAR 35 million in 2025 (unaudited), implying continued strong growth supported by both revenue expansion and margin progression.

Based on historical margins in the range of ~22–32%, and assuming a normalised 2025 net margin of ~26–30%, this implies revenue in the range of ~SAR 115–135 million.

EBITDA has not been disclosed. Based on Argaam Investments’ estimated 2025 net profit of ~SAR 35 million, EBITDA is approximated by adjusting for tax, interest, and depreciation and amortisation under the Saudi Zakat and tax framework.

Assuming predominantly Saudi/GCC ownership (tax burden expected to be primarily Zakat based, resulting in a low effective tax rate with minimal corporate income tax impact), limited leverage, and modest depreciation, EBITDA is likely in the range of ~SAR 38–45 million.

This implies EBITDA margins in the low-to-mid 30s, consistent with a premium, brand-led model with higher value capture at the retail level rather than wholesale distribution. This should be viewed as a directional estimate given limited disclosure granularity.

Implied Valuation and Peer Benchmarking

BinDawood acquired a 51% stake for SAR 217.9m, implying an equity valuation of approximately SAR 427m. No earn-out or contingent consideration has been disclosed, suggesting a clean upfront transaction structure.

In the absence of detailed balance sheet disclosure, equity value is used as a proxy for enterprise value.

Based on an enterprise value proxy of ~SAR 427 million and estimated 2025 revenue of ~SAR 125 million (midpoint of the implied range), the transaction implies an EV/revenue multiple of approximately ~3.4x (~4.6x on 2024 revenue).

Using estimated 2025 EBITDA of ~SAR 38–45 million, this implies an EV/EBITDA multiple of approximately ~10x–11x (~13x–14x on 2024).

Whilst there is no perfect comparable, Saudi listed food companies typically trade in the range of ~1.0x–2.5x revenue and ~9x–13x EV/EBITDA (based on current market trading ranges and consensus data), reflecting mature, scaled businesses with stable but lower growth profiles.

Within this, market leaders such as Almarai (~2.5x revenue) and SADAFCO (~2.1x revenue) sit at the upper end of the range (Bloomberg consensus / company filings).

In comparison, listed premium international players such as Lindt & Sprüngli and Mondelez International typically trade at higher multiples of (~2.5x–4.0x revenue and mid-to-high teens EV/EBITDA), reflecting stronger brand equity, international reach, pricing power and exposure to higher-margin categories including confectionery and gifting.

On this basis, Vaza appears positioned between the two universes: above domestic Saudi food retail benchmarks, but below fully scaled global branded consumer platforms. Whilst disclosed deal multiples in the GCC remain limited, available precedent transactions still provide a useful directional framework.

Distribution-led transactions such as The Chefs’ Warehouse’s acquisition of Chef Middle East point to materially lower valuation levels, with implied multiples of roughly ~0.6x revenue and ~7x–9x EBITDA based on disclosed purchase price and management guidance.

By contrast, branded consumer platforms sit higher on the range: Agthia Group’s acquisition of Abu Auf was explicitly structured at no more than ~12x EV/EBITDA, reflecting stronger brand equity, pricing power and growth.

✧ Concluding Thoughts ✧

Overall, while the transaction implies a clear premium to domestic Saudi food retail benchmarks, the multiple appears broadly justified when viewed through the lens of Vaza’s positioning, growth profile and high margin, gifting-led category-mix.

The business combines above-market growth with structurally higher margins, driven by strong pricing power and a differentiated gifting-led proposition that enables greater value capture at the retail level than traditional distribution-led food businesses.

This supports a re-rating versus domestic peers, where valuations are anchored to lower-growth and lower-margin retail economics. At the same time, while it does not fully exhibit the scale, diversification, or international footprint of global branded consumer platforms, its economics and category exposure place it closer to the lower end of that peer group than to regional retail benchmarks.

As a result, the implied valuation sits comfortably within a mid-point between these two universes, rather than representing a clear outlier on either relative or absolute grounds.

The acquisition of a controlling stake likely reflects both a control premium and revenue synergies from scaling Vaza through BinDawood’s established distribution and retail footprint.

While early-stage execution and margin normalisation risks remain, the current profitability profile suggests these are not near-term constraints to the investment case, with potential for further margin expansion. Sustaining premium positioning during rapid expansion will be a key determinant of long-term value creation.