Africa's fuel retail market offers what Saudi investors find rarely in mature regions: rising fuel consumption, young populations, and an EV market that, despite high forecast growth, starts from such a low base that ICE fuel demand is likely to remain dominant for the next 15–20 years.

For Saudi Arabia, which is expanding its downstream and fuel retail footprint, this is a natural geography to explore.

Among Africa’s larger markets, South Africa, Kenya and Morocco stand out as initial candidates. Measured against criteria most relevant to Saudi investors — currency stability, fuel demand, the middle class, fuel pricing policy, and EV adoption — Morocco offers the most coherent and balanced mix.

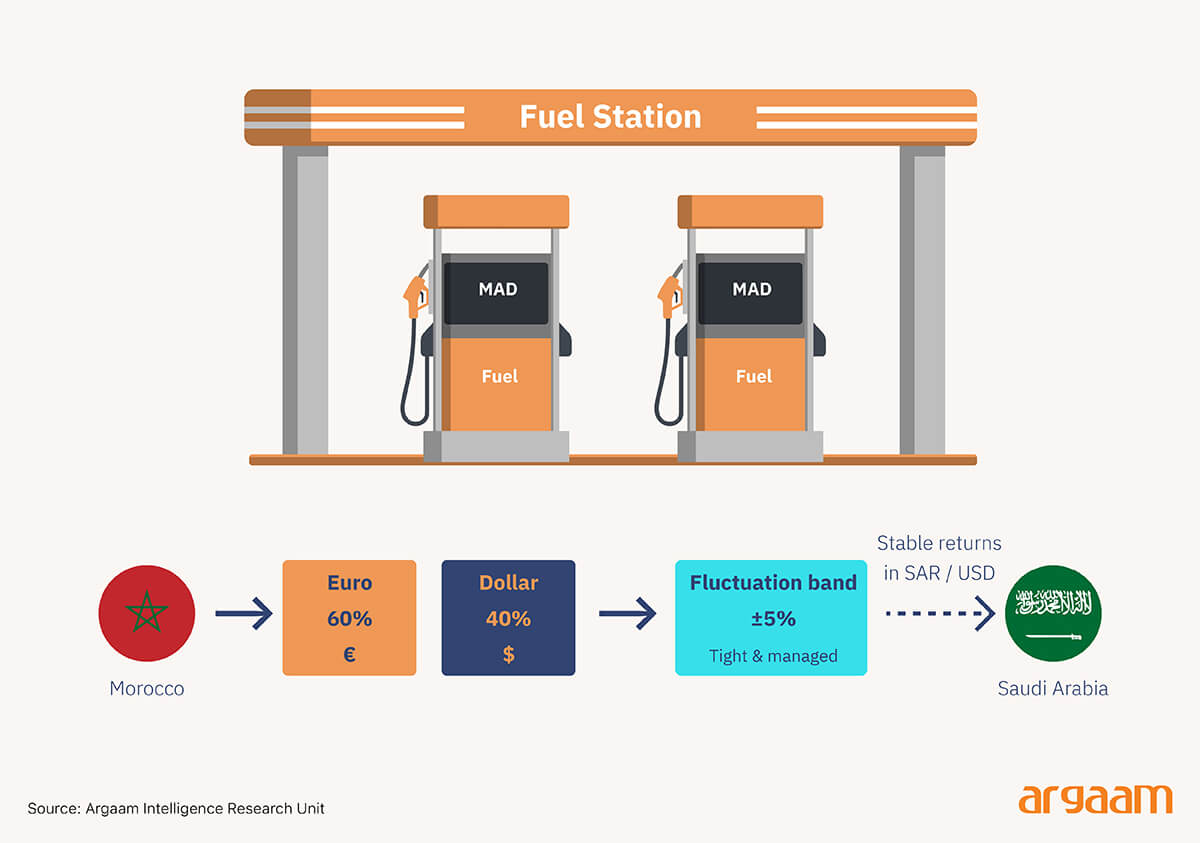

Currency factor: why Morocco’s FX regime suits long term Saudi capital

For Saudi investors, returns are ultimately measured in SAR and USD. A market where the local currency witnesses frequent, sharp depreciation can undermine an otherwise attractive business. In this respect, Morocco’s FX regime is favourable comparatively.

The Moroccan dirham is managed against a currency basket dominated by euro and US dollar - within a defined fluctuation band (managed against a 60% EUR / 40% USD basket within a ±5% fluctuation band).

IMF assessments highlight Morocco’s very strong macroeconomic policies and institutional policy frameworks and this country continues to qualify for a Flexible Credit Line – which’s granted only to economies with robust fundamentals.

The dirham’s traded in relatively narrow range versus USD in recent years, in sharp contrast to South African and Kenyan currencies - both experienced significant bouts of depreciation and volatility.

For long life assets such as service stations, depots and non fuel retail, this lower FX noise supports more predictable planning, hedging and profit repatriation over a 15–20 year horizon, rather than returns being at mercy of sharp currency swings.

Morocco’s also preparing a carefully sequenced shift toward inflation targeting regime from 2027 - with 2026 as pilot year, while maintaining the current exchange rate peg for now. IMF assessments and Bank Al Maghrib emphasise this transition is being undertaken from position of strength and with clear safeguards, which should keep FX volatility manageable, rather than disruptive for long term investors.

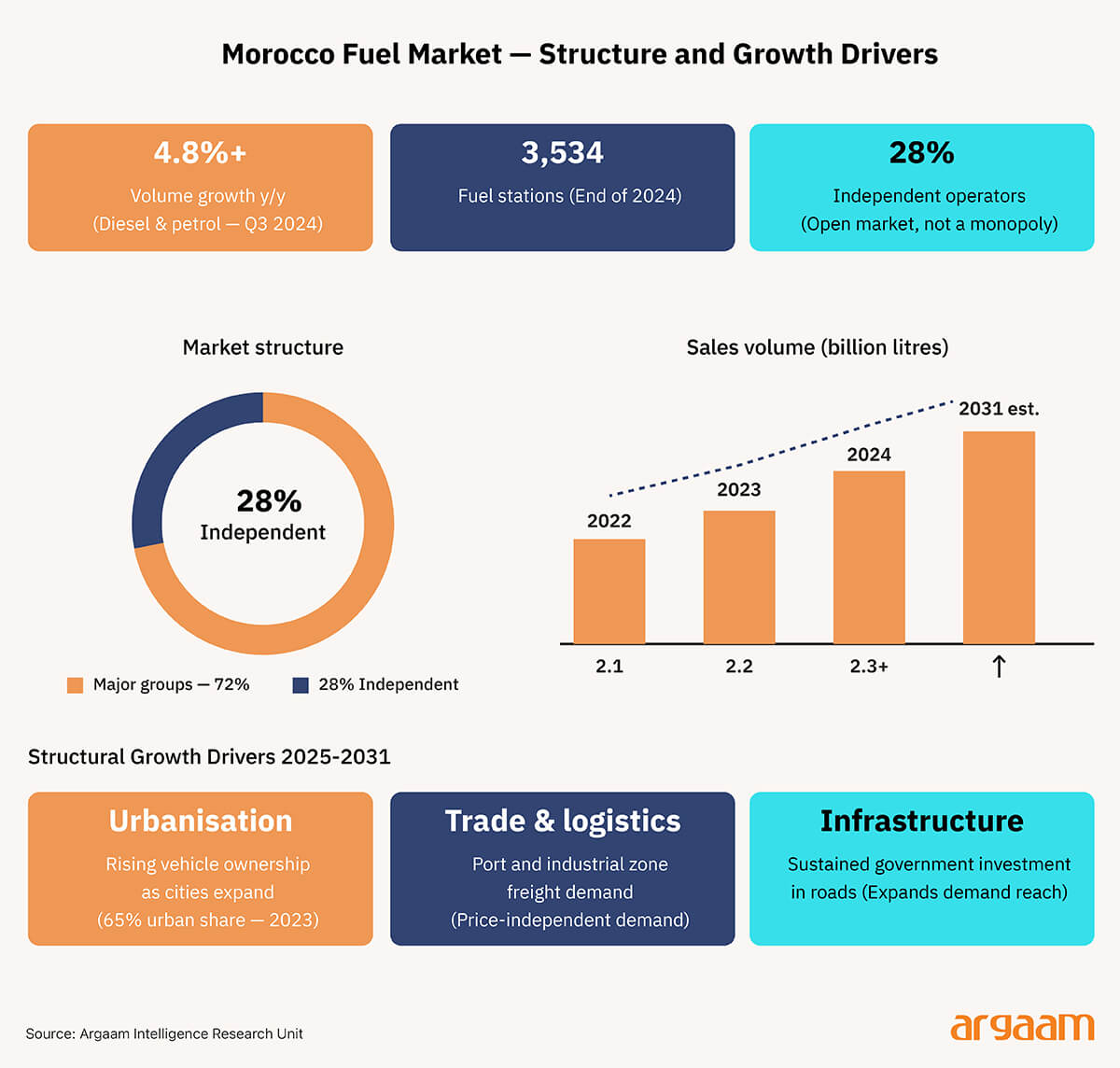

Fuel demand and market structure

Fuel retail economics depend both on volume and quality of underlying demand. Morocco’s fuel market demonstrates mix of rising sales and diversified customer base that supports Saudi interest.

In Q3 2024, even as revenues for the nine largest distributors fell on lower global oil and fuel prices, diesel and gasoline sales volumes rose 4.8% y/y to over 2.3 billion litres.

By end 2024, the fuel station network had grown to 3,534 outlets, with 28% operated by smaller independent companies — sign of an active, evolving market, not a closed oligopoly, even though top nine still dominate sales by value.

Industry outlooks (2025–2031) points towards continued growth in Morocco's fuel station and retail fuel market - driven by urbanisation, rising vehicle ownership, infrastructure investment, which sustains a multi-decade runway aligned with 15–20-year investment horizon Saudi capital would be underwriting.

Morocco's fuel consumption is diversified across private urban vehicles, inter city transport, trade logistics, tourism, rather than tied to a single commodity sector.

For Saudi investors, that diversification – combined with demonstrable growth in volumes and an expanding station network – makes the market structurally attractive even if it’s smaller than South Africa’s.

Market-based pricing: what it actually means for the investor

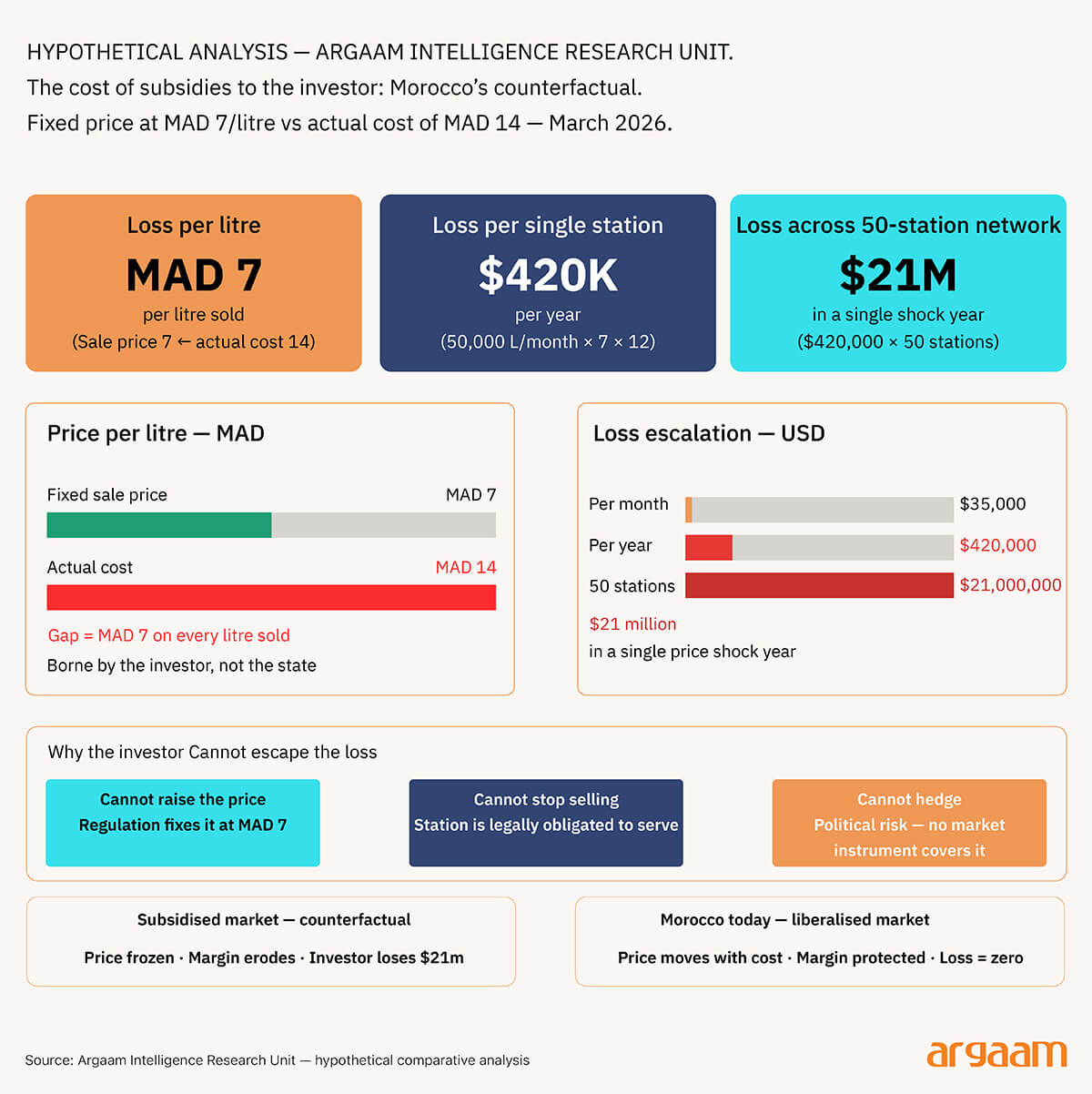

To understand the true significance of Morocco's fuel price liberalisation since 2014, it is not enough to say that prices "follow the market." What matters is how this mechanism plays out in practice, and what it means specifically for the foreign investor.

In mid-March 2026, two weeks into the Iran-US-Israel war, fuel prices in Morocco rose by approximately 13.9% in a single month. Diesel climbed by around two dirhams per litre and petrol by roughly 2.4 dirhams, with pump prices in most cities reaching between MAD 13 and MAD 14 per litre — equivalent to approximately $1.30 to $1.40 at the current exchange rate.

That sharp and rapid rise was painful for the Moroccan consumer. But for the fuel retail investor, it was precisely the opposite: a natural reflection of market logic that protected operating margins rather than eroding them.

In a liberalised market like Morocco, a fuel station operator works to a margin defined by the spread between the wholesale purchase price and the retail sale price.

When petrol reached MAD 13–14 per litre in March 2026, distributors adjusted their prices in line with international benchmarks, and that adjustment flowed through automatically to the pump.

The operator did not have to wait weeks for a government decree authorising a new price. Nor was the operator forced to sell fuel below its actual cost.

The counterfactual makes the point plainly. Had Morocco maintained a government subsidy fixing the price at, say, MAD 7 per litre, the investor would have faced severe losses — as the hypothetical analysis below illustrates.

The operator cannot raise the price, because regulation locks it in. Cannot stop selling, because the station is legally obligated to serve the public. And cannot hedge financially, because the risk is not a market risk — it is a government decision, and no financial instrument covers that.

The EVs market

A central part of the investment question is whether EVs will erode fuel retail volumes within the investment horizon. Morocco is actively positioning itself as an EV manufacturing and battery supply hub, but domestic EV adoption is still at an early stage (Morocco is emerging as an EV producer before it becomes an EV consumer, with manufacturing scale outpacing domestic adoption).

Recent estimates suggest electric and hybrid vehicles account for 0.3% of Morocco’s total vehicle fleet (BMI's 2025–2026 'surge' forecast is measured off a ~0.3% fleet base, so rapid growth rates still leaves ICE vehicles dominant - in absolute terms), while passenger EVs made up 2.6% of new car sales in 2025, and public charging network totals roughly 300 charging points, concentrated in key cities such as Casablanca, Rabat and Marrakech.

Even optimistic scenarios for Africa's e mobility show gradual, not explosive, penetration through 2035, with internal combustion engines still dominating private mobility and road freight.

In practice, this means Morocco will witness gradual EV growth from a low base, driven partly by export oriented manufacturing and pilot domestic programmes, but not the rapid ICE displacement observed in developed economies.

For Saudi investors thinking in 15–20 year horizons, this implies a window extending through the mid-2040’s in which ICE based fuel retail remains central to mobility, even as EVs ramp up.

✧ Conclusion✧

When fuel retail is added to Saudi Arabia's investment map in Morocco, it does not arrive as an isolated new sector — it arrives as an additional layer in a strategic relationship that has been deepening for years.

The Kingdom is already a significant presence in Morocco across tourism, healthcare, renewable energy and textiles, with cumulative Saudi investment exceeding six billion dollars by early 2026.

An investor who already knows the market does not start from zero — and in a sector that demands precise familiarity with the regulatory environment, supply networks and institutional relationships, that prior knowledge is an advantage that cannot be easily replicated or priced.

But the case for entering fuel retail goes beyond completing an investment portfolio. A fuel station — when designed to Saudi operational standards — is not simply a pump and a payment terminal.

It is a strategic asset. And Morocco, as an Arab-African market sitting at the intersection of Europe, the Gulf and West Africa, offers a combination of structural attractions that few markets on the continent can match: a stable currency that protects returns at the point of repatriation, liberalised fuel prices that protect margins at the point of sale, diversified demand that protects revenues across economic cycles, and an EV transition timeline that protects the business model from early obsolescence.

That convergence of factors is rare. And it is rarer still in a market where the Saudi investor arrives not as a stranger, but as an established institutional presence with relationships already in place. |