Al-Mutaqadima Petrochemicals' results reflect a clear paradox. The pricing environment appears supportive — but this support is not fully translating into profits.

The problem is not demand, nor selling prices: it is the cost of reaching the market and sustaining operations. Hormuz disruptions did not halt sales, but they raised the cost of every ton sold and eroded the benefit of price improvement.

⁉️

What Actually Happened?

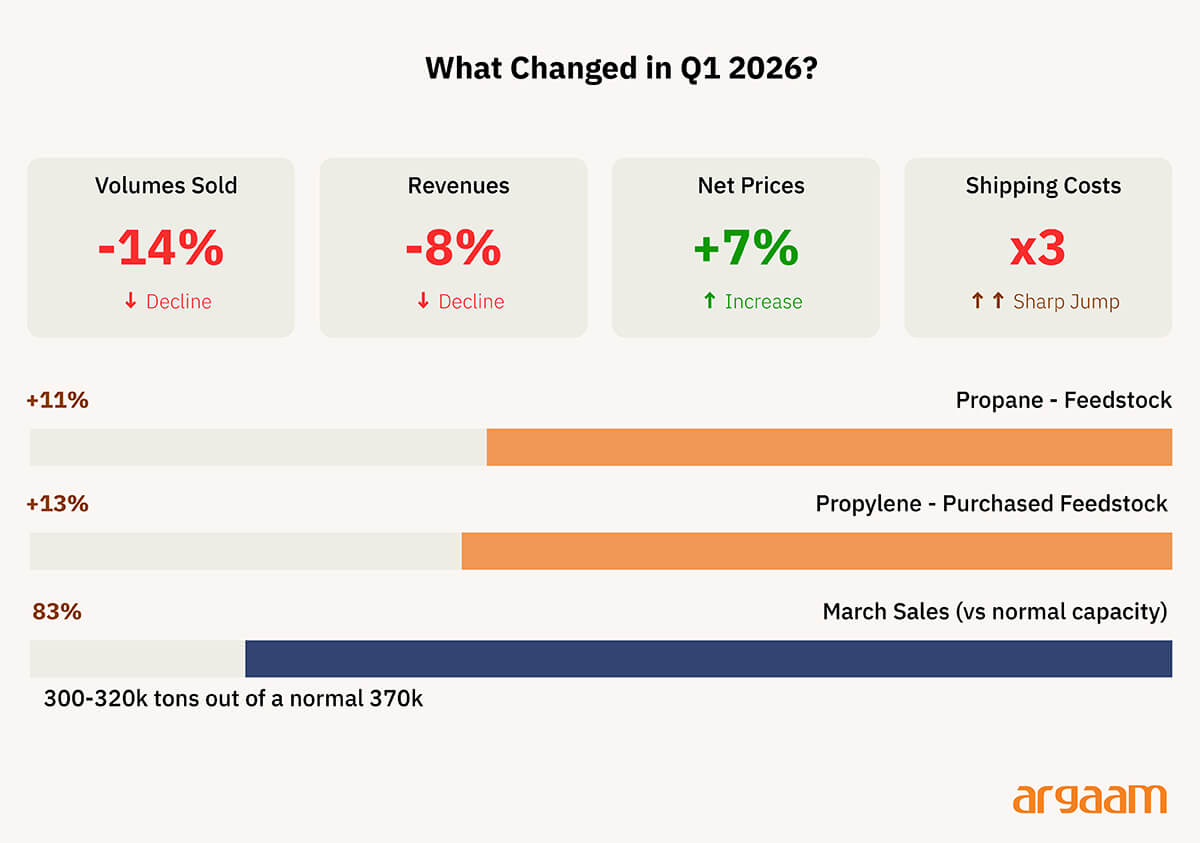

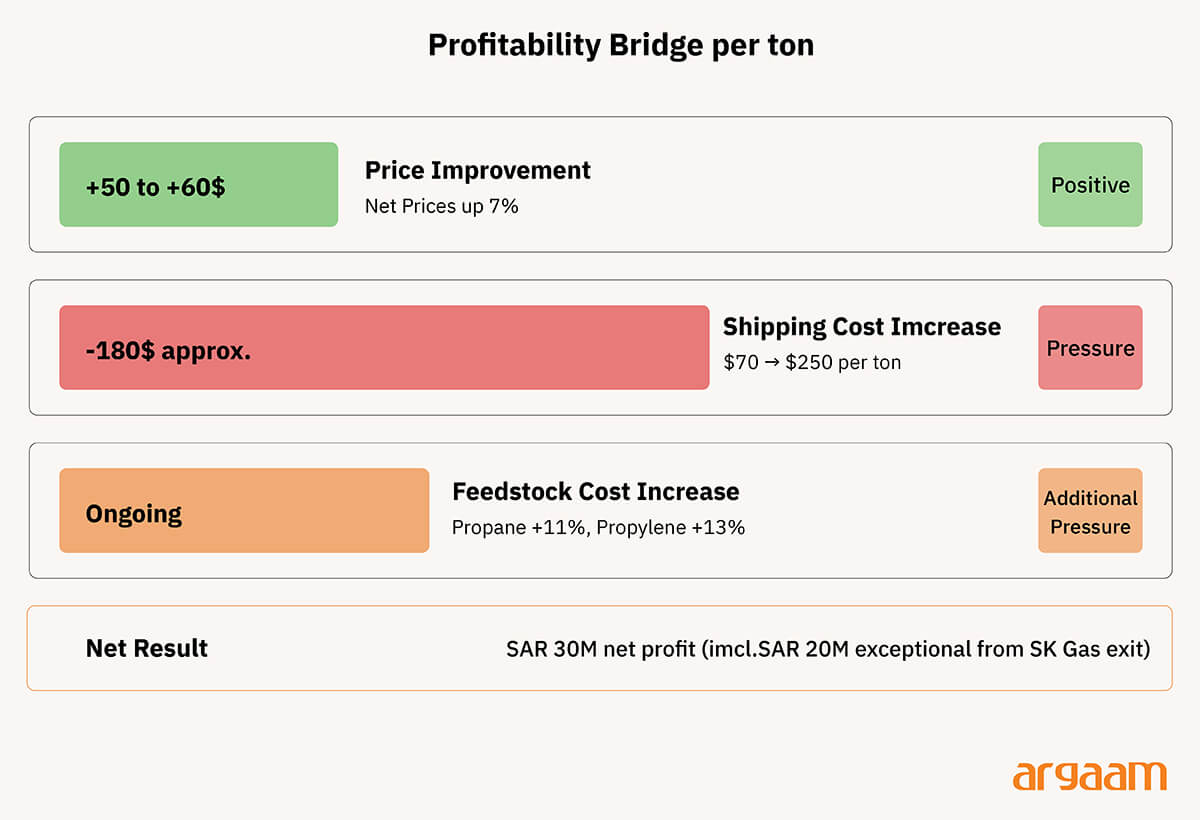

Revenues declined 8% quarter-on-quarter, driven by a 14% drop in volumes sold. Net prices improved 7%, and net profit reached SAR 30 million versus SAR 1 million in the prior quarter — but SAR 20 million of that figure came from an exceptional gain related to the exit from SK Gas.

The improvement in profit therefore does not reflect a full recovery in operations, but rather a combination of an exceptional gain and a partial improvement in costs.

Feedstock costs also increased: propane rose 11% and purchased propylene 13%. In March, sales reached 300–320k tons against a normal level of approximately 370k tons — roughly 80–85% of typical volumes.

💸

Why Don't Prices Convert to Full Profits?

ℹ︎

The current profitability equation can be simplified into three key components:

● Profitability = PP price spread over feedstock -shipping costs -impact of lower utilisation

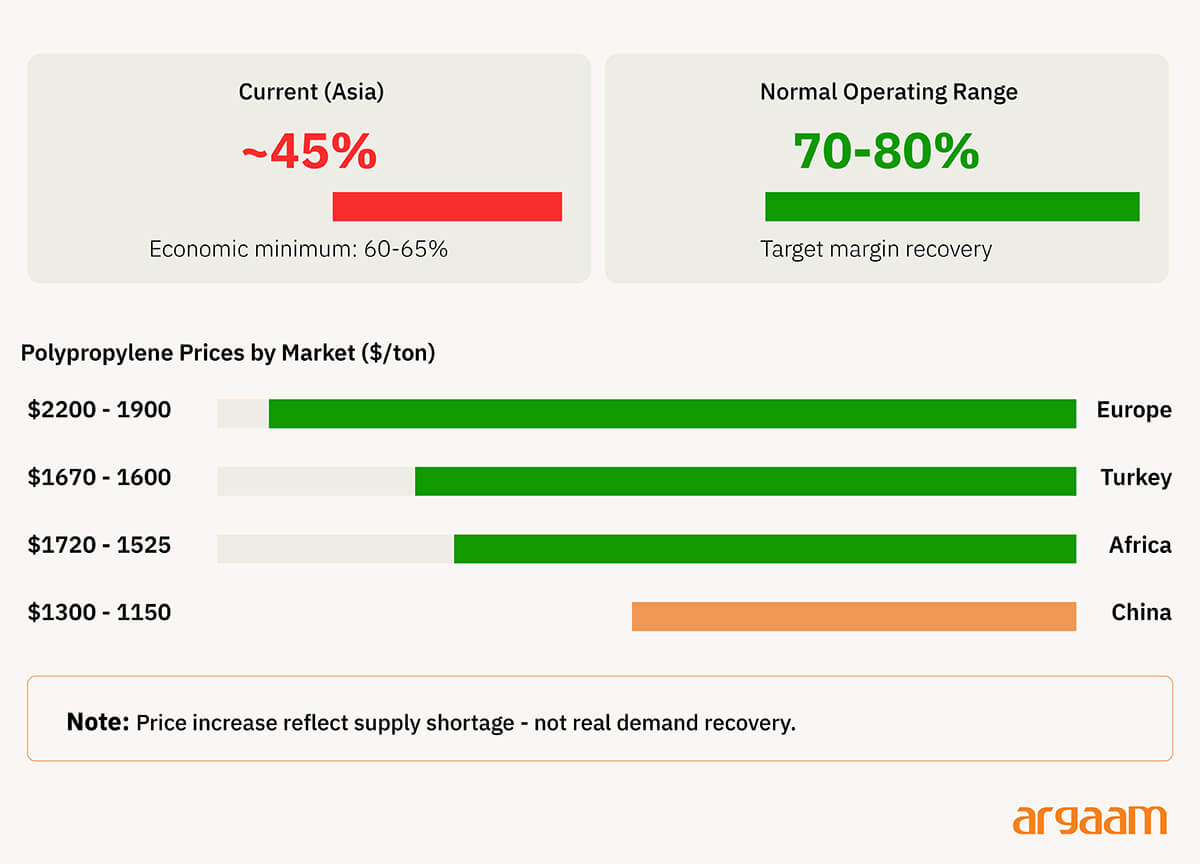

Prices have genuinely improved. Polypropylene is priced in Europe at $1,900–2,200/ton, Turkey at $1,600–1,670, Africa at $1,525–1,720, while China remains at lower levels of $1,150–1,300. The company noted margin improvements of approximately $50–60/ton versus March in its investor call.

But this improvement is offset by sharper cost pressure. Shipping costs have risen from $60–70/ton to levels reaching $250/ton — an increase alone sufficient to absorb most of the price gain.

Added to that is the rise in feedstock costs, making the net margin impact limited despite higher prices.

Put plainly: the market is offering a better price, but reaching that price has become more expensive.

🔦

Hormuz Strait Impact

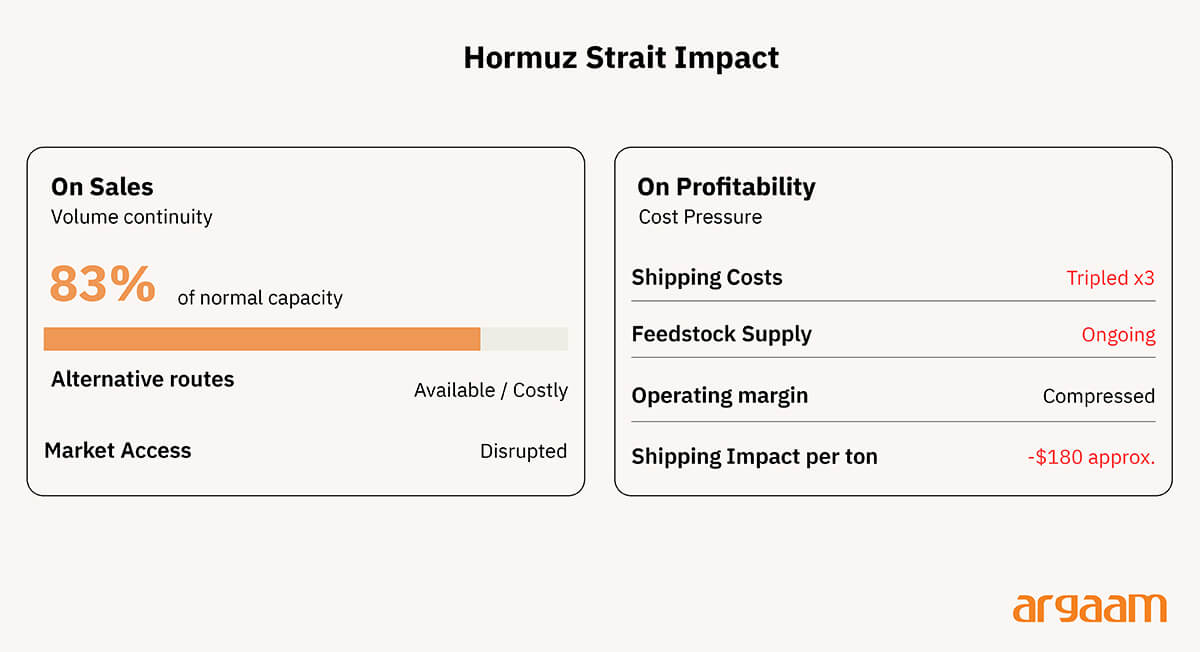

On sales, the company has not stopped selling — but it is operating below normal levels, at approximately 80–85% of usual capacity, using alternative routes and ports. This suggests demand remains intact, and the issue is not product placement.

On profitability, the impact is clear. Shipping costs rising to approximately $250/ton, combined with propane supply disruption, are squeezing margins simultaneously from both sides. The true impact of the Hormuz disruption was not on the ability to sell — but on the cost of reaching every ton sold.

🔍

Operational Manoeuvre: Containing Damage, Not Eliminating Its Impact

The company navigated disruptions through a mix of operational flexibility and priority realignment. It used alternative shipping routes across multiple ports to maintain sales flow despite higher costs.

It also brought forward part of the planned maintenance at APPC, capitalising on the period of partial downtime to reduce future shutdown durations.

Meanwhile, the APOC project remains in its operational ramp-up phase and has not yet reached full stability. This means any feedstock disruption during this phase has a proportionally larger effect on performance. Management nonetheless indicates gradual improvement as propane supplies begin to return and throughput rates rise.

📈

Global Market Conditions

ℹ︎

The market is not strong. The market is supply-constrained.

The current price improvement does not reflect a demand recovery — it reflects a supply shortage. Some Asian polypropylene plants have reduced utilisation rates to approximately 45%, versus a normal range of 70–80%, while the economic minimum for operations is 60–65%.

This means part of global production is running below economic viability — which is compressing supply and pushing prices higher on a temporary basis.

● Duration of Q2 production impact and how close it gets to a full month

● Shipping cost trajectory — whether it eases as routes stabilise

● Propane and propylene supply normalisation

● The company's ability to restore sales toward ~370k tons

🎯

Conclusion

Al-Mutaqadima is not facing a demand crisis — it is operating in an environment that does not fully reward higher prices. The ton is sold at a better price, but reaching it has become more expensive, feedstock is under greater pressure, and operations have not yet stabilised.

Q2 will therefore test not just prices — but the company's ability to convert prices into real operating profit.