A systematic review of TASI index data over recent years has surfaced a striking pattern, one that Argaam Intelligence believes warrants close analytical attention: the majority of cumulative returns do not accrue during official trading hours, but in the after-close period — between market close and the following session's open.

Intraday returns, by contrast, have been on average negative or negligible, while the after-close period consistently generates cumulative gains. This is not a random fluctuation, nor the product of exceptional short-term circumstances.

The pattern repeats with notable consistency across thousands of trading sessions, suggesting that structural factors are at work — factors that sustain and amplify it over time.

Understanding this pattern requires appreciating what makes TASI structurally distinct. The index is dominated by a group of large entities carrying significant market weight — institutions that combine substantial scale, long investment horizons, and advanced analytical and execution capabilities.

Together, these entities account for more than 64% of the index's total market capitalisation, a level of ownership concentration that naturally gives rise to pricing and liquidity dynamics that differ markedly from markets where ownership is more broadly distributed.

Additionally, TASI operates on a Sunday-to-Thursday trading week, creating a three-consecutive-day closure gap between the end of each week and the beginning of the next.

This gap carries significant analytical weight: geopolitical developments, oil price movements, and major government announcements accumulate over those three days before the market reconvenes.

These structural features together make TASI a natural environment for amplifying the after-close phenomenon — and understanding it is an analytical necessity, not an academic exercise.

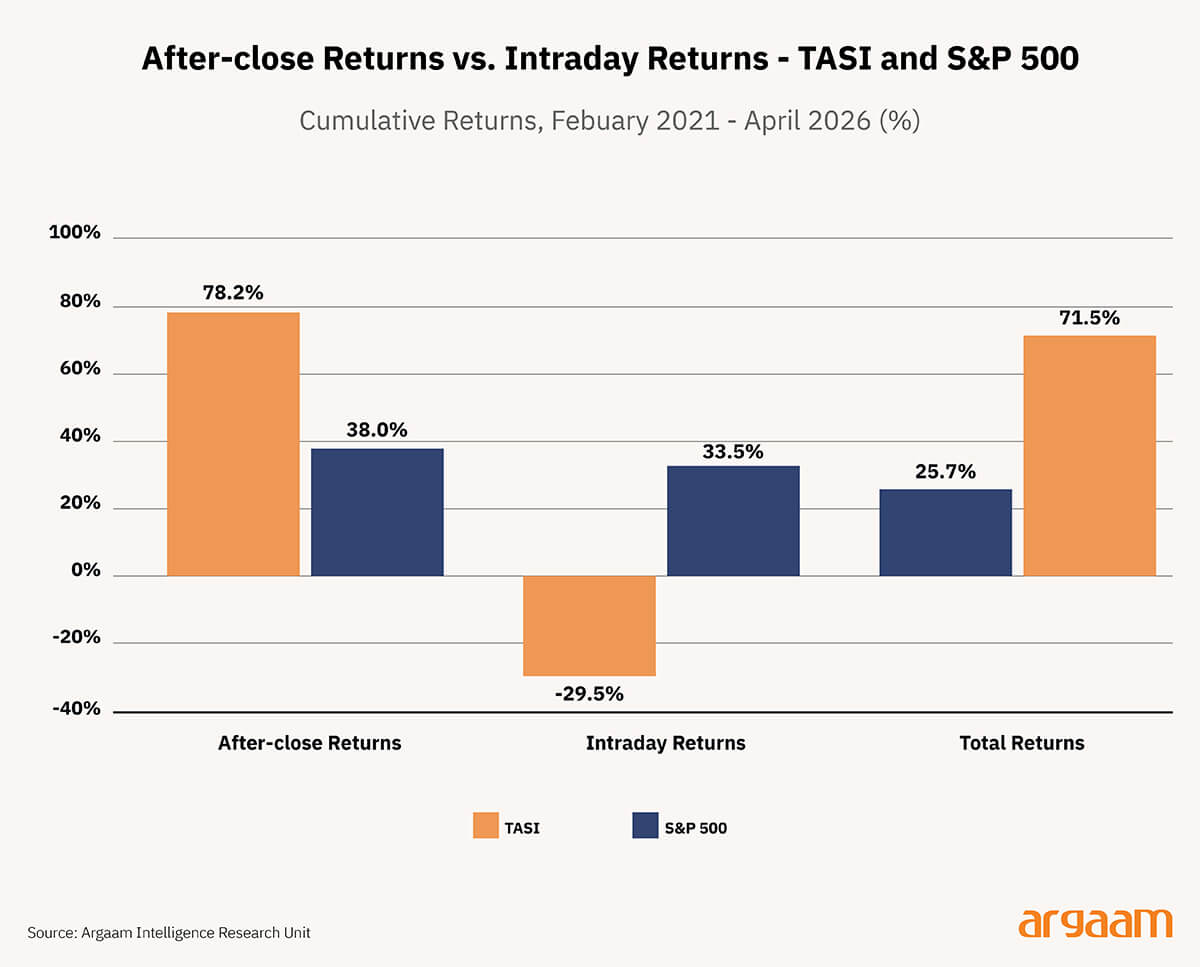

Drawing on daily open and close price data for the TASI index across 1,257 trading sessions meeting the analytical criteria — from 21 February 2021 to 9 April 2026 — the picture is unambiguous.

The cumulative after-close return over the period reached +78.2%, while the cumulative intraday return registered -29.46%. Total close-to-close returns over the same period were +25.7%.

In plain terms: after-close gains are more than three times the size of total returns, because intraday losses consume a substantial portion of those gains. This is not a marginal difference — it is a structural pattern.

Statistically, the mean daily after-close return is +0.047%, with a t-statistic of 3.65 and a p-value of 0.0003 — meaning the probability that this pattern is pure coincidence is less than one in ten thousand.

The mean daily intraday return of -0.025%, by contrast, is statistically insignificant — indistinguishable from zero.

◆ Note: the t-statistic measures how far a result sits from zero relative to normal data variation — the higher it is, the stronger the result.

The p-value measures the probability that the result is random: a value of 0.0003 means the odds of this pattern being coincidental are less than three in ten thousand.

Compared with the S&P 500 over a comparable period, after-close returns reached +38% and intraday returns +33.5% — with after-close accounting for 45.2% of total returns.

On TASI, the concentration in after-close sessions is roughly seven times greater than in the US benchmark.

◆Methodological note: Although TASI historical data on Yahoo Finance extends back to 1998, a systematic audit revealed that pre-2021 opening prices largely replicate prior closing values — rendering them unreliable for after-close return calculations.

The analysis is therefore confined to 1,257 verified sessions, a statistically robust sample by any conventional standard.

It is worth noting that academic research confirms a direct relationship between the length of a market's closure and the magnitude of the after-close effect — the longer the market remains shut, the more pronounced the phenomenon becomes.

This makes TASI an exceptional case: the three-day gap separating Thursday's close from Sunday's open provides a far wider window for this effect to build than any market operating on a standard single overnight closure between consecutive sessions.

This raises the central question this report sets out to answer: is the pattern of returns accruing after market close a universal feature of equity markets worldwide — or is it fundamentally a product of each market's own structure, shaped by its particular investor composition, price discovery mechanisms, and liquidity dynamics?

Answering that question in the context of TASI — with all its distinctive structural characteristics — is precisely what this report aims to do.

Gains take shape before everyone trades

The explanation becomes clearer when examining market structure. Institutional investors — led by large entities with significant market weight — combine long investment horizons with the operational capacity to build their positions at or before the market open.

By contrast, the more than seven million individual investors registered by end-2025 account for the bulk of daily trading activity.

The most plausible interpretation is that institutional investors, equipped with superior information access and execution capabilities, move first — establishing their positions at or just before the open, with gains crystallising in that initial moment.

Individual investors enter later, during ordinary trading hours, typically reacting to information that has already reached them with a delay, or responding to price movements that have already occurred.

This is not a reflection of inferior judgement on their part, but rather a structural reality: large entities possess the research infrastructure, analytical tools, and execution systems to act on information faster than is available to the ordinary investor.

As a result, their trades tend to arrive at a later stage of the price move, gradually eroding a portion of the gains that formed at the open.

ℹ︎

This implies no legal violation whatsoever — every transaction at the open is a fully lawful market operation. The pattern only becomes visible in aggregate, across thousands of sessions, when its consistency exceeds what can be explained by ordinary random variation

The Thursday-to-Sunday gap deepens this dynamic considerably. During Friday and Saturday — while TASI is completely closed — oil prices move, OPEC decisions are issued, geopolitical developments accelerate, and major economic announcements are made.

When the market opens on Sunday morning, not all investors arrive at the same starting point: the institutional investor will have absorbed these developments and reassessed positions over the weekend, while the ordinary investor finds himself facing a market that has already moved before he has had the chance to process what changed.

ℹ︎

Large institutions hold a structural advantage because they possess dedicated research teams, advanced technological infrastructure, longer investment horizons, and the capacity to process publicly available information at a speed that is simply not available to the individual investor. This advantage exists in every equity market in the world.

✧ Conclusion✧

These findings raise substantive questions across three dimensions.

◆ Investor protection: The Capital Market Authority's regulatory framework classifies individual investors among the highest-priority categories for protection, and the Investor Protection Guide explicitly acknowledges that this segment is more exposed to the consequences of information asymmetry.

The pattern this report documents is precisely the kind of structural disparity that does not manifest in any single transaction, and that individual investors cannot detect through their day-to-day trading experience — it only becomes visible when thousands of sessions are analysed together.

◆ Market efficiency: The theory of market efficiency rests on a fundamental premise: that prices reflect all available information simultaneously and equally for all participants, making sustained outperformance by any individual investor inherently difficult. The findings of this report invite a reconsideration of that premise as it applies to TASI, on three interconnected grounds.

Prior research has already established that the index's returns carry measurable historical patterns, and that the market's response to earnings announcements persists longer than the efficiency model would predict.

The central finding of this analysis adds a third dimension: the consistency with which gains concentrate at the open suggests that information does not reach all investors at the same speed — a finding that warrants serious regulatory attention, and one that implies information asymmetry between investor groups may be sufficiently wide to generate consistent patterns across multiple years.

◆Transparency and market development: Saudi Arabia aims to establish TASI as a globally competitive financial market with deep liquidity and broad foreign participation. The Capital Market Authority's decision to abolish the Qualified Foreign Investor regime effective February 2026 was a consequential step in that direction.

Yet attracting and sustaining foreign capital goes beyond access alone — it depends fundamentally on the confidence of international investors that prices in the market reflect available information fairly and equitably for all participants.

In this context, the patterns documented in this report — while carrying no suggestion of legal violation whatsoever — merit proactive regulatory attention, particularly given that major international institutions increasingly treat equality of access to information as a key criterion when assessing the readiness of emerging markets.

Accordingly, strengthening pre-open transparency, raising disclosure standards, and broadening individual investors' access to relevant market information are all measures that align directly with the Authority's stated strategic objective: building an efficient market that commands enduring confidence at home and abroad. |