Cerebras, a company looking to open itself up to public investment, reported a significant 220% growth in revenue from FY2022 to FY2023 (made public when the firm filed an S-1 in 2024).

Looking more closely into the S-1 reveals that 83% of total revenue in 2023 came from just one customer, G-42.

The overall growth this year is undeniable, but how sustainable is the revenue being created? The relationship between these two firms creates distortions in the numbers that are important for an investor to understand.

These distortions are caused by the revenue quality, the customer concentration, and a dual role problem (G42 playing the role of both customer and investor).

This article will look at how Cerebras’ accounting creates an illusion of growth, and how its relationship with G42 both creates the illusion of growth, and is likely causing higher overall risk than markets may initially acknowledge.

Revenue Quality: The Issues with Accruals Cerebras has a lot of prepayments from its services. Total deferred revenue grew from $3.99M at the end of 2022 to $48.965M in June 2024. Rollforward in H1 2024 shows this deferred revenue is actively turning over, but with more additions than revenue recognised, so this prepayment balance is growing.

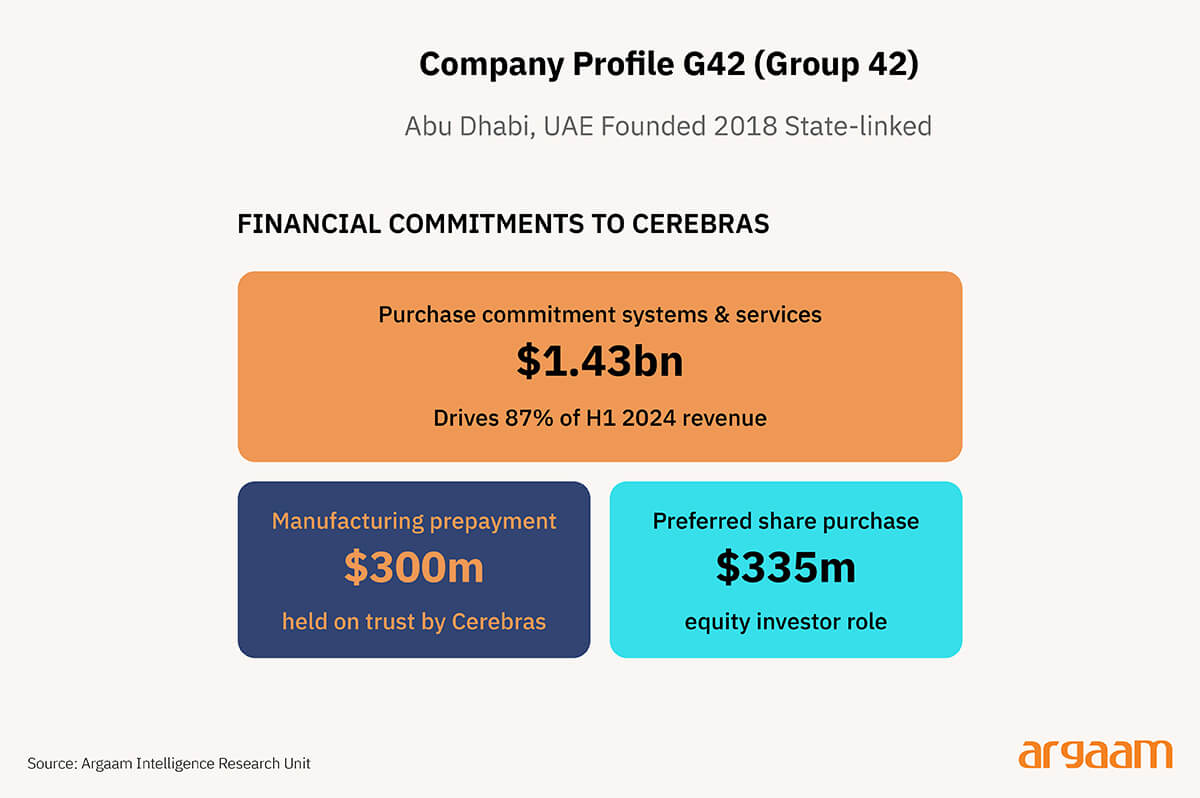

However, more importantly, is the $300.049M classed as customer deposits. This is essentially a prepayment from G42, Cerebras must use this $300M to fulfil any purchase orders that G42 places - but if no purchase orders are placed then Cerebras must return the money.

This $300M sits on the balance sheet as a liability, and when it arrives creates a large cash inflow, but there is no immediate impact on the income statement.

The cash is converted into revenue, in chunks, whenever Cerebras must manufacture and deliver hardware for a G42 purchase order. Operating cash flow in H1 2023 was a negative $70.185M, and in H1 2024 leapt to a positive $311.813M.

This makes it seem like business has become more effective at generating cash, but this swing is significantly attributable to simply a liability being added on the balance sheet and not actual revenue being earnt.This is reflected by the income statements.

In H1 2024, Cerebras had a net loss of $66.6M, despite the cash gain in the same period. An issue with this contractual revenue recognition is that the accounting cycle being front loaded can make future performance look worse.

Once this prepaid $300M pool is drawn down, the revenue being recognised from this contract will start declining - simply as there is less money in the pool.

This can make subsequent quarters look less profitable - which isn’t because demand has fallen but because purchase orders run out unless new contracts can get signed.

The balance sheet also hides a risk. This $300M is restricted cash, if G42 does not issue the purchase orders then Cerebras must return the money, which would be a very significant cash outflow.

We believe that accrual based earnings (the way in which Cerebras defers revenue) have significantly lower persistence than cash based earnings.

More simply, accrual based earnings results in less earnings predicted in the future. Sloan also finds that markets do not correctly acknowledge this information - future earnings are valued the same regardless of if they are accrued or cash based.

In this case, investors might then see Cerebras’ 220% growth, but fail to price the components of Cerebras’ earnings correctly. Markets essentially treat Cerebras’ earnings the same as if they were generating equivalent revenues with numerous customers in a more ‘sustainable’ way.

Mispricing Risk: The Relevance of Customer Concentration

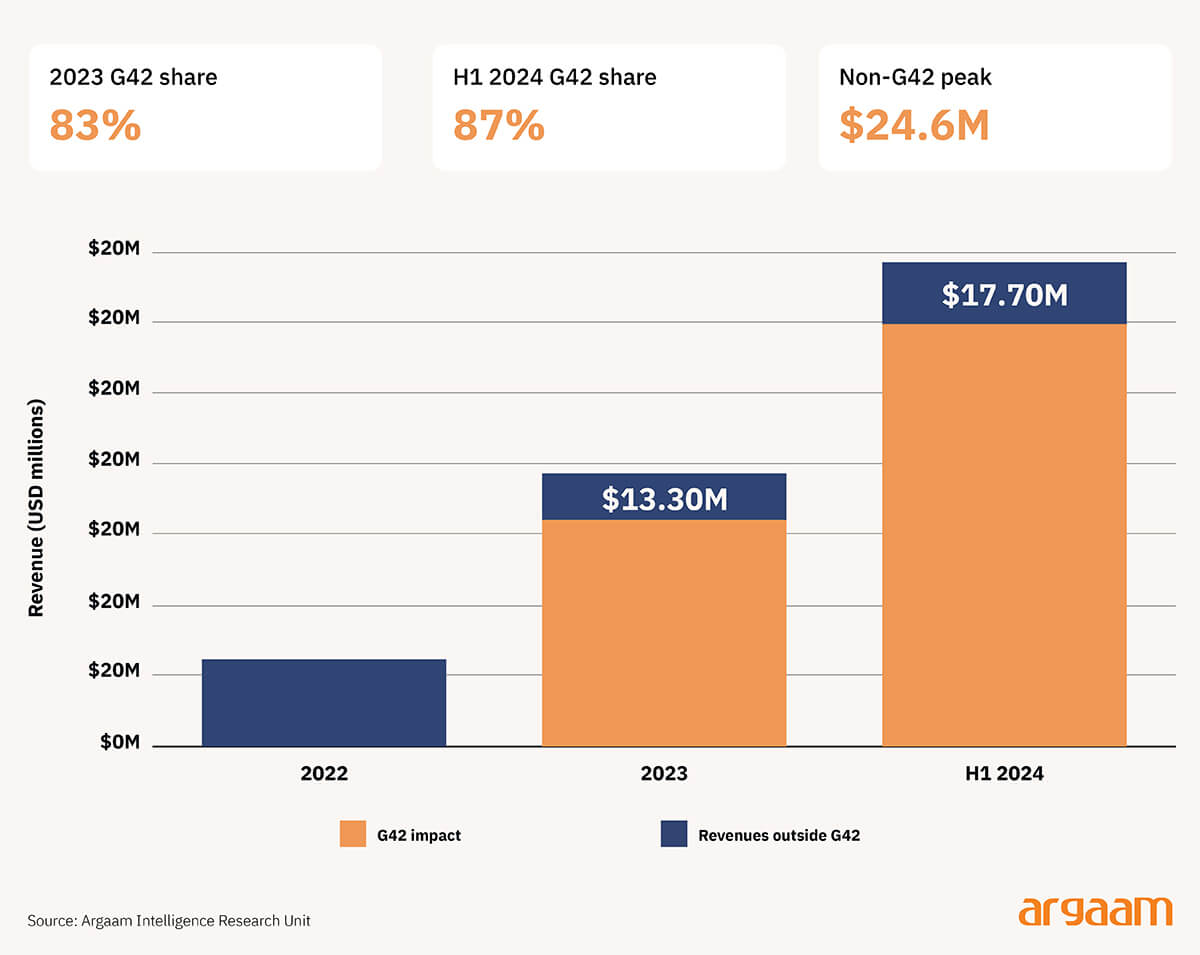

Cerebras’ customer concentration was clearly high in 2023 and 2024, 83% of their revenue being generated by G42 throughout 2023 and 87% in H1 2024, as stated by Cerebras themselves in the S-1.

Cerebras claims to be a growth company, but what happens when you remove this single relationship? By stripping away estimated G42 revenue from total revenue in 2022, 2023, and H1 2024, the respective non-G42 revenue becomes $24.6M (before G42) → $13.3M → $17.7M.

This is a very different story than implied by the headline 220% growth. Is Cerebras really a growth company in the market, or a company with a profitable single contract? Having a large portion of business with one customer should raise concern from investors.

But higher customer concentration is positively associated with cost of equity capital - the more a company relies on a smaller number of customers the higher the risk, and the more return investors should be expecting.

Also, risk is amplified when suppliers would suffer larger losses in the case of losing customers or if they are more likely to lose their customer. However, it is important to note that markets underprice these risks during growth phases, and only corrects once this risk becomes too pronounced to ignore.

Cerebras would effectively be priced as a sustainable growth company regardless of this heavy dependency on G42, but if this risk became too obtrusive, then markets would abruptly correct. Without this relationship, Cerebras become only a fraction of their current worth.

Other factors in this specific relationship further amplify Cerebras’ risk. G42 has cut ties with foreign firms in the past due to geopolitical reasons, so changing political dynamics is another source of possible volatility in this relationship.

G42 itself also does not publish any financials, so there is no way for investors to independently verify G42’s health, and how reliable it is that this $1B+ commitment will be fulfilled.

If G42 reduces or cancels its purchase commitment, whether that be for business or political reasons, Cerebras’ revenue base collapses. Although Cerebras’ S-1 claims to “expect customer concentration to decrease over time” the S-1 does not provide any hard plan or evidence of this.

It is also important to note the conflict of interest in equity pricing. G42 as a shareholder with financial interests wants to maximise Cerebras’ value. But G42 as a customer has a commercial interest to pay as little as possible. These two conflicting interests means that behaviour in any given transaction is difficult to decipher.

Related party transactions such as this are associated with lower earnings quality - because investors cannot determine which interest is the main driver.

All transactions made with G42 carry lower earnings qualities according to the findings. Although the S-1 claims that its relationship with G42 reflects arms length terms, there is no way of independently verifying this.

✧ Conclusion✧

Cerebras's 220% revenue growth is real — but it is the materialisation of a single relationship, not a market. Strip out G42 and what remains is a business generating $13–18M from all other customers combined.

The headline figure obscures a more uncomfortable truth: these are not financial statements shaped by arm's length market dynamics, but by one counterparty whose true interests cannot be determined and whose ability to fulfil purchase commitments cannot be independently verified.

It is possible that Cerebras diversifies, that non-G42 revenue accelerates, or that the G42 relationship simply proves durable. But the more recent pivot — away from G42 and toward a reported $10B contract with OpenAI — raises a harder question: is Cerebras building a business, or serially building dependencies? A new anchor customer resolves the concentration risk only if it is the last one.