● The Cumulative Effect of an External Shock Coinciding with Domestic Structural Transformation

Saudi Arabia's industrial sector is navigating an exceptional convergence of simultaneous pressures: the supply chain repercussions of the US-Israeli conflict with Iran, domestic energy price reforms, escalating construction costs, and tightening credit conditions — all within a single financial cycle. When an external disruption coincides with internal structural reform, the impact does not appear in this year's data. It surfaces in the productive capacity gap five years from now.

❄️

The Damage Mechanism: Freeze Precedes Cost

The prevailing assumption is that companies stop investing when costs rise. But what crisis-cycle data consistently reveals is the opposite sequence: companies first stop investing because they cannot forecast; second, because liquidity has been redirected to cover operating costs; and only third does elevated cost emerge as a constraining factor.

◆ Uncertainty alone is sufficient to defer a capacity expansion decision

We do not invest when we cannot price the project: what energy will cost next month, when the shipment will arrive, what rate the expansion loan will carry.

◆ Capital earmarked for a new production line is absorbed by the logistics bill

When a shipping shock coincides with rising energy cost pressure, reserve liquidity is channelled into covering operations — not into investment.

◆ Structural damage materialises after the disruption ends

A company may survive the crisis without going under, yet emerge with ageing equipment and a widening technology gap. When demand returns, it cannot respond quickly enough — and a foreign competitor fills the void.

The Simultaneity That Converts Challenge Into Compound Burden

When these pressures arrive in isolation, companies typically have sufficient time and resources to adapt. It is their convergence at the same moment that transforms pressure into crisis.

A. Supply Chain Disruptions: A Structural Cost Shock

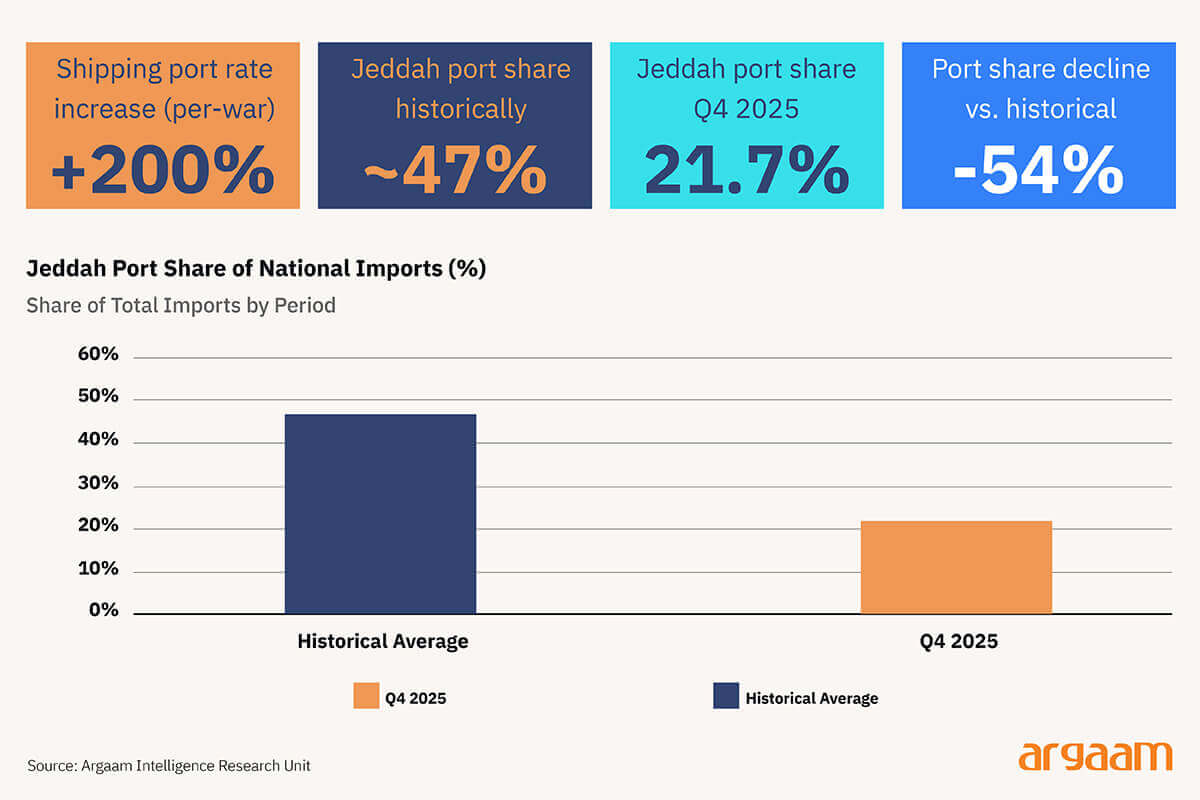

Shipping rates had already risen more than 200% before the latest conflict. Jeddah port's share of national imports fell from a historical average of approximately 47% to 21.7% in Q4 2025 — meaning the bulk of what once arrived directly to western Saudi Arabia now travels longer routes via Dammam or alternative Gulf ports. A factory operating on a Just-in-Time model has no buffer to absorb this delay: its production line stops before the shipment arrives.

B. Energy Pricing Reforms: An Internally Programmed Pressure at an Inopportune Moment

The reforms were designed to phase in gradually over years — not to coincide with an external shock. The conflict has not introduced new energy costs; it has compressed the timeline. Companies are absorbing the final phase of the reform cycle before they have built the reserves needed to adapt.

The difference is not in the magnitude of the cost, but in its timing: what could have been absorbed over five years may constitute a genuine risk when concentrated into a single year.

C. Credit Pressure: Competition for Liquidity Between Private Lending and Government Financing Pull

The loan-to-deposit ratio has reached approximately 106% — a level that puts banks in credit rationing mode. A compressed net interest margin of 2.73% means banks select the safe borrower; government-backed projects move to the front of the lending queue.

The private manufacturer does not find the door permanently closed, but finds it narrower and more expensive. That alone is sufficient to defer an upgrade or equipment purchase to "a quieter quarter ahead."

A Counter-Reading of the Machinery Figures

The headline numbers say one thing. A careful reading says the opposite.

|

Surface Reading |

Counter-Reading |

|

Machinery imports rose 23% — the sector is expanding and investing in new equipment. |

◇ Aggregate imports do not distinguish between domestic consumption and re-exports |

|

◇ A 79.2% re-export ratio means the Kingdom is acting as a logistics corridor, not an industrial investor |

|

◇ Rising trade flows ≠ new industrial capital formation |

|

◇ The hasty reader commits the classic analytical error |

The parallel rise in machinery re-exports — 79.2% over the same period — reveals that a meaningful portion of these imports is not converting into domestic productive capacity.

The Kingdom is fulfilling a logistics corridor role (which carries genuine economic value), but this is structurally distinct from domestic capital investment.

What gives this analytical reading its significance is precisely its capacity to move beyond the surface indicator and render a fuller, more nuanced picture.

Historical Precedent: Deferred Damage Is a Documented Pattern

What this analysis describes is not a theoretical hypothesis. It is a pattern documented in two comparable crises.

1973 Crisis: United States — Deferred Capital Contraction

➨ The oil crisis caused an abrupt surge in energy costs. Factory utilisation rates fell from 89% to 71% in under two years — meaning a third of US productive capacity went idle.

➨ Capital expenditure fell from 4.1% to 2.2% of GDP and did not recover to its pre-crisis level until 2004.

➨ A decision to pause investment — which appeared temporary — became structural weakness that persisted for three decades.

2022 Crisis: Europe — The Competitive Gap with the Cheaper Rival

➨ Russia's invasion of Ukraine caused an abrupt spike in energy prices. Factories could no longer sustain production costs and either closed or reduced capacity.

➨ Cheaper Chinese imports began filling the void left by idled European plants. The import-to-domestic-production ratio rose 11% in energy-intensive sectors.

➨ The competitive gap does not reveal itself at the height of the crisis — it surfaces at the moment of recovery, when demand returns to find the domestic producer not yet ready.

SABIC: Live Evidence from the Saudi Context Itself

SABIC's experience in the European market matters not as an isolated example, but as proof that the logic described here has already translated into a decision inside a major Saudi corporation.

When the elevated cost environment outweighed expected returns, SABIC closed its UK facility and exited the European market entirely.

The analytical projection: if SABIC — with its financial scale and state backing — took this decision in a foreign market, the legitimate question is: what protects the smaller, less capitalised domestic manufacturer from making a comparable decision within Saudi borders?

The difference is that this decision will not be recorded as an accounting write-off in an annual report. It will appear years later in operating and employment data.

✧ Conclusion ✧

This analysis does not approach the conflict as a direct threat to Saudi industry. It examines a subtler phenomenon: how the convergence of external disruption and domestic structural reform — should geopolitical instability persist — can quietly erode industrial investment decisions, even as the headline indicators of output and employment remain within acceptable bounds.

ℹ︎

INDICATOR UNDER THE LENS

The metric to watch is not the current capacity utilisation rate, but the industrial capital renewal rate — in other words: is the private sector purchasing new equipment, or running existing assets until exhaustion?

The difference between these two answers is the difference between a sector that exits this phase more competitive and one that exits it carrying a capital gap that will take a decade to close.

The solution is not to freeze the reform agenda, but to anchor it to transitional financing mechanisms that give manufacturers the time window to adapt — rather than forcing a defensive contraction.