ℹ︎

This analysis by Argaam Intelligence integrates visible economic indicators with the broader supply chain context, with the aim of moving beyond a literal reading of standalone figures. The detailed research methodology and in-depth analytical framework remain the intellectual property of Argaam.

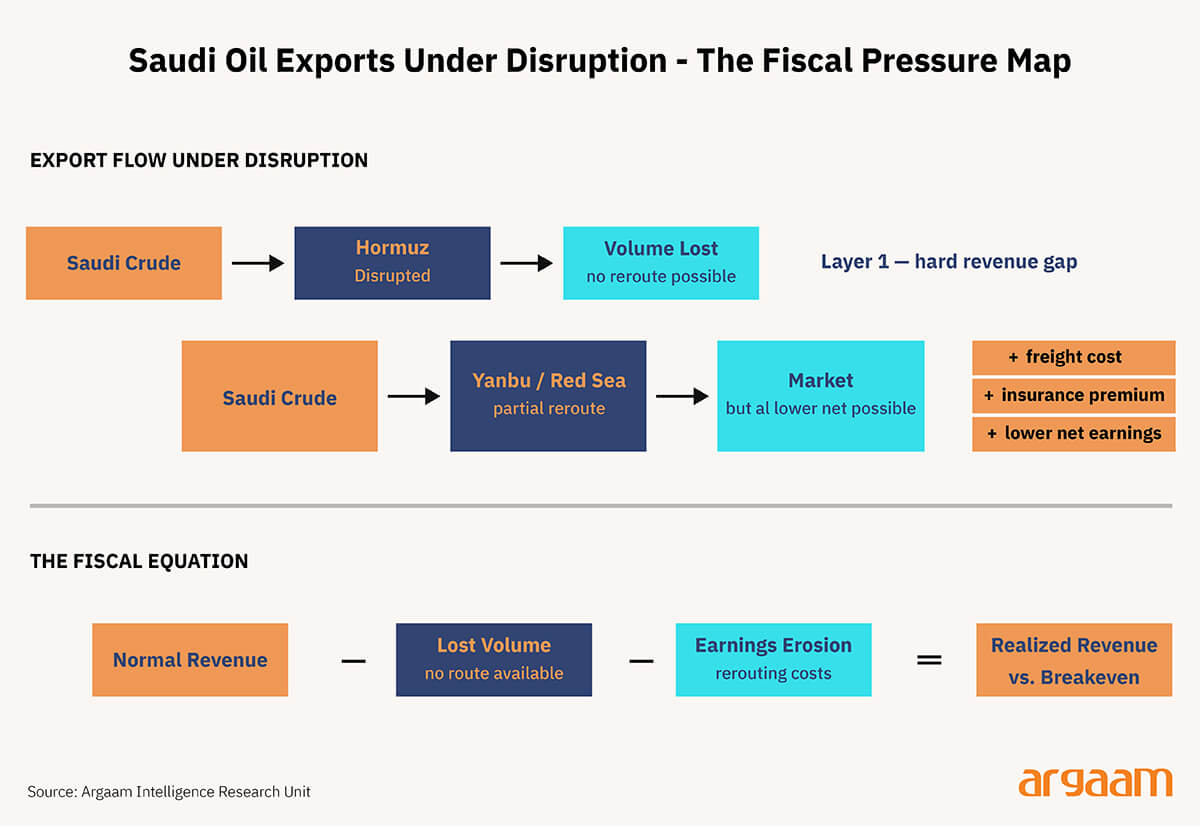

The East-West Pipeline and Yanbu terminal resolve the logistics question. What they do not resolve is the fiscal one. Even with full rerouting capacity operational, Saudi Arabia faces a gap between the price its crude commands under normal conditions and the price a disrupted, rerouted, risk-premium-laden market will actually pay.

The analytical question worth holding is not whether the oil moves — it can — but what it earns when it does, and whether that is enough to sustain some budget commitments, especially those related to development projects.

Yanbu absorbs some of what Hormuz cannot move, but the recovery is partial and comes at a cost — higher freight, steeper insurance premiums, thinner margins on every barrel rerouted.

The disruption does not stop the oil from moving; it erodes what the oil earns. That distinction matters, because it reframes the problem from one of supply continuity to one of fiscal endurance.

The right analytical lens, therefore, is not a single forecast but a scenario matrix built around two variables that will determine the outcome: how long the disruption lasts, and where oil prices settle relative to Saudi Arabia's fiscal breakeven — the price per barrel the kingdom needs to balance its budget.

The fiscal impact, therefore, has two distinct layers. The first is volumetric: the barrels that cannot move through either route represent a hard revenue gap with no offsetting mechanism.

The second is marginal: the barrels that do move through Yanbu arrive at a discount to their normal value once rerouting costs are stripped out. These two layers do not behave the same way under different scenarios.

Volume loss is binary — it either exists or it does not. Margin erosion is continuous, worsening as disruption extends and insurance markets reprice risk upward. A complete fiscal assessment requires treating them separately.

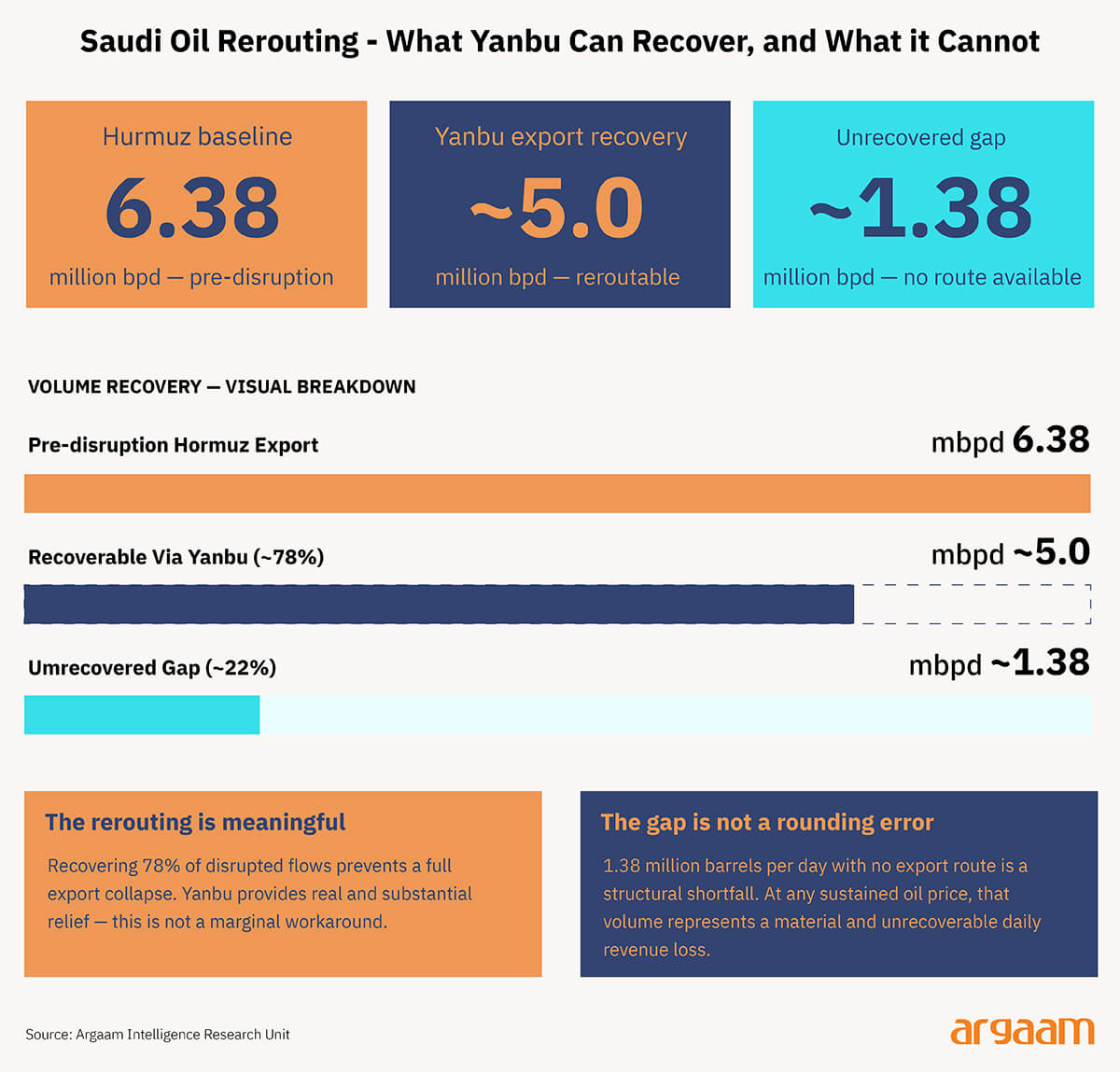

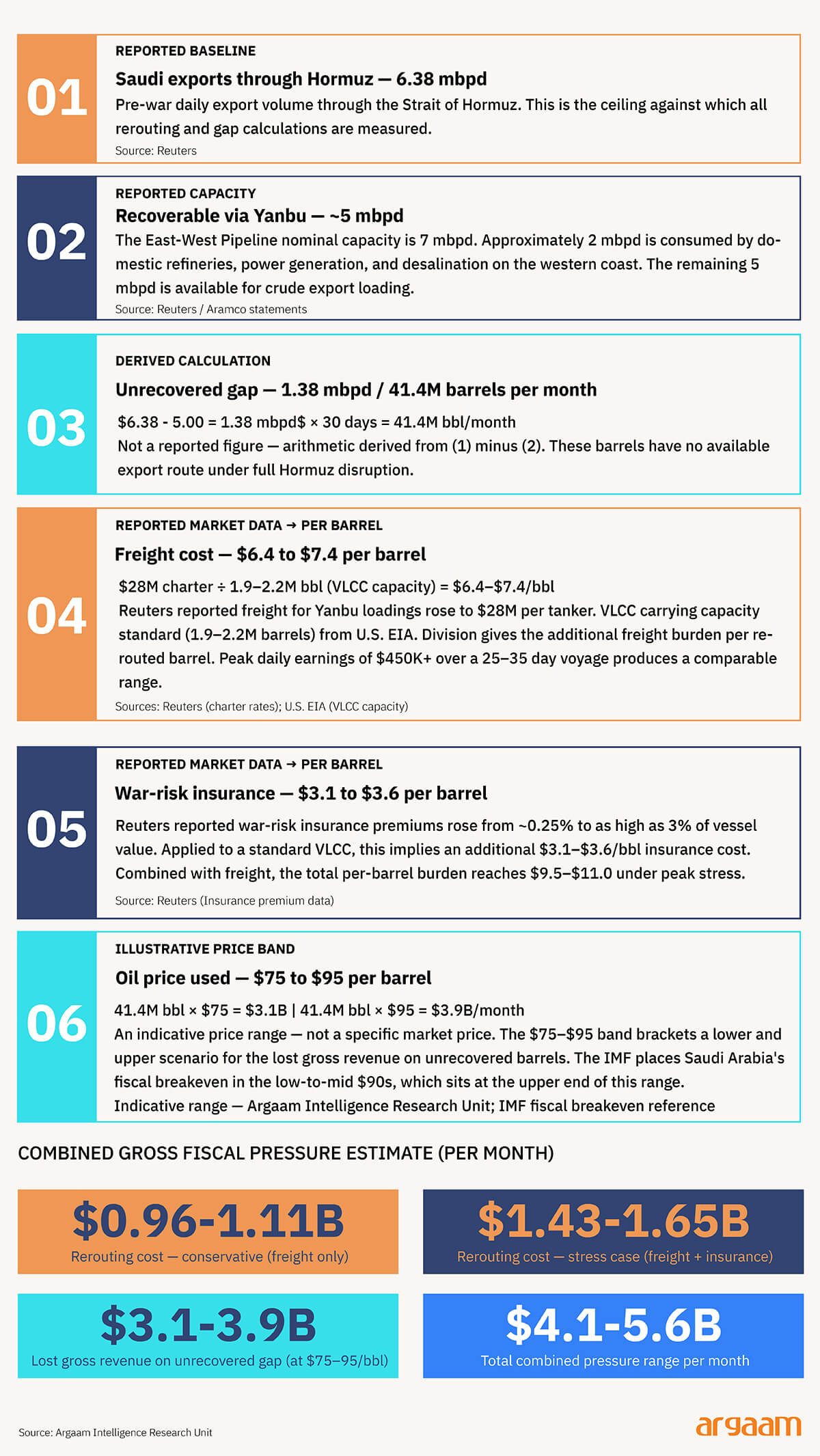

Before the disruption, Saudi Arabia was moving approximately 6.38 million barrels per day through the Strait of Hormuz. If that route were to close entirely, the East-West Pipeline and Yanbu terminal could redirect around 5 million barrels per day westward for export — recovering roughly 78% of the disrupted volume.

That leaves approximately 1.38 million barrels per day with no available export route. The numbers tell a story that cuts both ways.

The rerouting capacity is substantial enough to prevent a complete export collapse, but the unrecovered gap — nearly a quarter of normal eastern flows — is large enough to register as a meaningful fiscal shortfall, not a rounding error.

There is a second layer to the Yanbu picture that is worth understanding. Looking at Aramco's own port data, the physical loading infrastructure at Yanbu is not actually the main bottleneck.

The north terminal has four crude berths, each capable of loading at 130,000 barrels per hour, and the south terminal has three berths capable of 132,000 barrels per hour. That is a substantial loading capacity on paper.

The real constraints sit further back in the chain. Sustaining high export volumes through Yanbu over a prolonged period depends on how much crude the East-West Pipeline can continuously push through, how storage and scheduling at the terminal holds up under pressure, and how crude is allocated between export and domestic refining needs.

Those are the variables that would determine the ceiling in practice, not the number of berths. The practical conclusion is straightforward. Yanbu is a meaningful buffer — large enough to matter significantly in any disruption scenario — but it is still a capped system with operational limits that prevent it from fully replacing Saudi Arabia's eastern export infrastructure on a sustained basis.

The Oil Still Moves — But It Earns Less

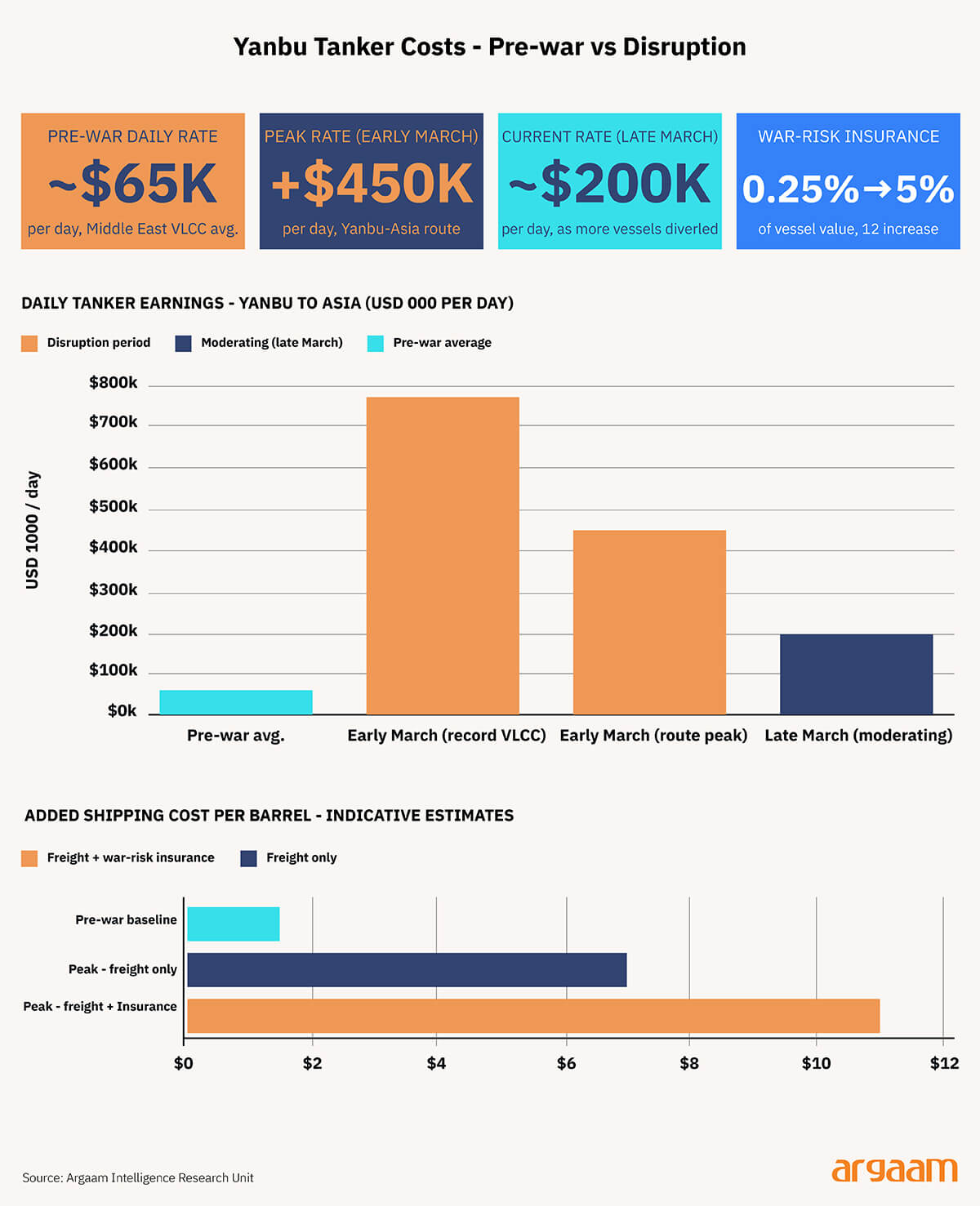

When Saudi Arabia reroutes oil through Yanbu instead of Hormuz, the oil still moves — but it costs significantly more to ship. Tanker earnings on the Yanbu-to-Asia route surged to over 450,000 dollars per day at their early-March peak — more than three times the pre-war average for equivalent Middle East voyages.

As more vessels repositioned to the Red Sea, rates moderated to around 200,000 dollars per day in the weeks that followed, but even that reduced level remains well above normal conditions.

To translate daily earnings into per-barrel cost, a standard large crude tanker carries between 1.9 and 2.2 million barrels, and a Yanbu-to-Asia voyage runs roughly 25 to 35 days.

At peak rates, the total voyage cost approaches 11 to 16 million dollars per tanker, implying a shipping-cost increase of roughly 5 to 8 dollars per barrel compared to pre-disruption norms — simply to move the same oil through an alternative route.

War-risk insurance adds a further layer. Premiums had risen from around 0.25% of vessel value to as high as 3% — a twelvefold increase.

When that insurance cost is factored in alongside the freight increase, the total additional burden on each rerouted barrel could exceed 9 to 11 dollars in a peak stress scenario.

These are indicative estimates built from reported market data, not official Saudi government figures. But the direction they point in is unambiguous. Every barrel that takes the Yanbu route instead of Hormuz earns less — sometimes significantly less — than it would under normal conditions.

The Saudi fiscal challenge under disruption is therefore not only about how many barrels can be exported. It is equally about how much each exported barrel actually earns after the full cost of getting it to market is accounted for.

The scenario matrix is not a forecast. It is a structured way of showing how fiscal pressure shifts when two variables move together: how long the disruption lasts, and where oil prices sit relative to Saudi Arabia's fiscal breakeven — the price per barrel the government needs to balance its budget. The IMF has placed that breakeven in the low-to-mid nineties per barrel.

The cost estimate has two components. First, the rerouting burden — the extra freight and war-risk insurance cost on every barrel that moves through Yanbu.

Based on reported market data, that adds roughly 0.96 to 1.11 billion dollars per month in a conservative case, rising to around 1.43 to 1.65 billion dollars per month under peak stress conditions.

Second, the unrecovered volume — the barrels that cannot move through either route. Valued at prevailing prices in the 75 to 95 dollar range, the lost gross revenue from that gap alone runs to approximately 3.1 to 3.9 billion dollars per month.

Combined, the indicative gross fiscal pressure sits in the range of 4.1 to 4.8 billion dollars per month under a lower-price scenario, and 4.9 to 5.6 billion dollars per month under a higher-price scenario. These are not official government figures.

They are order-of-magnitude estimates that illustrate the scale of pressure building across different combinations of duration and price — and how quickly that pressure compounds the longer the disruption extends beyond the IMF breakeven threshold.

✧ Concluding remarks ✧

✧ If oil prices stay above the fiscal breakeven, a short disruption — under three months — looks manageable. Strong prices cushion the revenue loss from unrecovered export volumes, and Saudi Arabia has enough room to absorb the extra rerouting costs through higher oil receipts, reserve drawdowns, and access to debt markets if needed.

✧ A medium disruption of three to nine months would still be financeable, but pressure would start to build. The unrecovered export gap does not reset — it accumulates month after month. Rerouting costs compound over time. Even if the budget remains fundable on paper, the margin for manoeuvre narrows steadily.

✧ Beyond nine months, high oil prices would still help, but they would no longer be enough to fully offset the combined weight of the export gap and the persistently higher cost of shipping through Yanbu. At that point, the conversation shifts from managing a disruption to making choices about which spending commitments to prioritise and which to defer.