Licensed taxi operators in Saudi Arabia have not lost ground simply on price — the deeper disruption is structural. Ride-hailing platforms dissolved the economic logic that sustained traditional taxi operations: fixed fares, territorial exclusivity, and predictable daily yields.

In their place came algorithmic pricing, demand aggregation, and real-time driver deployment — mechanisms that traditional operators lack both the capital and regulatory permission to replicate.

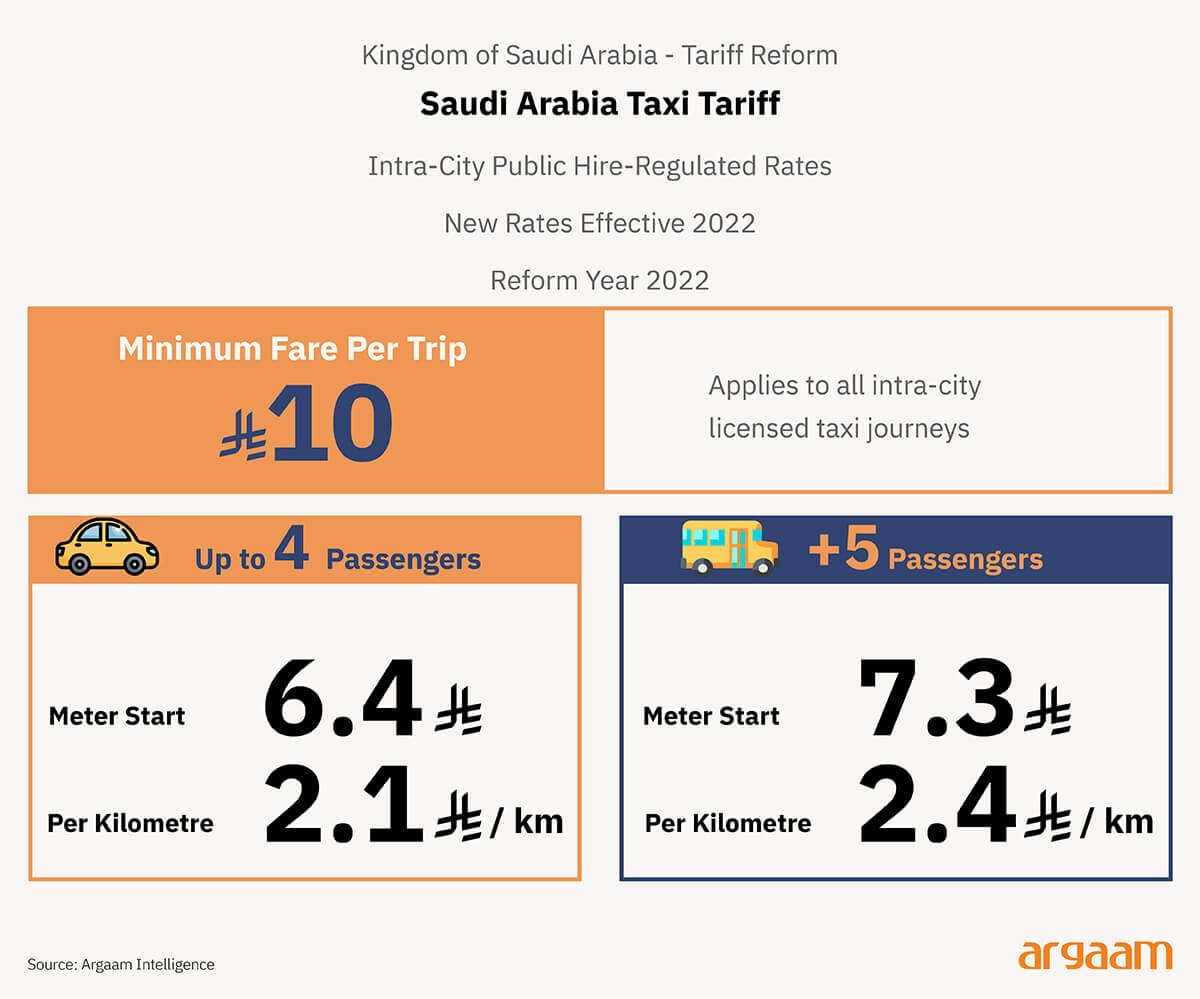

The 2022 tariff revision is analytically significant — it confirms that regulators recognised the pricing gap and attempted to close it.

But the reform's limitations reveal precisely why our economic structural argument holds. Raising the meter flag and per-kilometre rate addresses one variable in an equation that platform operators have already rewritten entirely.

Consider what the new tariff does not touch. It does not grant licensed operators dynamic pricing authority — they remain bound to fixed rates regardless of demand conditions, while platforms adjust fares in real time, capturing peak-hour revenue that taxi drivers cannot access. It does not resolve territorial allocation rigidities or reduce vehicle-licensing costs.

And critically, it does not address the demand-side shift: passengers who migrated to app-based services between 2014 and 2022 did not leave primarily because taxis were expensive — they left because platforms offered cashless payment, GPS tracking, driver ratings, and guaranteed availability, none of which a tariff revision restores.

Against this backdrop, a passenger surcharge on ride-hailing trips, channelled into a dedicated compensation fund for licensed taxi drivers, deserves serious consideration from policy makers and it’ the main angle of this analysis from Argaam Intelligence.

The logic is straightforward: those who benefit most directly from technological disruption contribute to transitional support for those who bear its costs. The policy question is not whether ride-hailing should exist, but how its distributional effects should be managed.

But the response does not have to be a compensation cheque and a quiet exit. Dubai showed that there is another way — one where licensed taxis are not pushed aside by the platform economy but pulled into it as we explain in the last part of this analysis.

There is also a timing problem that no tariff revision could solve. By 2022, app-based platforms had already spent nearly a decade building passenger habits, driver networks, and routing infrastructure across Saudi Arabia's major cities.

That accumulated presence does not unwind because a competitor adjusts its prices — passengers who have grown accustomed to booking a ride from their phone, tracking its arrival, and paying cashlessly are not drawn back by a revised meter rate.

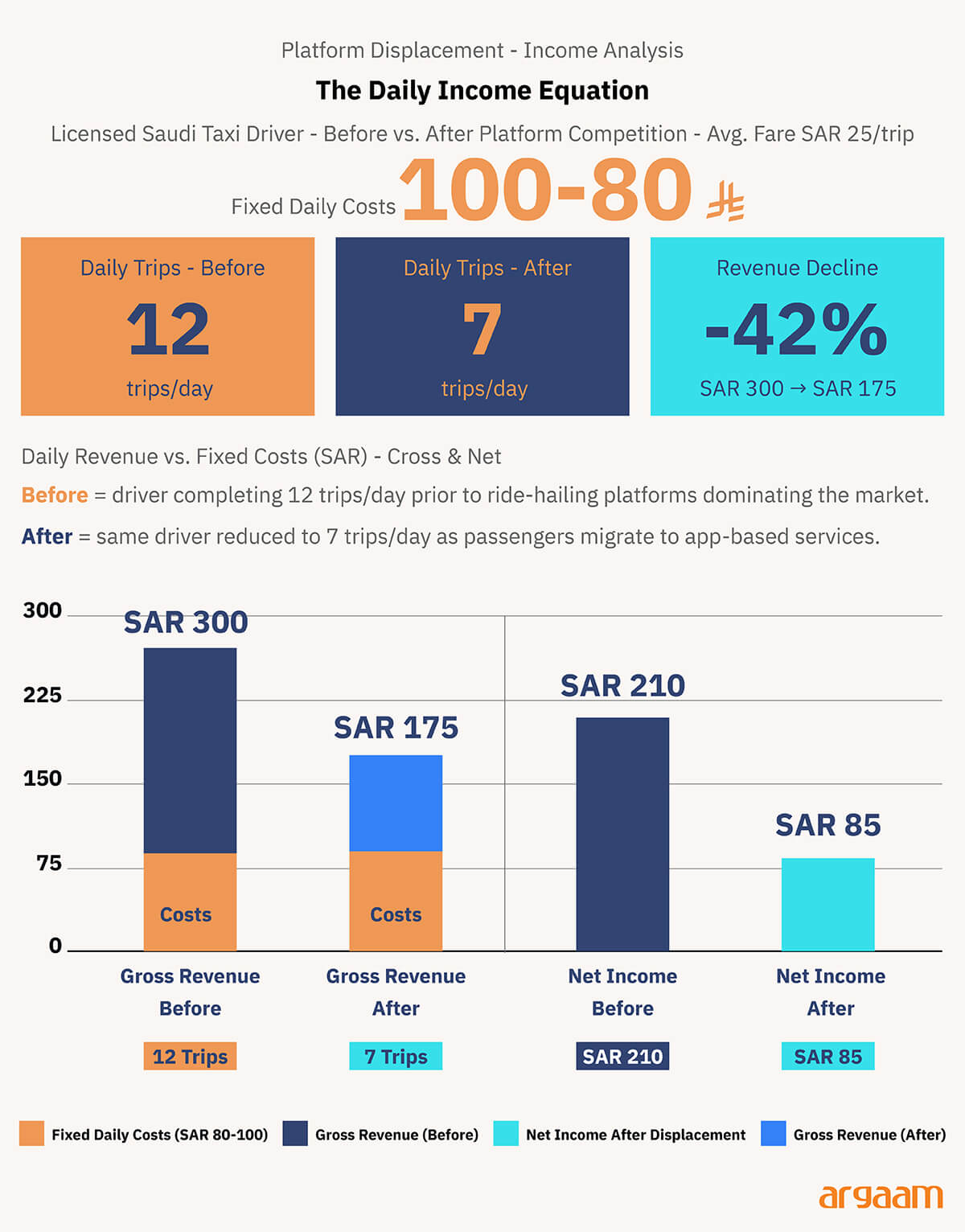

SAR 175 In, SAR 100 Out

The economic loss to traditional taxi drivers is not only about losing passengers to platforms — it is about what happens to the time in between. A licensed taxi driver who completes fewer trips does not simply earn less; his fixed costs — fuel, vehicle depreciation, licensing fees — continue accumulating whether the car is moving or stationary.

As platform services absorb a greater share of urban trips, traditional drivers spend more time cruising or waiting for a fare that may not come, effectively paying to work without earning.

A driver who previously completed 12 trips daily at an average fare of SAR 25 generated SAR 300 in gross revenue. If platform competition reduces that to 7 trips, revenue falls to SAR 175 — a 42% decline — while his daily fixed costs of roughly SAR 80 to SAR 100 remain unchanged.

The idle hours are not neutral; they are expensive. Every kilometre driven without a passenger is a cost without a return.

When trip earnings fall, drivers do not reduce their hours — they extend them. The instinct is rational: if each trip pays less, more trips are needed to reach the same daily income. But the response contains its own trap.

Longer hours on the road do not proportionally restore earnings; they dilute them. A driver working fourteen hours instead of ten to recover lost income is not earning more per hour — he is earning less, while absorbing greater fuel costs, accelerated vehicle wear, and physical fatigue that compounds over time.

The practical example sharpens the point. A driver who previously earned SAR 300 across ten hours — SAR 30 per hour — and now earns SAR 175 across the same period faces a stark choice: accept the income loss or extend his shift.

If he works fourteen hours to recover closer to SAR 280, his hourly return has fallen from SAR 30 to SAR 20, and his operating costs have risen with every additional hour driven. He has worked harder, worn his vehicle faster, and still not recovered his former income.

Taxing the Algorithm

A small surcharge on every ride-hailing trip — invisible to most passengers but significant in aggregate — could fund direct compensation for taxi drivers displaced by platform competition.

The logic is clean: the transaction that causes the harm finances the remedy. Saudi Arabia already has the regulatory infrastructure to collect and distribute such a fund through the General Authority for Transport.

The real work is in the design: how much to charge, who qualifies, and how payments are structured. Those are solvable problems. The more important point is that the mechanism exists, the justification is clear, and the cost to passengers would be negligible.

Saudi ride-hailing platforms completed 80.5 million trips in 2024, generating SAR 2.3 billion in revenue — figures published by the General Authority for Transport that now serve as the baseline for any serious policy calculation.

The numbers matter here because they transform the surcharge argument from abstract principle into testable arithmetic: a one riyal levy on every trip would have generated SAR 80.5 million in 2024 alone, without touching platform economics or meaningfully affecting passenger behaviour.

A one riyal surcharge would not alter how Uber or Careem price their services, manage their drivers, or compete with each other. Their business model remains intact.

For passengers, Someone paying SAR 25 for a ride would now pay SAR 26. That difference is too small to change whether they book the app or look for an alternative. Demand holds.

A SAR 1 surcharge per trip would generate roughly SAR 80 million annually

SAR 2 per trip: ~SAR 160 million

SAR 3 per trip: ~SAR 240 million

Spread across the licensed taxi driver population, that SAR 80.5 million would not replace a driver's lost income — but it was never designed to.

Divided among, say, 50,000 drivers, it amounts to roughly SAR 1,600 per driver annually. Among 20,000, it rises to SAR 4,000. The exact figure depends on how many drivers qualify, but the point holds across all assumptions: this is a cushion, not a salary.

Precise figures are not a prerequisite for policy action, since data is hard to get. But our calculations represent reasonable estimates, and it’s better rather than waiting for data that may never arrive.

Who Really Pays?

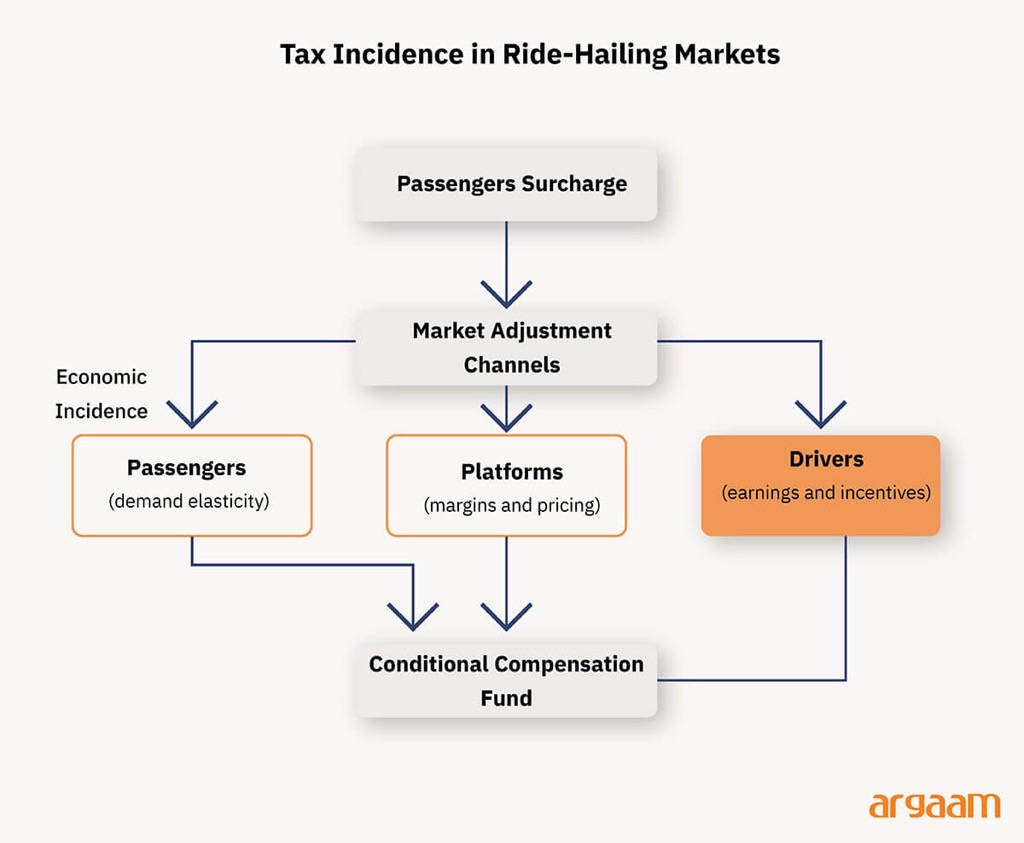

Calculating how much a compensation fund could raise is the easier part of this policy challenge. The harder question is what happens next: once a surcharge enters the ride-hailing ecosystem, market forces — not regulatory intent — determine who ultimately absorbs it.

When a government adds a charge to a transaction, it decides who pays it on paper — but markets do not always follow that instruction. A surcharge formally charged to passengers may end up being absorbed by platforms, who quietly reduce driver commissions to protect their margins.

Or drivers may bear it indirectly through reduced incentive payments. The label on the charge and the reality of who pays it can be two very different things.

Tax incidence analysis is simply the discipline of tracking where the burden actually lands after everyone in the market has adjusted their behaviour.

It asks: once platforms, drivers, and passengers have all responded, who is genuinely worse off? That answer determines whether the surcharge does what it promises — or quietly fails while appearing to function.

Who ends up bearing the cost of a surcharge depends on where the power sits in the market. In ride-hailing, passengers have options and platforms compete aggressively for their business — which means neither side can easily absorb a price increase without losing ground.

That pressure has to go somewhere, and economic evidence consistently shows it travels toward whoever has the least leverage to resist it.

That is almost certainly the driver. Platforms protect their margins, passengers remain price-sensitive, and drivers — operating without collective bargaining or formal employment protections — are left holding a cost they had no part in setting.

Saudi Arabia had more than 332,000 active ride-hailing drivers in 2024, up 27% year-on-year, according to the TGA, indicating a growing but increasingly competitive driver pool.

This diagram tracks what happens to a passenger surcharge once it enters the market — and the answer is that it does not stay where it was placed.

The surcharge is formally charged to passengers at the top. But before it reaches any compensation fund, it passes through what the diagram calls market adjustment channels — meaning the market reshapes who actually bears the cost.

Three parties can absorb it. Passengers may pay more if demand holds — but ride-hailing demand is sensitive to price, so platforms risk losing bookings if fares rise visibly.

Platforms can protect passenger-facing prices by quietly compressing their own margins or, more likely, reducing driver incentives and commissions. Drivers absorb it through their earnings without any visible fare change to the passenger.

The Dubai Taxi Model

Dubai took a different route of how taxi-sector disruption can be managed. Rather than treating app-based mobility as an external threat to traditional taxis, Dubai folded licensed taxis into the platform economy itself.

In 2019, the Roads and Transport Authority (RTA) and Careem launched Hala, a joint venture that allowed users to book official Dubai taxis through the Careem app.

Later that year, RTA moved taxi booking and dispatch services onto the Hala platform, effectively shifting a large part of taxi demand from telephone-based and street-based matching to app-based digital dispatch.

By integrating taxis into a digital booking platform, Dubai improved the speed and precision of trip allocation. This raised utilisation rather than simply subsidising losses.

In that sense, the policy worked as a form of indirect protection: it did not compensate drivers for declining competitiveness, but instead improved the competitiveness of the regulated taxi system itself.

The available operational results support that interpretation. Dubai’s taxi sector posted growth of 7% in the first half of 2025 compared with the same period in 2024.

Hala Taxi’s market share also increased to 41.3% of total taxi trips in H1 2025, up from 40.3% in H1 2024—a rise of 2.5% growth in share. Over the same period, the number of active drivers in the sector grew from about 13,000 to nearly 14,000. Dubai did not simply hand the taxi market over to ride-hailing economics. Instead, it kept a pricing framework in place.

Hala uses surge pricing during busy periods, but the maximum increase is capped at 1.3 times the base fare — far more controlled than the open-ended price spikes common on other ride-hailing platforms. That combination of app-based convenience and regulated pricing is what makes the Dubai model distinctive.

Conclusion

The broader insight is that taxi drivers can be protected in more than one way. Saudi Arabia faces a real choice here. One path is direct compensation — a dedicated fund for eligible drivers that cushions the financial impact of market disruption.

The other is structural redesign, following something closer to the Dubai model, where drivers are protected not through payments but through better demand allocation, lower idle time, faster dispatch, and deeper integration into digital mobility platforms.

The case for looking at Dubai is not that it offers a ready-made template, but that it proves transition costs in the taxi sector can be absorbed through system reform rather than subsidy alone.