Saudi Arabia has largely moved past the question of whether it can produce startups. The more important question now is whether it can produce enough companies that scale from Series A to Series B and beyond.

That is the real test of ecosystem maturity. Headline funding growth matters, but it is not the same as scale-up formation.

Saudi venture funding accelerated sharply after 2020, and the market remained active in 2025, with H1 funding reaching $860 million across 114 deals.

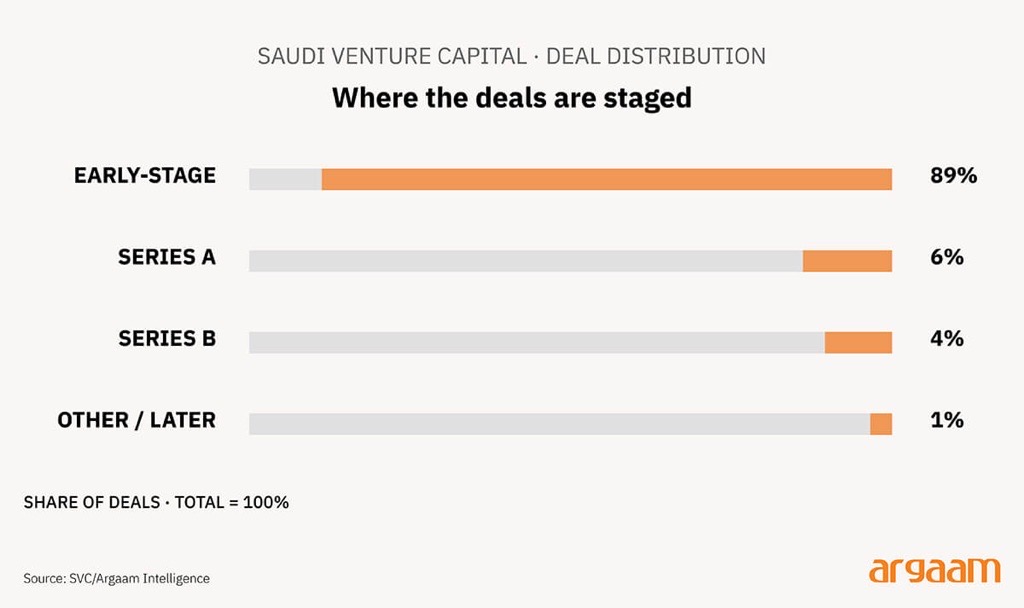

Yet the stage mix still shows where the bottleneck lies: early-stage deals accounted for 89% of transactions in H1 2025, while Series A represented 6% and Series B only 4%. In other words, startup creation is no longer the main constraint; mid-stage depth is.

Measuring exactly how many Saudi startups successfully move from one funding stage to the next is difficult — simply because the data does not yet exist in the organised, trackable form that more mature markets have built over decades.

And even in places like the US where that data does exist, the journey between funding rounds is rarely quick or straightforward.

Rather than pretend otherwise, this report takes four practical angles to assess where the Saudi startup ecosystem actually stands today: how funding is distributed across early and late stages, what the investment portfolio of Wa'ed — Saudi Aramco's venture arm — reveals about startup progression.

How government and quasi-government money is shaping the market, and how Saudi Arabia compares to the US and China at similar points in their venture capital development.

Saudi Arabia’s venture market already shows where the bottleneck lies: not in generating startup activity, but in building a sufficiently deep mid-stage pipeline to carry those companies into scale.

By 2024, the Kingdom had become the largest VC market in MENA by both funding and deal activity, with $750 million invested across 178 deals.

That tells us the starting point of the ecosystem is no longer the main problem. Saudi Arabia is clearly producing founders, startups, and investable early-stage companies at scale.

The issue appears further along the funnel. The same SVC data shows that Saudi venture activity remains heavily concentrated in early rounds, while Series A and especially Series B still account for a much smaller share of the market.

That matters because an ecosystem can look vibrant at the startup-creation stage while still lacking enough depth in follow-on capital, investor specialization, and operating maturity to consistently turn those startups into scale-ups.

This is also why graduation is hard to measure directly. Saudi Arabia’s venture ecosystem is still young enough that many A-round companies are effectively still in the pipeline, rather than clearly successful or failed.

Even in the United States — where startup data is detailed and well-tracked — companies are taking longer than ever to move from one funding round to the next, with the typical gap between Series A and Series B stretching to nearly three years by early 2025.

In Saudi Arabia, where far fewer companies have reached that middle stage and the ecosystem itself is still young, trying to calculate a single definitive graduation rate would give an icoomplete picture — because most of the data simply is not mature enough yet to tell the full story.

A useful way to approach Saudi Arabia’s scaling question is to look at a portfolio sample rather than pretend that a complete national dataset already exists. Wa’ed Ventures is a reasonable proxy for that purpose.

It is one of the Kingdom’s most visible state-linked technology investors, backed by Aramco through a $500 million fund, and its public portfolio spans sectors such as artificial intelligence, fintech, robotics, e-commerce, drones, quantum computing, logistics and other frontier or operational technologies.

That makes it broad enough to be informative, even if it is not a substitute for a full market-wide cohort database.

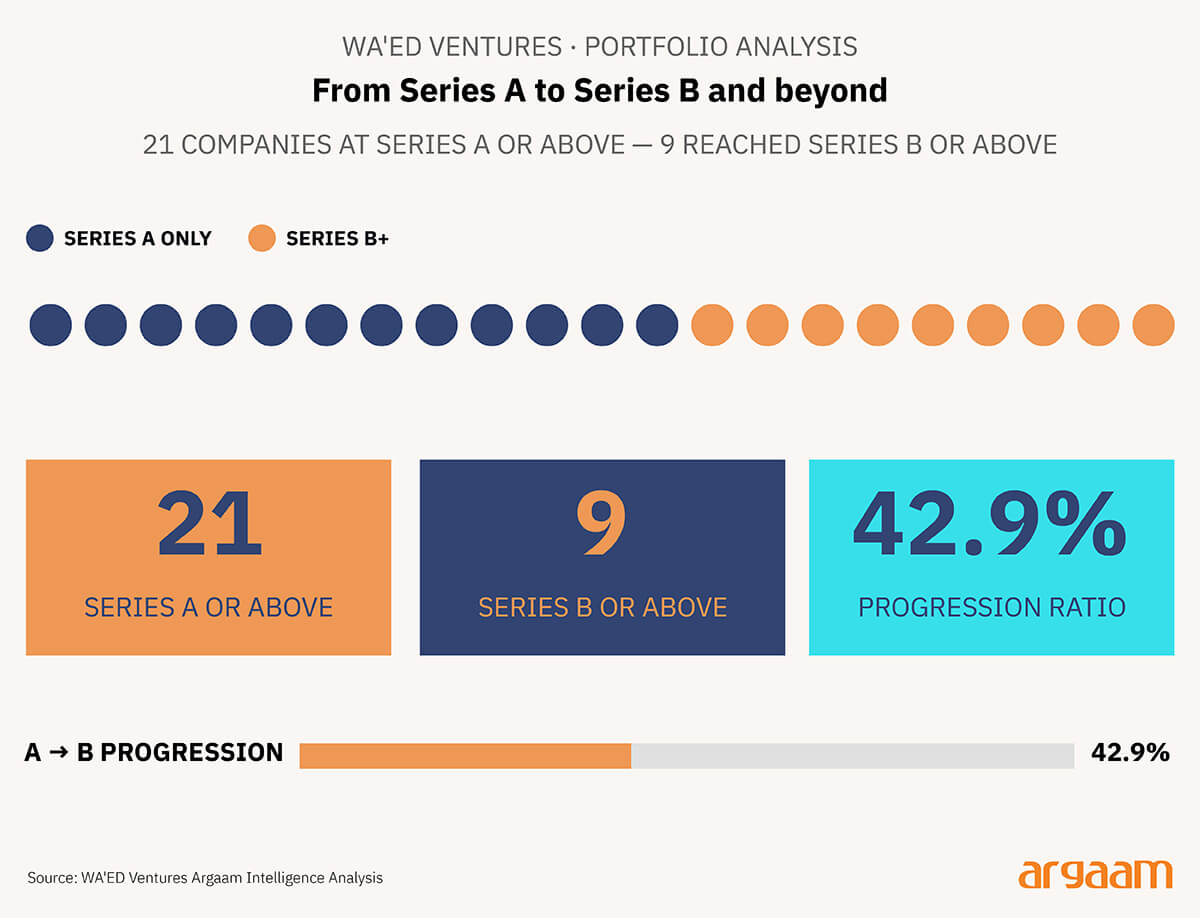

Looking at Wa'ed's public portfolio page, 21 of its companies have raised a Series A round or beyond, and 9 of those have gone on to raise a Series B or beyond.

That works out to a progression rate of roughly 42.9%, meaning nearly half of the companies that cleared the Series A milestone have continued growing and secured even larger funding rounds.

This is not a formal Saudi national graduation rate, and it should not be presented as one. But it is still useful. It suggests that, within an important Saudi-linked technology portfolio, progression beyond Series A is clearly happening.

In other words, the ecosystem is no longer only generating startups at the front end; it is also beginning to produce a visible layer of scale-up candidates.

The limitations matter. This is a single-investor sample, not a full market census. Portfolio companies entered at different times, so a 2024 Series A company has had much less time to progress than a 2020 one.

The stage labels on Wa’ed’s site usually reflect the round in which Wa’ed participated, not always the company’s full fundraising history.

How quickly a startup grows depends partly on what it does. A portfolio full of deep-tech or hardware-heavy companies will naturally take longer to mature than one built around software businesses. That distinction matters in Saudi Arabia, where startups are not all working to the same timeline.

Software, SaaS, fintech, and many AI companies tend to move faster because they can build, test, and start generating revenue without much physical infrastructure.

Recent analysis from Bessemer Venture Partners on AI-native software companies also suggests that some parts of the software market are now scaling revenue unusually quickly, which means certain digital businesses can reach later funding stages faster than was previously typical.

By contrast, robotics, drones, industrial technology and smart-city infrastructure usually move more slowly because they require longer R&D cycles, technical validation, pilot deployment and real-world integration before the next funding milestone becomes credible.

McKinsey notes that deep-tech ventures often take around 12 months longer than traditional tech companies to progress from seed to Series A in the early stages, precisely because scientific and engineering risk must be reduced before capital can scale.

This is why the mix of companies in Saudi VC portfolios matters. Most tend to focus on technology and localization, with investments spread across areas like AI, drones, cloud, and IoT rather than being concentrated in consumer internet or pure software businesses.

That makes it easier to understand why funding progression can look slower — companies in these sectors simply take longer to hit the milestones that attract later-stage investors, which does not mean they are underperforming.

The Institutional Architecture Behind Saudi Venture Finance

Saudi startup finance cannot be understood through private VC alone. A more accurate lens is sovereign and quasi-sovereign capital: capital linked directly or indirectly to the state through vehicles such as PIF-backed platforms, government-backed funding institutions, and state-linked corporate investors.

This matters because Saudi Arabia’s venture market has been built not just by private risk appetite, but by institutions designed to expand the market itself.

SVC, for example, says it has invested in 60 private capital funds that together have backed 800+ startups and SMEs through around $3 billion in assets under management.

Government venture capital can channel funding toward firms that private investors may overlook, especially when it works alongside private investors rather than replacing them.

In practical terms, that can mean stronger credibility, more patient capital, and better follow-on support for startups operating in sectors with longer development cycles.

But government-linked capital can also crowd out private investors, fund weaker projects, or soften the competitive pressure that normally forces startups to hit milestones quickly. That is why the key question is not whether sovereign capital is good or bad in principle.

The real question is whether startups are reaching later stages because they have earned it through growth, or because the system is designed to keep them alive.

The more revealing metric over the next few years will be whether those Series B and beyond companies are generating real revenue, attracting international co-investors, and eventually exiting — that is the true test of whether Saudi sovereign capital is building a market or just funding one.

Saudi Arabia’s 2024 VC report points to a growing exit story, including IPOs such as Rasan, Nice One and Jahez, but visible exit activity is still limited relative to the size of the early-stage pipeline.

◎ Capital without growth is just noise.

◎ Slow timelines hide whether companies are scaling or just surviving.

◎ The real scorecard is revenue, foreign investors, and exits — not round counts.

Stop Comparing Saudi Startups to Silicon Valley

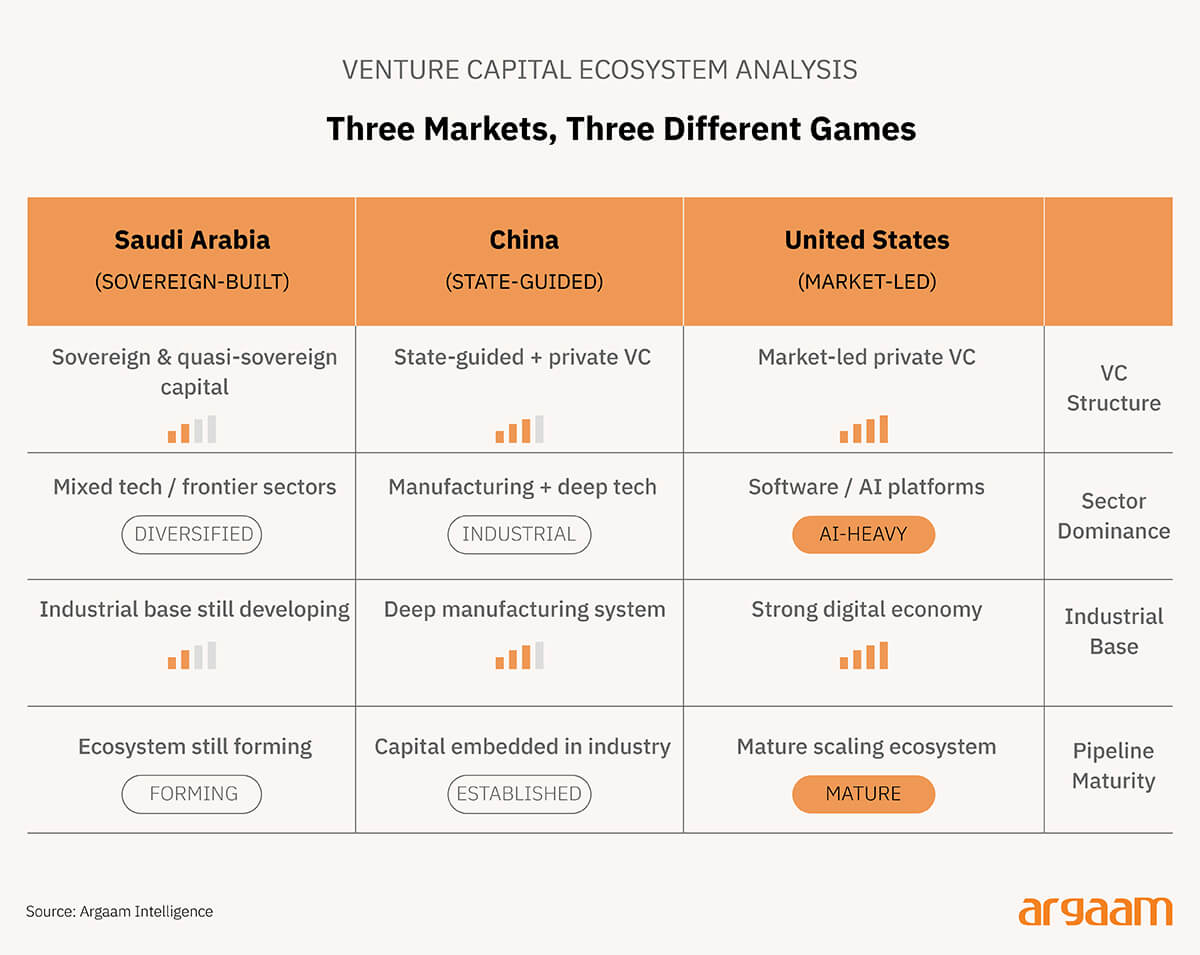

Saudi Arabia's startup market does not look like the US or China, and it should not be judged by their standards. It is a young, state-supported ecosystem that is still developing the middle layer of its funding pipeline — the stage where companies move from early bets into genuine scaling businesses.

The US operates a more market-driven venture system with clearer patterns for how companies progress between rounds.

That is partly because the American market is so heavily weighted toward software and AI — recent data shows that AI and machine learning accounted for 65.6% of all US venture deal value in 2025 — and software businesses tend to scale faster and follow more predictable funding timelines.

Saudi Arabia is different. Its portfolio is more spread across hardware-heavy and frontier technology sectors, state-linked capital plays a much larger role, and the mid-stage funding layer is still relatively thin.

That makes direct comparisons with the US misleading. The more useful question is whether Saudi Arabia is making progress on its own terms, not whether it matches benchmarks built for a different market entirely.

ℹ︎

Different Market, Different Rules

◎ The US is market-led; Saudi Arabia is state-built.

◎ American VC is dominated by software and AI, which compress funding timelines.

◎ Saudi startups tend to operate in more complex, infrastructure-heavy sectors that simply take longer to build — so slower funding progression is expected, not alarming.

◎ The right benchmark for Saudi Arabia is its own progress, not Silicon Valley's.

China offers a different comparison. Like Saudi Arabia, it has strong state-linked capital influence, but it sits on top of a far deeper industrial base.

China’s share of global manufacturing production rose from 5% to 35% between 1995 and 2023, and now exceeds the combined manufacturing output of the next nine largest manufacturing countries.

Chinese venture capital is not just helping build an ecosystem.It is embedded in an already broad manufacturing and industrial system that can absorb, test and scale technology more quickly.

That is why Saudi Arabia cannot simply borrow American or Chinese A-to-B expectations as if they were universal benchmarks.

Conclusion

The funding round is not the finish line — it is just evidence that someone believed in the company at a point in time. What matters is what came after: whether the business kept growing, found an exit, or faded quietly. That is the only scorecard worth reading.