This report is produced for informational and analytical purposes only. Nothing in it constitutes investment advice, a recommendation to buy or sell any asset, or a solicitation of any kind. Readers should not treat this analysis as a substitute for independent professional advice.

King Salman International Airport is not simply a transport project. It anchors a 57 square kilometre aerotropolis in northern Riyadh — a planned urban district built around the airport as its economic core, zoned for residential, commercial, logistics, hospitality and mixed-use development, with a target completion date of 2030.

The real estate question this raises is straightforward but consequential: do today's land prices around the site already reflect what the airport will become, or do they still reflect what the area currently is? The gap between those two valuations — if it still exists — is where investment returns are made or lost.

Proximity to major international airports generates measurable and sustained uplift in land values, particularly for commercial and logistics uses.

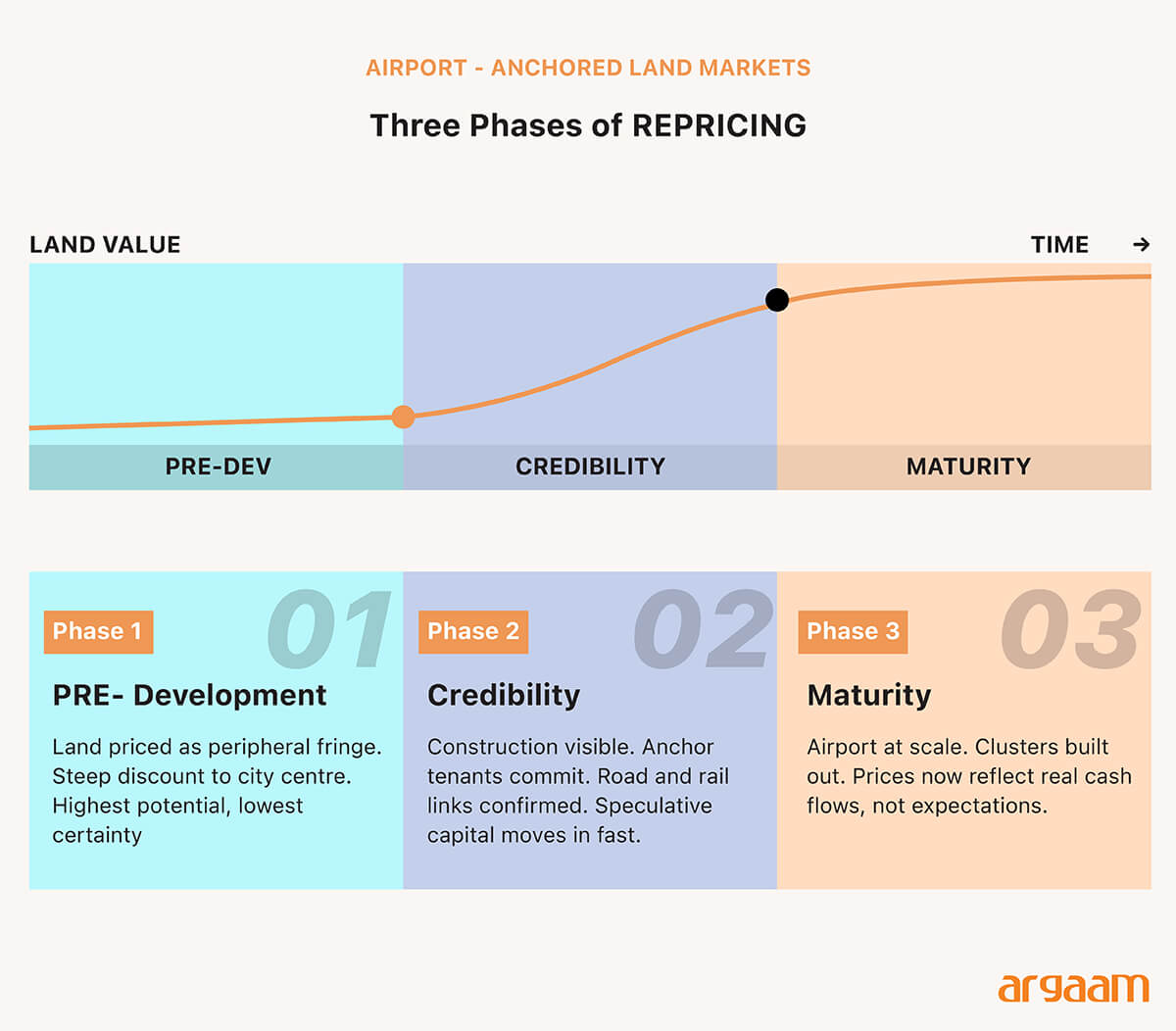

But that uplift is not evenly distributed across time. Early movers capture the largest share of the appreciation. By the time infrastructure is operational and tenants are signed, much of the premium is already priced in.

Classical urban economics has a simple rule: land is most valuable at the city centre and loses value as you move away from it, because distance means higher transport costs and worse access to where people and businesses want to be.

This is bid-rent theory — tenants bid more for central locations because centrality saves them time and money. Large hub airports break that rule by creating a second centre of gravity.

For certain types of businesses, being close to a major international airport is worth more than being close to the traditional city centre.

✦ Note on phase 2: If the airport is delayed, or demand comes in below expectations, or interest rates shift — the price he paid can no longer be justified by any real numbers. The buyer did not buy land at its actual value. The buyer actually bought a dream at a premium. So, the early mover buys the opportunity. The late mover buys the expectation. And the difference between the two is where the profit margin.

Evidence from Airport City Benchmarks

The closest regional comparison is Dubai South, the district built around Al Maktoum International Airport. For years it traded at a steep discount to established Dubai locations like Downtown, Business Bay, and Dubai Marina — reflecting its distance from the city centre, incomplete roads and infrastructure, and an uncertain timeline for when the airport would actually operate at scale.

That began to change when Dubai confirmed a USD 35 billion airport expansion and gave a clearer schedule for shifting most passenger operations to Al Maktoum.

Recent brokerage data and market commentary suggest land and property prices in Dubai South have re-rated sharply, with projected increases in the 15–20% range as the expansion accelerates — on top of earlier gains from what were very depressed starting levels. Values there still sit below core Dubai, but the discount has narrowed considerably.

A similar pattern played out around Navi Mumbai International Airport, where neighbourhoods such as Ulwe and parts of Panvel recorded cumulative price increases of 70–110% as the airport moved from planning into active construction and supporting metro and transport links became real. That significantly outpaced broader Mumbai price growth over the same period.

Around Noida International Airport and the Yamuna Expressway corridor, land repriced strongly once road connections, industrial zones, and airport concessions became credible — though from much lower base prices than Mumbai or Dubai.

ℹ︎

Note

● Timing is everything, not trajectory.

The total return from airport land is less about the long-term direction — which is almost always upward — and more about which specific moment you enter. Miss the milestone triggers and you buy the expectation rather than the opportunity.

● Infrastructure is the investment thesis, not the airport itself.

The airport creates the logic but it does not create the value alone. Roads, metro lines, and logistics corridors are what convert proximity to an airport into genuine economic demand — without them, the district stays an island regardless of how large the airport becomes.

●Know what the land is worth at maturity, not just what it costs today.

Airport districts start cheap and rise, but they rarely reach parity with established city centres. Investors who underwrite returns assuming full convergence with prime urban pricing will be disappointed. The discount to the CBD is structural and persistent, especially for residential — building that into the model from day one separates disciplined analysis from wishful thinking.

The price hierarchy across Riyadh

The price hierarchy across Riyadh is not just background context — it is the baseline against which the airport land opportunity is measured.

Without knowing where land currently sits in the city's pricing structure, you cannot assess whether land near KSIA is cheap, fairly priced, or already expensive.

So, the following price explainer is the map. The airport is the event that could redraw it.

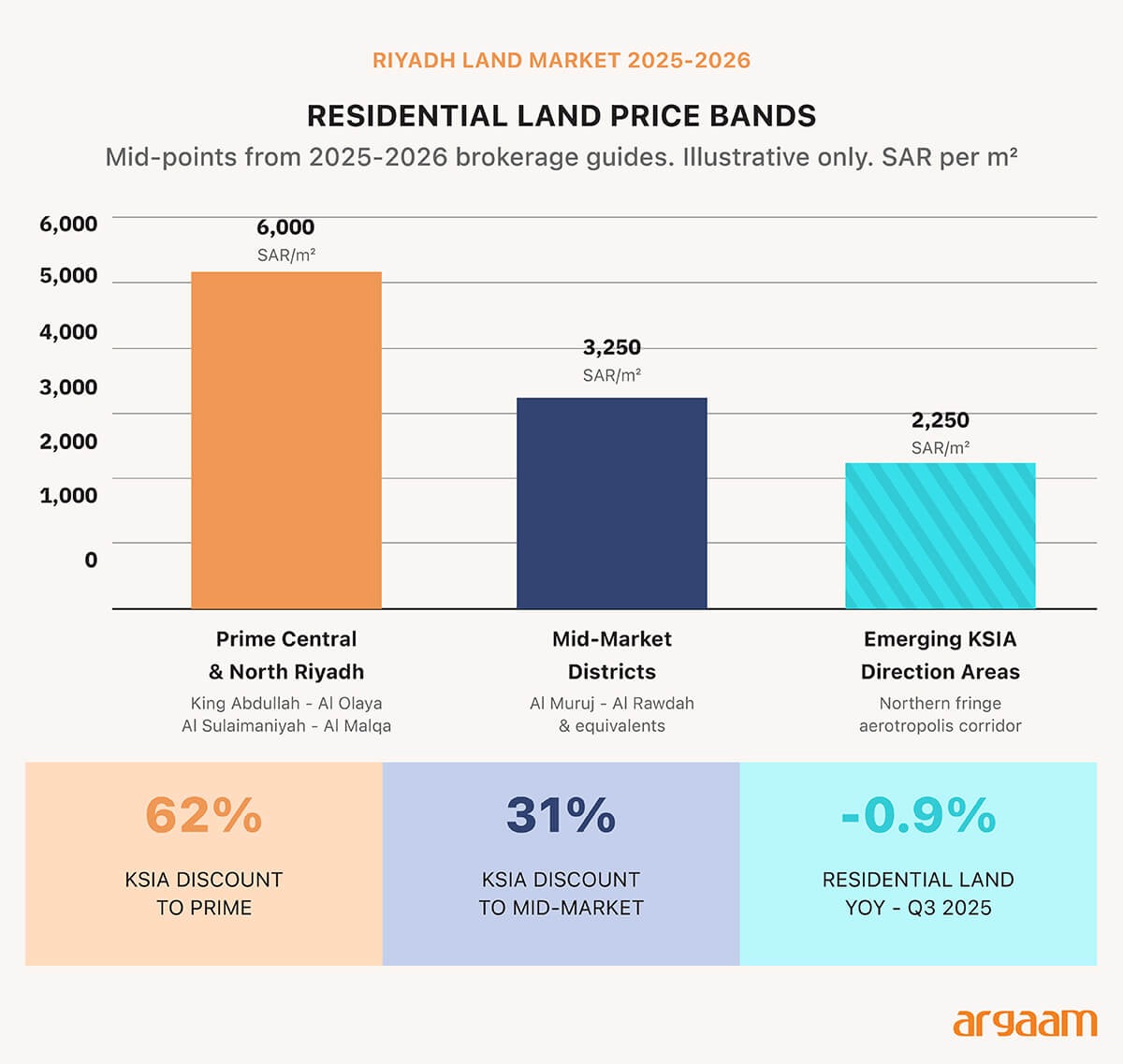

Riyadh's land market has a clear hierarchy — prices vary significantly depending on where you are in the city, and that gap reflects real differences in income levels, infrastructure quality, and access to amenities.

At the top end, residential land in prime central and northern districts commands the highest prices. Areas such as King Abdullah, Al Olaya, Al Sulaimaniyah, and Al Malqa typically range from around SAR 3,300 to SAR 8,700 per square metre, with King Abdullah district at the upper end of that range.

Mid-market districts such as Al Muruj and Al Rawdah sit in the SAR 3,000–3,500 per square metre range. Southern and some eastern districts are considerably cheaper, often between SAR 1,000 and SAR 1,250 per square metre — a reflection of lower household incomes, weaker infrastructure, and fewer nearby services.

Commercial land follows the same pattern. Prime northern commercial corridors cluster at or above SAR 3,000 per square metre, while secondary commercial areas typically fall in the SAR 1,400–2,100 range.

After a period of strong gains, the market has entered a calmer phase. According to GASTAT's real estate price index, residential land prices edged down 0.9% year-on-year in the third quarter of 2025 — a modest correction rather than a reversal, but a signal that the earlier momentum has cooled.

KSIA's northern Riyadh location puts it on the city's growth axis, but still at the edge of today's urbanisation.

Early MoUs with local and international developers indicate that some land use parcels are effectively pre allocated for large, master planned schemes rather than fragmented retail plots. A meaningful share of the "airport surplus" may therefore be internalised by state linked entities and master developers, limiting pure land plays for smaller investors and anchoring prices in institutional expectations about connectivity and tenant mix.

Public listing and guide data suggest that land in emerging northern and north eastern districts that lie along the KSIA growth axis is generally priced below prime north Riyadh, typically in the indicative 1,500–3,000 SAR/m² band depending on plot size, zoning, road access.

Where parcels are explicitly marketed as "near future KSIA" or along key connecting corridors, asking prices sometimes incorporate a modest premium to undifferentiated fringe land but still sit at a discount to established northern neighbourhoods such as Al Malqa and Al Yasmin. The market recognises the airport story, but does not yet price land as if KSIA were fully operational.

Compared with Dubai South and Navi Mumbai and Yamuna airport corridors at similar stages, KSIA direction land still trades at a relatively wide discount to core city districts, indicating that airport city upside is only partially priced in

Concluding remarks:

The real concern here is not whether land prices are rising — it is whether they are rising in the right sequence. If land near KSIA reprices too quickly, before the logistics activity, passenger volumes, and urban amenities are actually in place, the result is high entry costs that deter serious long-term investors and attract speculators instead.

But if land stays too cheap for too long, the opportunity to use rising values to fund infrastructure and public services is wasted. The goal is not cheap land or expensive land — it is land that reprices in step with real development.

The opportunity near KSIA has not disappeared, but it is shrinking. Right now, there are still plots of land in northern Riyadh — close to where the airport's roads and freight routes will run — that are priced as if the airport is not coming. Those plots are the opportunity.

Once construction accelerates and major tenants start committing, those same plots will be priced as if the airport is already there. That is when the easy return disappears.

Investors who approach KSIA primarily as a future luxury residential story risk paying too much too early. Those focused on logistics, light industrial, and business-service uses are likely to find a more compelling return profile over the next five to ten years.

For patient investors who can absorb execution and timing risk, that remaining gap — between today's fringe-plus pricing and the levels consistent with a mature northern airport city — is where the residual opportunity lies.

The distinction between these two categories is fundamental for valuation. In the coming phase, AI will not act as a displacement force for these companies, but rather as a benchmark for their ability to enhance margins and improve return on capital.

More this Weekend

SISCO HOLDING Holding's PSS Acquisition Is a Bet on Future Value, Not Current Earnings

Saudi SISCO HOLDING , through its logistics platform LogiPoint, recently acquired a 51% stake in Public Storage Solutions (PSS).Before outlining out objective analysis, we would first establish the strategic logic behind the bargain.

Data Is Not a Commodity: How AI Is Rewriting the Pricing Rules

Saudi Arabia is rapidly building an AI-driven economy, but the way value is currently assigned to data risks falling behind the way AI actually creates that value. Today, most Saudi data and content creators are compensated through one-time payments, even though the AI models trained on them continue to generate revenue long after training ends.