Rent defaults have become an increasingly pressing issue in Dubai’s real estate landscape, reflecting underlying systemic challenges within the current old-fashioned policy of rent collections.

Rent defaults have more than doubled, and late payments have tripled, in just the last year, according to independent estimates. The core issue here is the timing of cash flows, with quarterly or annual cheques being the most common method used.

Our suggested new policy is converting rent, which’s traditionally “dead” expense in a household, into a source of redeemable value through a rewards-based credit card with zero transaction fees.

Monthly digital rent payments create a rich behavioural dataset that can be used to assess creditworthiness more accurately than annual cheques. This reduces information asymmetry between tenants, landlords, and financial institutions.

Dubai would not be the first to use rewards to incentivise frequent, low-sum, rent payments. Bilt Rewards, a US Fintech platform, lets customers earn Bilt Points for on time rent payments.

These Bilt Points can then be redeemed for a range of different types of rewards, such as complimentary items when dining or free gym classes. Every dollar spent on rent gives its customers Bilt Points, a $2000 dollar rent payment gives 2000 Bilt Points.

Bilt’s model is very successful, it boasts millions of American customers, and works with the majority of the US’s top 100 property managers. The company says that Bilt’s model reduces delinquencies by 12% and increases on time payments by 30%.

In this system, the points earned per dirham increases as overall spending increases.

As an example, two points per dirham are earned after 100 dirhams have been spent in total, and three points per dirham are earned after 200 dirhams have been spent.

Accelerated rewards improve how motivated customers are to earn these rewards, and this perception of added value results in extra spending.

If a tenant in Dubai gains extra rewards over time, they are more likely to participate in the on-time rental payments scheme, ensuring that landlords receive their pay promptly.

ℹ︎

Note

The shift from checks to credit cards doesn’t just change the payment method — it redefines who owns the core financial relationship in the rental market.

In the traditional model, the landlord maintains a direct relationship with the tenant, while the bank’s role is limited to executing the transfer.

But once credit cards are introduced, the point of control moves to the entity that manages the payment instrument, which then becomes able to… ● To achieve stable monthly cash flow data ● build a more accurate credit history linked to rent ● and develop additional financial products based on the same relationship

This shift opens the door to competition among three major players: ● banks ● fintech companies ● and property management platforms

A Win-Win Strategy for Banks

Zero transaction fees for rent payments are another component of our suggested rewards-based credit card - no fees for the tenant or for the landlord.

But if banks are not receiving their interchange fees, why would they facilitate these payments?

Well, on top of paying monthly rent, tenants can use this special credit card for their own everyday expenses. We extend in our suggested new policy the rewards from earning points via rent payments, to earning points from all payments made using the credit card.

Thus, everyday expenses using the credit card will still incur the regular interchange fees. Also helping our case, real estate interchange fees (between the bank and the credit card issuer) in the UAE are 0.65% and capped at 32.50 AED.

In contrast, credit cards for general purchases can reach fees up to around 2%. This makes it very easy for the bank to earn its interchange fees back.

Merchant Segment Rate Programs

Debit and Prepaid Consumer Cards Rates3

Government and Utilities

0.50% cap AED 25.00

Transport

0.50% cap AED 25.00

Petrol

0.50% cap AED 25.00

Education

0.65% cap AED 32.50

Real Estate

0.65% cap AED 32.50

Charity

0.65% cap AED 1.00

Exchange Houses

AED 2.00

Source: VISA UAE/Argaam Intelligence (2024 data)

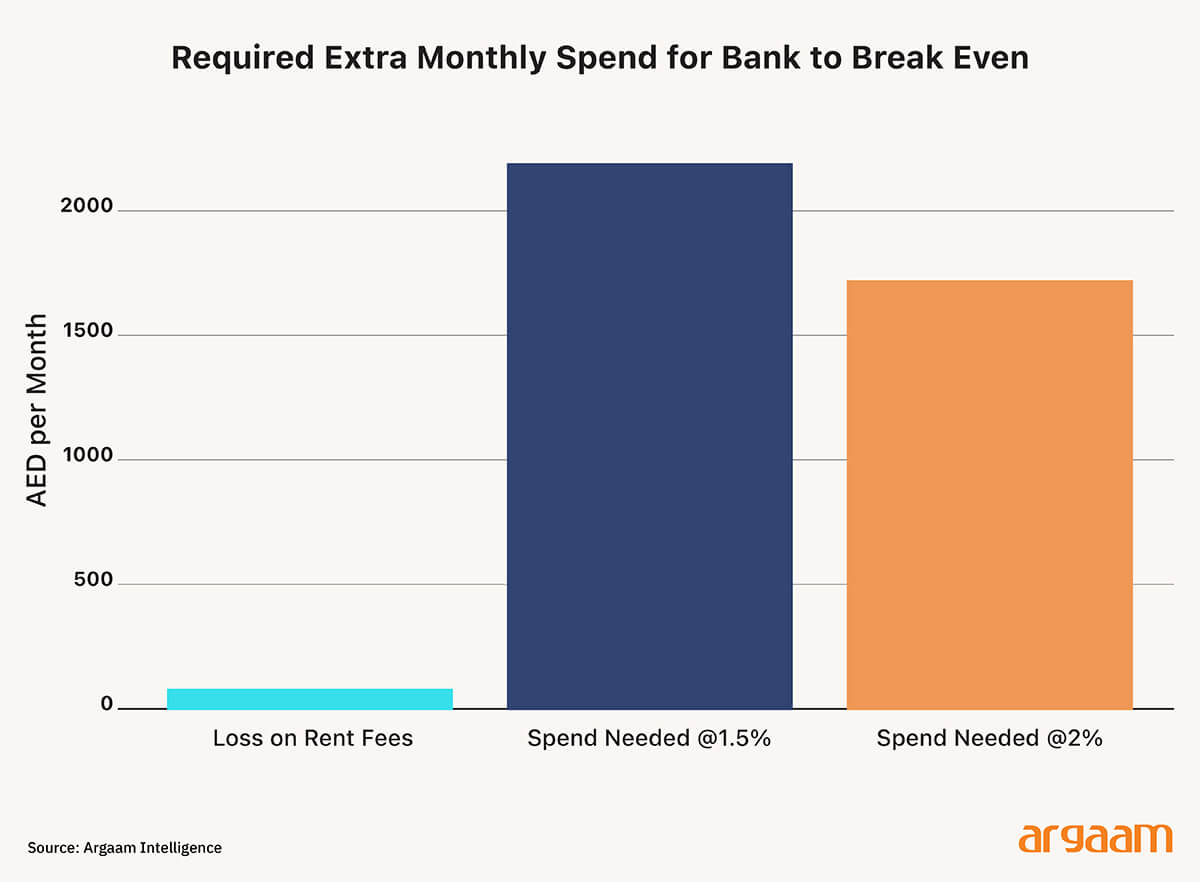

As seen in the graph above and with interchange fees are capped at 32.50 AED with 1.5% interchange fees, the bank would need the tenant to spend around 2100 AED extra above the rent a month to break even.

At 2% interchange fees, the bank would need the tenant to spend around 1600 AED extra a month to break even. Of course, if the tenant spends more than these amounts then the bank now profits overall, and if the tenant spends less then the bank is losing money and this isn’t sustainable.

Interchange fees in the USA are also slightly higher, with fees reaching up to around 3%, so banks could be profiting extra consumption in the USA more than they would do in Dubai.

The American Bilt business model has a solution, its credit card system provides 4% cashback on all purchases. This is also profitable for banks, as it encourages consumers to spend more and especially encourages more expensive purchases.

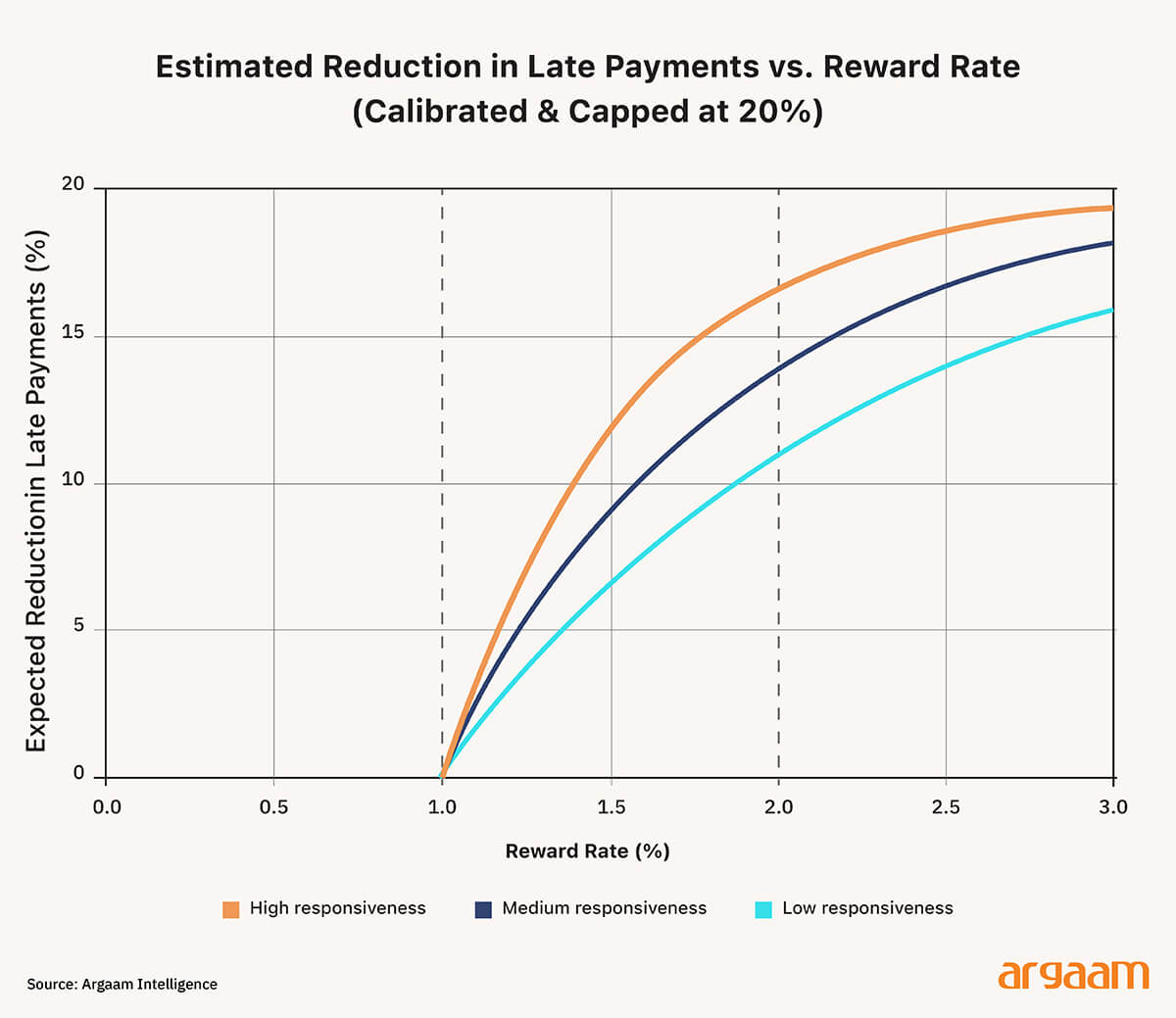

The graph above shows an estimate of how much late payments would reduce at different levels of rewards - depending on how responsive the tenant is to the incentive. The curves all start at 1%, a commonly agreed point at which behavioural effects start.

◆ Low responsiveness (red): tenants don’t change behaviour much even when rewards rise ◆ Medium responsiveness (blue): moderate behavioural change ◆ High responsiveness (green): tenants strongly adjust behaviour to earn rewards

All three curves slope upward. This means that as the reward rate increases, tenants are more motivated to pay on time. At 1%, reductions are modest across all scenarios.

At 2%, the gap between low, medium, and high responsiveness becomes much more pronounced.

But exactly how much would a rewards based, zero fee, credit card reduce delinquencies and defaults in Dubai? Well, as said before Bilt claims its users have 12% less delinquencies and 30% more on time payments. So perhaps we could expect a similar reduction in Dubai.

It is worth noting, in the USA, smooth monthly payments are already common. These smoother, frictionless payments are not yet common in Dubai so introducing it could make further reduction in the number of delinquencies.

This helps policymakers choose a reward rate that balances cost (reward expense) and impact (reduced delinquencies).

If Bilt was able to reduce defaults by 12% and boost on-time payments by 30%, it’s not absurd to think our system in Dubai would produce similar (or better) results. Especially if accelerated rewards specifically for rent payments, something Bilt lacks, successfully motivates tenants to pay on time.

Concluding remarks:

What This Means for Dubai’s Rental Market? It means that the incentive structure can be cost‑efficient, scalable, and targeted—especially when paired with data that identifies which tenant segments respond most strongly to behavioural nudges.

By linking reward rates to measurable reductions in late payments, the system transforms rent collection from a volatile, cheque based model into a predictable, model driven cash flow environment as it happened with millions of tenants across the United States.

Note

This analysis is based on market indicators and international case studies, and aims to understand potential future trends in light of Dubai’s advanced regulatory role in developing its real estate market.

More this Weekend

The Economic Case for Per-Minute Parking Pricing in Riyadh

Riyadh’s current parking lot charge of SAR 3.45 per hour rate, coupled with a 15-minute free grace period, is designed to target a specific occupancy level as an operational goal, assuming that maintaining an optimal occupancy would lead to efficient space utilization.

What Targeted Localisation Could Unlock for Saudi Arabia: An Illustrative Policy Scenario

This paper argues that the current policy framing — centred on broad local content mandates and headline percentage targets — is insufficient and in some cases could be counterproductive. What Saudi decision-makers require is a disciplined, sector-differentiated strategy grounded in the economics of comparative advantage.