This paper argues that the current policy framing — centred on broad local content mandates and headline percentage targets — is insufficient and in some cases could be counterproductive.

What Saudi decision-makers require is a disciplined, sector-differentiated strategy grounded in the economics of comparative advantage and a rigorous assessment of where the Kingdom can realistically compete at cost-competitive scale.

Every dollar of imports that gets replaced by a domestically produced equivalent is a dollar of foreign currency that stays inside the Kingdom permanently. It does not show up on an income statement — it shows up on the balance of payments as a reduced outflow.

In this analysis byArgaam Intelligence, we don’t attempt to present a forecast. What we present here is an illustrative policy scenario—a stylised calculation designed to show the order of magnitude of what could be achieved if certain policy choices and industrial capabilities materialise.

It highlights the strategic opportunity, not the expected outcome.

Our suggested policy should pivot from “build at any cost” to “build with discipline” in the years to come till 2030, with greater scrutiny of the import intensity of tourism, logistics and industrial project pipelines.

Supporting local content can serve not just as an economic policy goal but also as a tool to manage the budget and balance of payments—if efforts are targeted at areas where Saudi producers are able to compete on cost and have the necessary technology.

Choosing the Right Industries to Localise

The theory of comparative advantage in economics establishes the foundational insight of this paper that nations should specialise in goods they produce at lower relative opportunity cost, and trade for the rest.

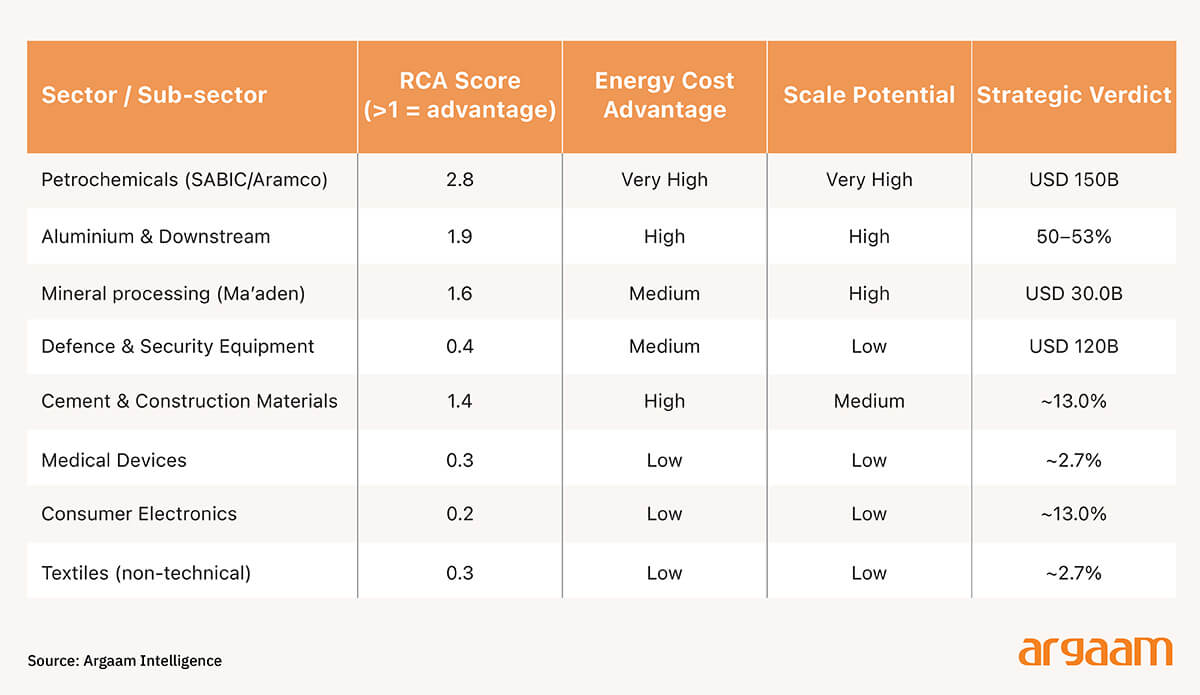

Sector data shows that Saudi Arabia has a comparative advantage concentrated in energy-intensive manufacturing (petrochemicals, aluminium, cement, glass), resource-processing industries (mining, mineral refining), and increasingly — given rapid infrastructure investment — logistics and supply chain management.

It does not imply comparative advantage in assembly-intensive manufacturing (electronics, machinery), skilled-labour-intensive production (medical devices, precision engineering).

In this context, import substitution that is genuinely cost-competitive carries a double economic dividend: it reduces the current account deficit directly (lower import payments) and eliminates the foreign exchange cost of those goods indefinitely.

By contrast, subsidised localisation — where domestic production costs exceed the import price — represents a hidden transfer from the state (or consumers) to the protected industry, which must be financed and crowds out higher-return uses of public capital.

ℹ︎

Stress Test

For each localisation initiative, policymakers should ask — what is the Net Present Value (NPV) of the stream of import savings, net of the subsidy cost and the opportunity cost of capital deployed?

If this NPV is negative over a realistic 10-year horizon, the initiative is not import substitution; it is import-cost substitution with a fiscal price tag.

Note A conceptual clarification that is missing from most localisation policy discourse in the GCC: not all import reduction is import substitution.

There are three mechanisms through which Saudi Arabia can reduce its import bill, and they have profoundly different economic implications: 1) Genuine localisation : domestic production replaces imports at competitive or near-competitive cost. Value is created. Foreign exchange is saved. Employment is generated. This is the target outcome. 2) Demand reduction : lower economic activity, project delays, or fiscal austerity reduce imports by compressing demand. Value is destroyed. This is the wrong mechanism, and one Saudi Arabia should avoid by design. 3)Import diversification : shifting sourcing from high-cost to low-cost foreign suppliers reduces the import bill without localising production.

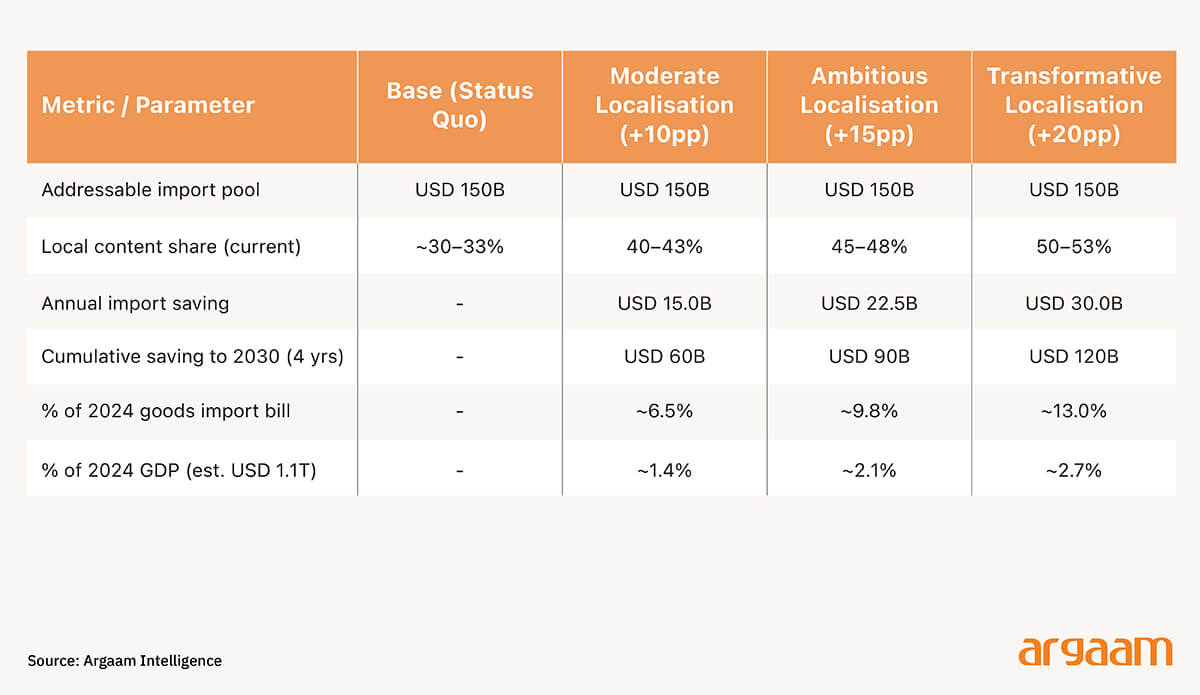

Saudi Arabia's 2024 goods import bill of approximately USD 230 billion can be disaggregated into three categories for localisation purposes.

First, a genuinely addressable pool of approximately USD 150 billion, covering goods consumed or used within the domestic economy where domestic production is plausibly achievable within a 5-10 year horizon, given the right capital, technology, and policy environment.

Second, a structurally non-addressable pool of approximately USD 55 billion, covering goods where Saudi Arabia has no realistic pathway to competitive production — advanced semiconductors, precision pharmaceuticals, certain aerospace components — and where attempting localisation would be economically irrational.

Third, a re-export and transit pool of approximately USD 25 billion, representing goods imported for re-processing or re-export; localisation metrics applied here are misleading.

Within the addressable USD 150 billion, the current local content rate across all categories is estimated at approximately 30–33%, implying that roughly USD 100–105 billion is still being imported despite Saudi Arabia having a theoretical production capability.

The policy question is how much of this remaining import pool can be displaced domestically at acceptable economic cost, and by when.

The Revealed Comparative Advantage (RCA) index — calculated as a country's share of global exports in a given product divided by its share of total global exports — provides an empirically grounded starting point for identifying sectors where Saudi Arabia has genuine production superiority. An RCA above 1.0 indicates comparative advantage; below 1.0 indicates comparative disadvantage.

Concluding Remarks

Every local content requirement imposed on a government project should be accompanied by a fiscal note quantifying the estimated cost premium — the difference between the domestic supply price and the import price — and an economic justification explaining why the industrial and employment benefits justify this cost.

It’s important to note that when local content requirements force buyers to source from domestic producers who are not cost-competitive, the price differential is a dead weight loss to the economy.

If a Saudi government project must purchase locally produced steel at USD 900/tonne when equivalent imported steel costs USD 700/tonne — a difference of USD 200/tonne or 29% — then every tonne purchased under the local content mandate generates a USD 200 transfer from the buyer (ultimately the government or the project's end-users) to the protected domestic producer. This transfer does not disappear; it is simply invisible in the import statistics.

More this Weekend

The Economic Case for Per-Minute Parking Pricing in Riyadh

Riyadh’s current parking lot charge of SAR 3.45 per hour rate, coupled with a 15-minute free grace period, is designed to target a specific occupancy level as an operational goal, assuming that maintaining an optimal occupancy would lead to efficient space utilization. But we argue in this analysis by Argaam Intelligence that this approach to manage paid street parking spaces across key districts could potentially overlook the fact that occupancy is an outcome rather than a direct policy tool. It is shaped primarily by how parking prices are set and how strictly rules are enforced.

Why Dubai’s Rental Market Needs a New Credit Card, Not Cheques

Rent defaults have become an increasingly pressing issue in Dubai’s real estate landscape, reflecting underlying systemic challenges within the current old-fashioned policy of rent collections. Rent defaults have more than doubled, and late payments have tripled, in just the last year, according to independent estimates.