Having larger hotels in Saudi Arabia’s ultra-luxury hospitality sector doesn’t necessarily lead to higher profits. As hotels get bigger and more complex, their value can actually decrease.

This raises an important question for investors: at what point does increasing size improve efficiency, and when does it start to harm the quality of the experience that allows hotels to charge premium prices? Empirical research shows ultra-wealthy individuals pay for ‘how they feel’.

Providing a personalized luxury hotel experience was associated with customers being willing to pay about 14 % more for their stay compared with less personalized services, and that hotels delivering excellent service could generate 5.7 times more revenue than competitors without such experiential strength. This strong focus on creating a unique experience can support higher prices, even without a large scale.

The core economic challenge in luxury hospitality

The economic theory of diminishing marginal utility states that each additional unit of consumption delivers less incremental satisfaction than the previous one.

While adding capacity usually improves efficiency in standard hotels, ultra-luxury operates under a different logic: the product is not the room itself, but the experience surrounding it.

As more rooms are added, common spaces become busier, service becomes harder to personalise, and the emotional payoff of exclusivity erodes.

This non-linear relationship between scale and performance means that while larger hotels can benefit from cost efficiencies, profitability does not rise proportionally with size. Scale alone is not a reliable profit driver. Industry data reinforces our argument.

According to STR and JLL, the two leading providers of performance benchmarking and comparative analytics to the hotel industry, ultra-luxury tourism often prioritises rate integrity over occupancy, accepting lower utilisation in exchange for higher average daily rates.

In practice, this means that expanding room count can reduce pricing power faster than it spreads fixed costs.

The implication is clear for investors: scale in ultra-luxury hospitality is not a volume decision but a pricing decision. Once additional capacity begins to dilute the experience guests are paying for, marginal revenue falls faster than marginal cost — turning growth from a benefit into a liability.

This is a directional economic illustration using publicly listed rate signals“From / Rates start from” and a 100% occupancy assumption to normalise comparability. It is not a realised ADR series or a performance forecast.

Economic theory suggests that beyond a certain point, increasing scale does not automatically translate into proportionate value creation. Unlike scale-driven models, ultra-luxury assets do not rely on spreading fixed costs across a growing number of rooms. Instead, value is concentrated in the pricing power of each individual unit.

A simple Maldives comparison helps clarify this dynamic using publicly listed rate signals. Conrad Maldives Rangali Island, a large-scale branded resort, currently lists entry rates from around $1,102 per night with 151 keys, while JOALI Maldives, a lower-density ultra-luxury property, shows starting rates above $4,000 with 73 keys.

Even after normalising at full occupancy for comparability, the resulting economics diverge sharply. While Conrad benefits from a larger room count, JOALI’s substantially higher nightly rate translates into materially stronger revenue and profit on a per-key basis.

Importantly, this outcome holds even when allowing for higher service intensity and cost structures in ultra-luxury operations. With Maldives-wide GOP margins (Around 33%) constrained by logistics and labour costs, the advantage does not come from superior cost efficiency, but from the ability to sustain premium pricing without dilution.

For investors, the implication is clear: in ultra-luxury hospitality, scale is most effective when deployed through replication of discrete, low-density assets, rather than by increasing density within a single property and risking erosion of pricing power.

The Red Sea: Room count is a pricing lever

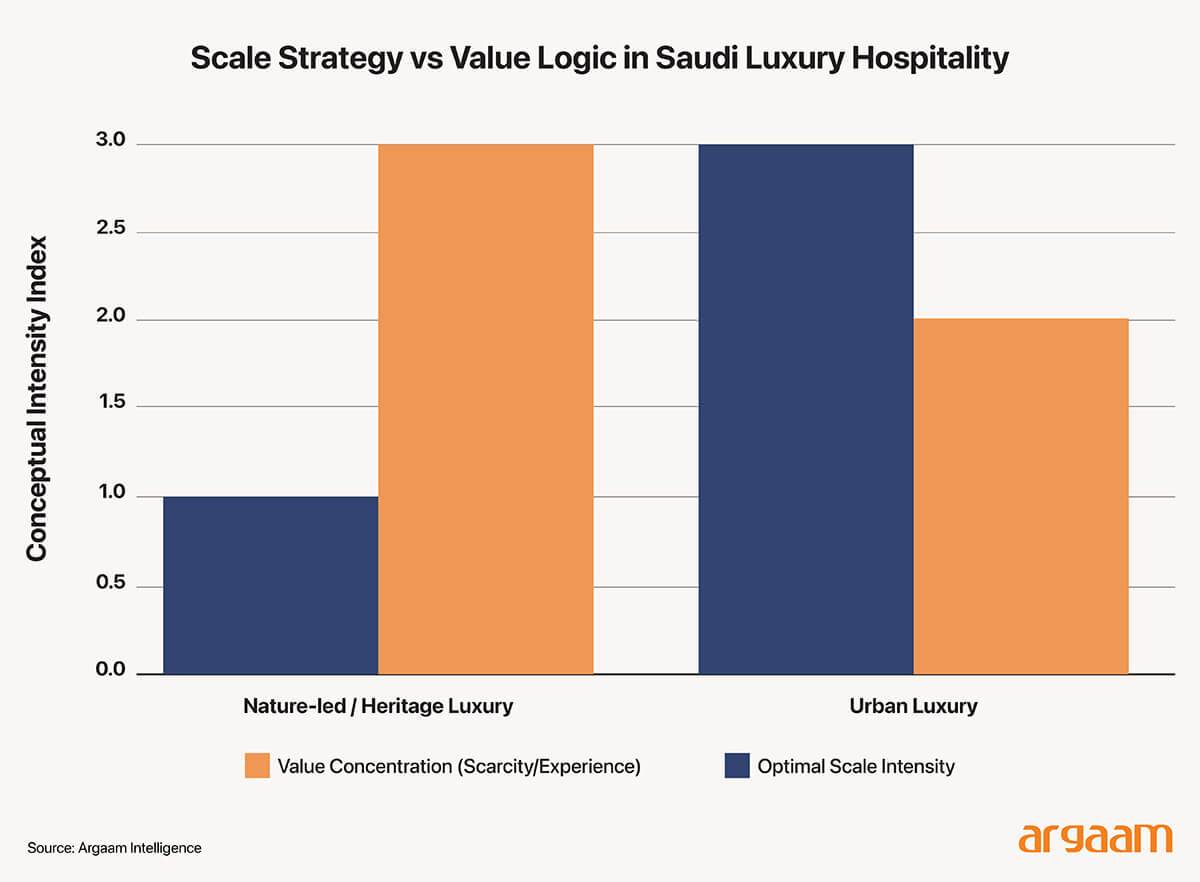

Ultra-Luxury hospitality in Saudi can be grouped into two broad models: nature-led luxury where value comes from privacy, landscape, and emotional “reset” and urban luxury where value comes from location, visibility, and cultural capital.

The Red Sea is the clearest Saudi example of the first model — and it shows why “anti-scale” is not anti-business, but a different profit logic.

The Red Sea destination is being built as a low-density, eco-led luxury proposition across islands and inland sites. Red Sea Global’s own destination plan targets 50 hotels and 8,000 rooms across 22 islands and six inland sites by 2030, while explicitly limiting development to no more than 1 million visitors per year to preserve the ecosystem.

At the ultra-luxury end, Ummahat Islands host two flagship properties: The St. Regis Red Sea Resort (90 keys) and Nujuma, a Ritz-Carlton Reserve (63 keys)—both designed as highly private, experience-first stays rather than high-volume hotels.

Scaling in this context does not contradict the ultra-luxury "less is more" philosophy because the approach emphasizes expanding through the addition of carefully curated, low-density properties across massive pieces of land rather than increasing the size or volume of individual resorts.

In nature-led luxury, room count is a pricing lever, not a production target. The Red Sea’s model protects scarcity by design (remote access, low keys, capped visitation). That scarcity supports higher willingness to pay, because guests are buying privacy, calm, and uniqueness—not more facilities.

Note Dynamic pricing of the Red Sea average daily rate against competitors worldwide represents a distinct analytical domain that diverges from our primary focus in this analysis. Dynamic pricing involves real-time adjustments of prices based on market conditions, competitor actions, and consumer behavior

Importantly, high average daily rate with lower occupancy can still be profitable when the product maintains rate integrity and avoids the operational strain that comes with maximising volume.

The Red Sea’s explicit visitor cap is therefore an economic choice as much as an environmental one: it protects the premium by preventing the experience from being scaled into sameness. Each extra room risks lowering the very utility being sold: privacy falls, silence breaks, and the emotional value of seclusion erodes.

The Red Sea’s explicit visitor cap is therefore an economic choice as much as an environmental one: it protects the premium by preventing the experience from being scaled into sameness.

Each extra room risks lowering the very utility being sold: privacy falls, silence breaks, and the emotional value of seclusion erodes.

Diriyah is a different economic narrative in hospitality

Diriyah/Riyadh is the clearest urban-luxury case. Here, scale is not automatically wrong — but it works through a different economic engine than the Red Sea.

Diriyah is being positioned as a national cultural flagship anchored by At-Turaif, a UNESCO World Heritage site. Urban luxury here is built as an integrated district: heritage, museums, retail, dining, events — plus a cluster of global hotel brands.

Official Diriyah announcements point to more than 40 hotels and over 6,500 rooms across Diriyah and the adjacent Wadi Safar area, with seven newly broken-ground luxury properties alone totaling 877 rooms (including brands like Raffles, Armani, Orient Express, Baccarat, Rosewood). A recent deal also confirms a 159-room Four Seasons Hotel Diriyah.

Urban luxury in Diriyah is driven by cultural capital and visibility, rather than isolation or scarcity. Its value is anchored in three closely linked sources: location rent, through proximity to Riyadh’s high-spend population, government activity, and event-driven demand.

Narrative value, created by the heritage significance and place-based storytelling around At-Turaif; and social visibility, where luxury functions as a public signal of status rather than a private retreat.

In this sense, Diriyah’s luxury positioning is closer to traditional urban markets such as London or Paris, where premium pricing is supported by proximity, recognition, and cultural meaning — not by seclusion.

Scale can help urban luxury by spreading fixed costs (district infrastructure, marketing, event programming) and improving efficiency through shared services. But it also has a ceiling: as clusters grow, experiences become more standardised, luxury becomes high-end but less rare, and pricing power hits a cap.

The result is that scale tends to deliver steadier cash flows, not guaranteed supernormal returns — especially if brand sameness starts to replace true distinctiveness. By contrast, urban luxury projects such as Diriyah operate under a different logic.

Here, scale can support profitability by spreading fixed infrastructure costs, strengthening destination branding, and capturing steady high-spend urban demand. Global city markets show that clustered luxury supply can deliver stable cash flows when supported by strong location and narrative value.

However, policymakers and investors should avoid over-extrapolating the urban model. Even in cities, luxury pricing power is not infinitely elastic. As supply grows and experiences standardise, hotels risk shifting from “rare luxury” to “premium accommodation,” placing a natural ceiling on margins.

Note The chart is our own conceptual synthesis, drawing on industry research (Like average daily rate vs occupancy trade-offs, density effects in luxury resorts) and project-level evidence from the Red Sea and Diriyah. The numbers express relative positioning, not measured outputs.

Concluding thought

The real question for investors in ultra-luxury hospitality is not whether to scale, but where scale supports value creation — and where it destroys it.

Ultra-luxury resorts should place more emphasis on the average daily room rate rather than obsessing over the number of guests. Keeping the number of resorts deliberately small is not a constraint on growth, but a mechanism to protect pricing power and long-term returns.

More this Weekend

What UAE’s AppliedAI’s Valuation Tells Us About the Future of GCC Tech

The UAE’s AppliedAI has recently completed a pre-Series B finacning by Mubadala’s sovereign MENA VC platform. This bridge round follows a $55 million Series A completed in February 2025, backed by a high-profile syndicate including G42, Bessemer Venture Partners and e&.

Assessing Tadawul Software Multiples: the up and down dynamic in the face of the AI re-rating wave

This analysis by Argaam Intelligence explores how leading Saudi IT companies are navigating the significant pressures affecting their global counterparts. Recently, major international technology firms have experienced sharp declines in their valuation multiples as capital has shifted toward frontier AI model builders.