This analysis by Argaam Intelligence explores how leading Saudi IT companies are navigating the significant pressures affecting their global counterparts.

Recently, major international technology firms have experienced sharp declines in their valuation multiples as capital has shifted toward frontier AI model builders.

The focus of this report is to assess whether three leading Saudi software and IT firms listed on Tadawul are facing similar industry-wide challenges and how they are adapting to these dramatic shifts in the global tech landscape.

Have Tadawul Software Multiples Started to Shrink?

Saudi Arabia's listed technology and software universe remains relatively small and is heavily skewed toward IT services, digital platforms, and specialized solutions, rather than pure-play global software or AI model builders. Three representative Tadawul names illustrate the dynamics.

ℹ︎

Hypothesis Under Examination: AI Shock or Valuation Reclassification?

To understand whether the contraction in P/E multiples for Saudi tech companies reflects a deep structural shift or merely a cyclical reset, we propose the following hypothesis: The decline in earnings multiples does not reflect a direct competitive threat from the AI wave.

Instead, it represents a valuation reclassification driven by changing investor appetite toward the global “technology” category.

This hypothesis is grounded in a fundamental difference in business models:

● Saudi tech companies operate under long-term government and semi-government contracts

● Their revenues rely more on executing digital‑transformation projects than on developing global SaaS products

● They do not compete directly in open subscription markets that are vulnerable to immediate technological disruption

Accordingly, testing this hypothesis requires answering two questions:

1) Have the operational fundamentals actually deteriorated (margins, growth, contracts)?

2) Or has the market simply reclassified these companies from “high‑growth tech” to “stable tech services”?

The following analysis attempts to test this hypothesis by examining the three listed cases on Tadawul.

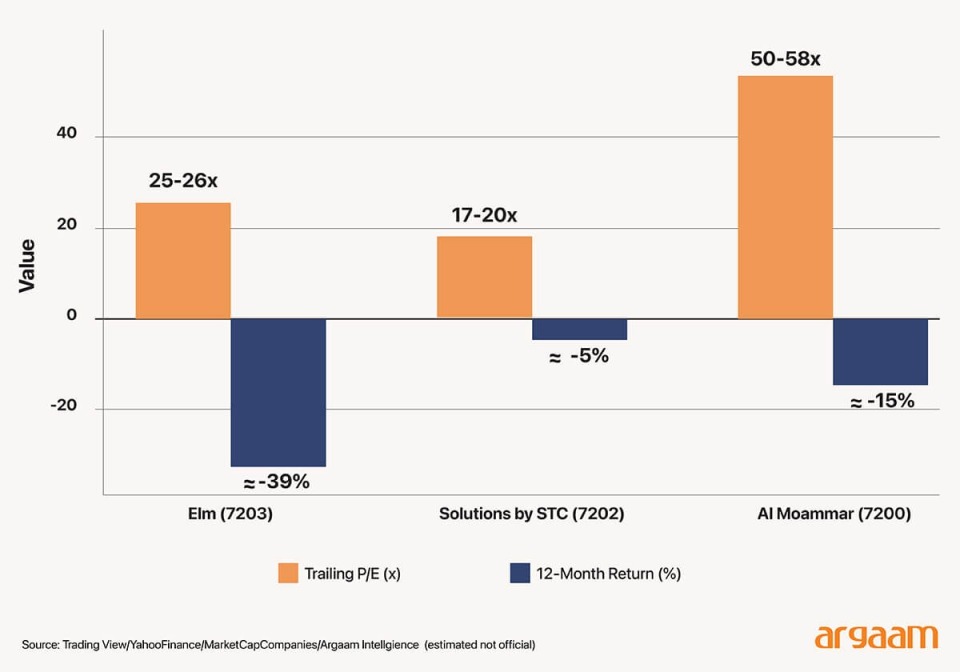

Elm Company (7203) is largest Saudi-listed technology name by market capitalization. Despite strong earnings growth---profit jumped 43% in Q1 2025 and reached SAR 1.64 billion in nine months of 2025---the stock fell as much as 46% from its January 2025 all-time high of SAR 1,289 to a low of around SAR 680 by early 2026, before partially recovering.

Crucially, Elm's trailing P/E has compressed from approximately 47x at end-2024 to roughly 25–26x by early February 2026—a 46% multiple compression that mirrors the global software repricing pattern, as we will explain in detail later in this analysis, despite solid earnings fundamentals.

Market data shows a roughly 39% return over the past 12 months, confirming that there has been a significant change in how assets are valued, no matter which reasonable time period is used to measure it.

✦ Note: there are differences in Elm's prices across different platforms. The highest and lowest prices should be checked against official Tadawul data to ensure accuracy.

Elm's sharp drawdown from its January 2025 peak despite 43% earnings growth—driven by post IPO normalization and the global tech re rating and amplified by the absence of a clear AI enhanced growth narrative—demonstrates that investors already demand more than growth to sustain premium multiples.

Solutions by STC (7202), the IT services arm of Saudi Telecom, trades at a trailing P/E of approximately 17–20x on revenues of SAR 12 billion, down from a 3-year average of approximately 25x and a 5-year average of approximately 27x—a mild compression of 20–35% that reflects its profile as a mature IT services provider rather than a high-growth software play.

Al Moammar Information Systems(7200), a small company with a market value of about SAR 4 to 5.5 billion, is currently valued at roughly 50 to 58 times its recent earnings.

This is similar to its average valuation over the past three years, around 53 times earnings, which means its stock price hasn't changed much in terms of its relative value.

However, there has been a lot of fluctuation from year to year. Recently, its valuation was as low as 38.3 times earnings, suggesting that the higher multiples are mainly due to changes in how earnings are measured trailing the past 12 montths, rather than a permanent change in how investors value the company.

Profit fell 53.7% in Q1 2025, primarily due to exceptional one-off gains in the prior-year comparative period and accumulated subsidiary losses, creating valuation vulnerability.

Tadawul listed software stocks are normalizing, driven primarily by global interest-rate dynamics and sector-wide re rating rather than direct AI displacement.

Crucially, direct AI competitive threat is structurally less acute for Tadawul software names than for global SaaS peers.

Elm and solutions by STC derive revenue primarily from government and semi-government digitisation mandates, national identity infrastructure, and captive enterprise IT services—markets defined by regulatory barriers, local licensing requirements, and long-cycle procurement, rather than the open, globally contestable subscription markets where AI model builders directly erode pricing power.

Al Moammar similarly operates in specialised IT implementation with strong public-sector linkages. This means the valuation pressure these firms face is a second-order transmission—driven by global rate dynamics, sector-wide multiple re-rating, and post-IPO normalization—rather than the first-order competitive displacement that global counterparts as we will explain later in this analysis face from generative AI in creative tools or from AI-native Customer Relations Management alternatives.

ℹ︎

Hypothesis Test: Have the Fundamentals Actually Deteriorated?

● If the decline is structural, we should observe:

● A drop in operating margins

● A sustained slowdown in growth

● Loss of contracts or market share

● Direct competitive pressure from AI driven solutions

If these indicators do not appear, then the downturn reflects a reset in investor expectations rather than a change in the operating model.

Saudi Arabia's Vision 2030 agenda — anchored by SDAIA, NDMO, and a national AI strategy targeting. This plan is supported by larger projects like the USD 100 billion Project Transcendence.

These initiatives create a strong demand for technology and AI solutions, especially through government-led programs and official channels.

This captive demand partially insulates them from global software repricing. However, this advantage is already priced into current multiples—Elm trades at ~25–26x P/E and solutions by STC at ~17-20x, both in-line with or above global IT services peers—and does not exempt Saudi firms from demonstrating AI-enhanced productivity and capital efficiency to sustain valuations as the sector matures.

ℹ︎

Global Repricing or a Shift in the Scarcity Premium?

Global markets have witnessed a rotation of capital from:

● Traditional software companies

to AI infrastructure and foundation model companies

This rotation has created a valuation gap:

● A scarcity premium for specialized AI players

● Multiple compression across the rest of the tech sector

Saudi companies do not fall into the first category, but they also do not face direct displacement — placing their valuations in a middle zone.

Explaining the global context: The shift from ‘Growth at Any Price’ to Multiple Compression

Since late 2021, public markets have systematically repriced listed software and SaaS companies.

Across developed markets, median EV/revenue multiples for software have fallen back toward roughly 2.5–3.5x, while high-quality SaaS names cluster around 5–7x revenues - with the broader SaaS median closer to 5x—well below the double-digit multiples that top growth names commanded at the peak of the zero rate era (2020-2021).

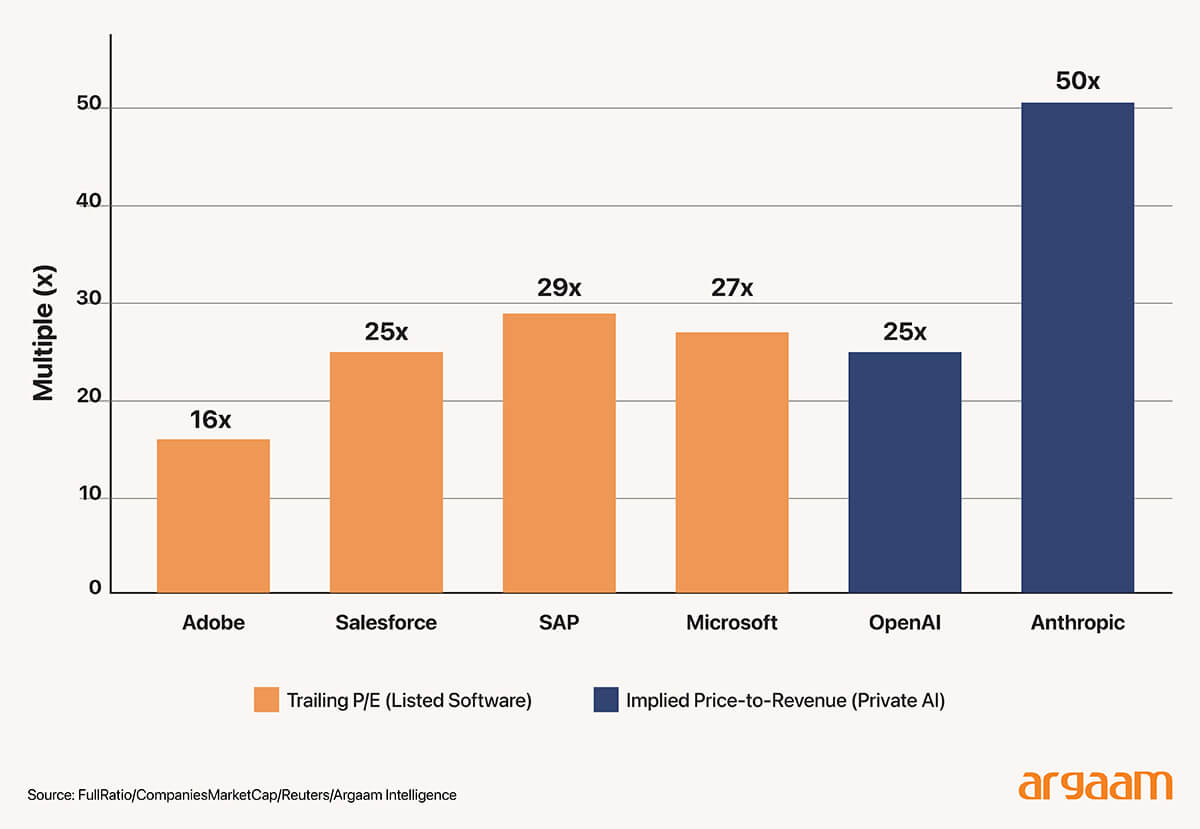

The compression is visible in specific key companies. Adobe's trailing P/E has declined from 51.6x at end-2023 to approximately 16x by early 2026—a 69% compression—reflecting market concerns about AI-driven competition in creative tools and slowing of subscription growth.

Salesforce traded at a P/E of 53x as recently as early 2025, before compressing sharply to approximately 25x by early 2026, as investors demanded profitable growth over top-line expansion.

And, SAP's P/E surged to over 85x at end-2024 during its cloud transition but has since moderated to approximately 28–30x by early 2026.

These are not distressed businesses—they generate strong margins and cash flows—but markets have recalibrated growth expectations as capital rotates toward the AI frontier.

ℹ︎

Why AI ‘Pure Plays’ Command Extreme Premia

● A Scarcity premium: only a handful of teams globally can build frontier-scale models, and capital and talent barriers are prohibitive.

● Substantial option value: a small number of foundation models may become indispensable infrastructure for entire industries, creating quasi-utility economics with high switching costs.

✦ Note: for clarity in translation not for publishing: a few big foundation models could become essential building blocks for many industries, acting like utility services. Once established, switching to different models would be difficult and costly, making these models highly valuable and hard to replace.

● Strategic importance: Large cloud providers encourage customers to stay with them by offering services that work best within their system, making it hard to switch to a different provider.

This helps boost their private company values, even before they are legally obliged to release public financial information.

ℹ︎

What Does the Current Multiple Imply?

When the P/E multiple declines despite continued growth, the market is implicitly assuming one of two things:

1) A sharp future slowdown in growth

2) A transition of the company into a lower growth category

✦ The key question for investors is not: Why did the multiple fall?

but rather: Is the implied assumption of slower growth justified by the numbers?

If you want, I can also turn this into a slide ready insight or integrate it into a broader valuation narrative.

ℹ︎

What Should Be Monitored Over the Next 12–24 Months?

1) The share of revenues tied to actual AI-driven initiatives

2) The evolution of operating margins after integrating AI tools

3) Return on invested capital (ROIC)

4) Changes in the nature of contracts (technical implementation vs. repeatable digital products)

✦ These indicators will determine whether the downturn is temporary or reflects a long-term reclassification.

Concluding remarks:

The core analytical takeaway is not whether Saudi tech companies will be affected by the global AI wave, but rather how they will be reclassified within valuation tiers.

The companies under review do not belong to the layer of foundation model developers or global open software players that have captured an exceptional scarcity premium in the current cycle.

Yet, at the same time, they are not facing direct competitive displacement that would justify a deep structural discount in their valuations.

The conclusion is not that Saudi tech firms are experiencing an AI shock, but that the market has reclassified them after a period of overly optimistic pricing.

The current compression in earnings multiples does not reflect a breakdown in the operating model; it reflects a shift from being priced as high growth tech to being viewed as stable tech services businesses supported by domestic digital transformation.

The distinction between these two categories is fundamental for valuation. In the coming phase, AI will not act as a displacement force for these companies, but rather as a benchmark for their ability to enhance margins and improve return on capital.