Analyzing Saudi Arabia’s strategic approach to its substantial investments in the online gaming and e-sports industries necessitates a nuanced understanding of current global industry dynamics and associated risks.

Despite pouring billions of US dollars into fostering a vibrant gaming ecosystem, it’s crucial for policymakers to recognize the deepening dilemma posed by market saturation and the challenges faced by large publishers in achieving profitability in the past few years.

The global video game market has become markedly oversaturated, with nearly impenetrable barriers for new releases.

High development costs on new games do not guarantee commercial success. Reliable data, as we demonstrate in this analysis from Argaam Intelligence, indicate that games with review scores above 90 degrees out of a scale of 100 are among the few that realize substantial profits, while the majority of new titles fail to break even, often getting lost amid countless similar offerings.

On the other hand, instead of viewing charity funds primarily as passive capital pools for social projects or endowments to sustain specific sectors, this approach advocates for deliberate, strategic interventions in broader macroeconomic stabilization efforts especially in helping paying off national debt.

ℹ︎

A saturated market

● The market is overwhelmed with new games ● Many games receive few or no reviews ● High failure and cancelation rates of new games ● Player behaviour stifles growth since players prefer old games Risk: Diminished profitability and growth

This fierce competition implies that even significant investments in innovative titles are increasingly risky, particularly when market access and consumer attention are scarce.

The Saudi Savvy Games Group has invested over SAR 142 billion ( $37.8 billion) across nine major acquisitions since 2022, targeting a SAR 50 billion ($13.3 billion) GDP contribution and 39,000 jobs by 2030.

This capital blitz has positioned Savvy as the 8th largest global games publisher and the world's largest esports company, commanding approximately 40% of the global esports market.

PIF's investment thesis centers on acquiring established market leaders rather than developing unproven Intellectual Property from scratch, like new brands or games in esports, with major acquisitions including Scopely ($4.9 billion, 2023)—the second-highest grossing mobile publisher globally generating over $10 billion in lifetime revenue.

ESL FACEIT Group ($1.5 billion integration) controlling 40% of global esports market share, and strategic stakes including 8.1% in Embracer Group and 30% in Hero Esports, the Asia-Pacific esports leader.

That said, this approach also bears inherent risks—namely, the potential shift in players’ preferences and behavioral trends that could render current assets less relevant in the near future.

Why More Games Might Mean Less Profit for Big Publishers

The market has become flooded with a high number of major releases, even large companies can face diminished returns due to increased competition for players’ attention and consumer spending.

Around 83% of new mobile games fail within three years of launch, while 43% are cancelled during development before ever reaching an audience.

This saturation can lead to reduced sales per title, lower profit margins, and slower growth for the investment portfolio, making it a systemic risk despite the PIF’s ownership of key IP assets.

Another aspect of market saturation centres around the player behaviour. The overwhelming majority of players don't spend much time the new release.

Latest data available shows that only about 6.5% of their total gaming time is spent on new titles. Most players are instead sticking with established, popular franchises they already like.

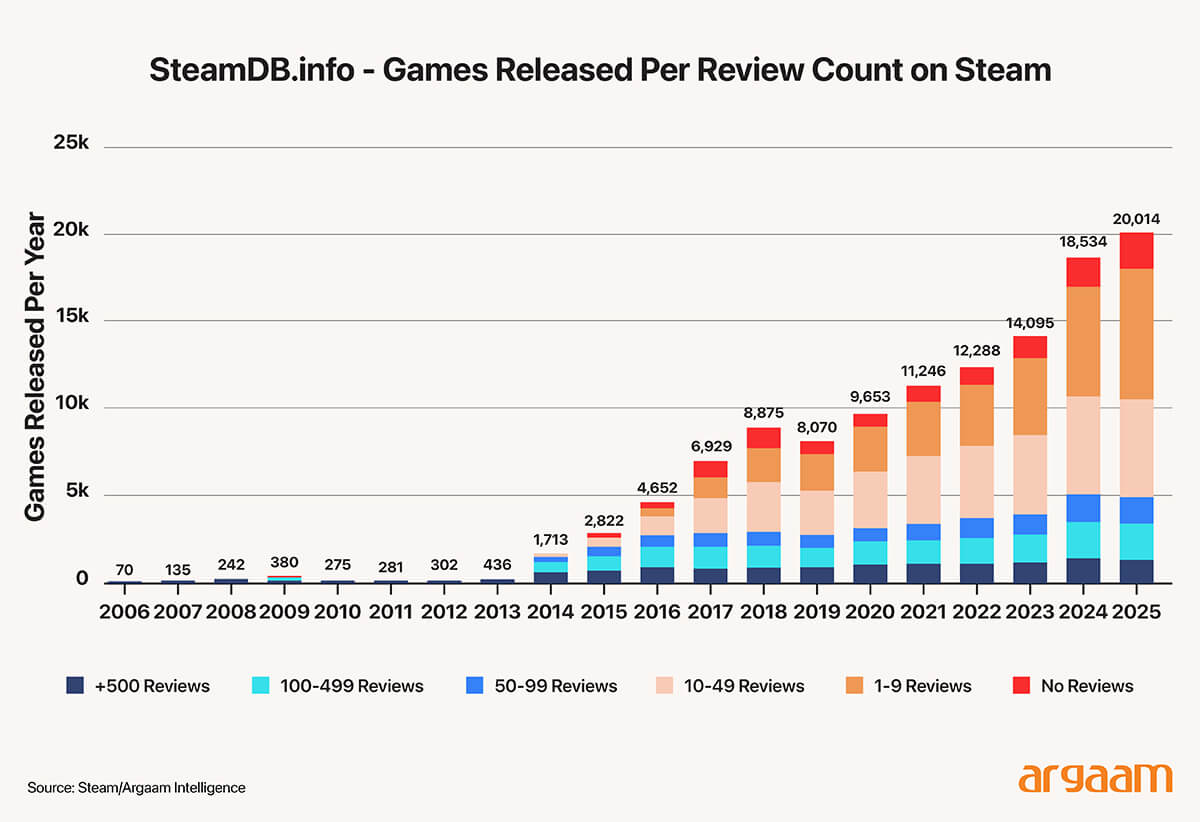

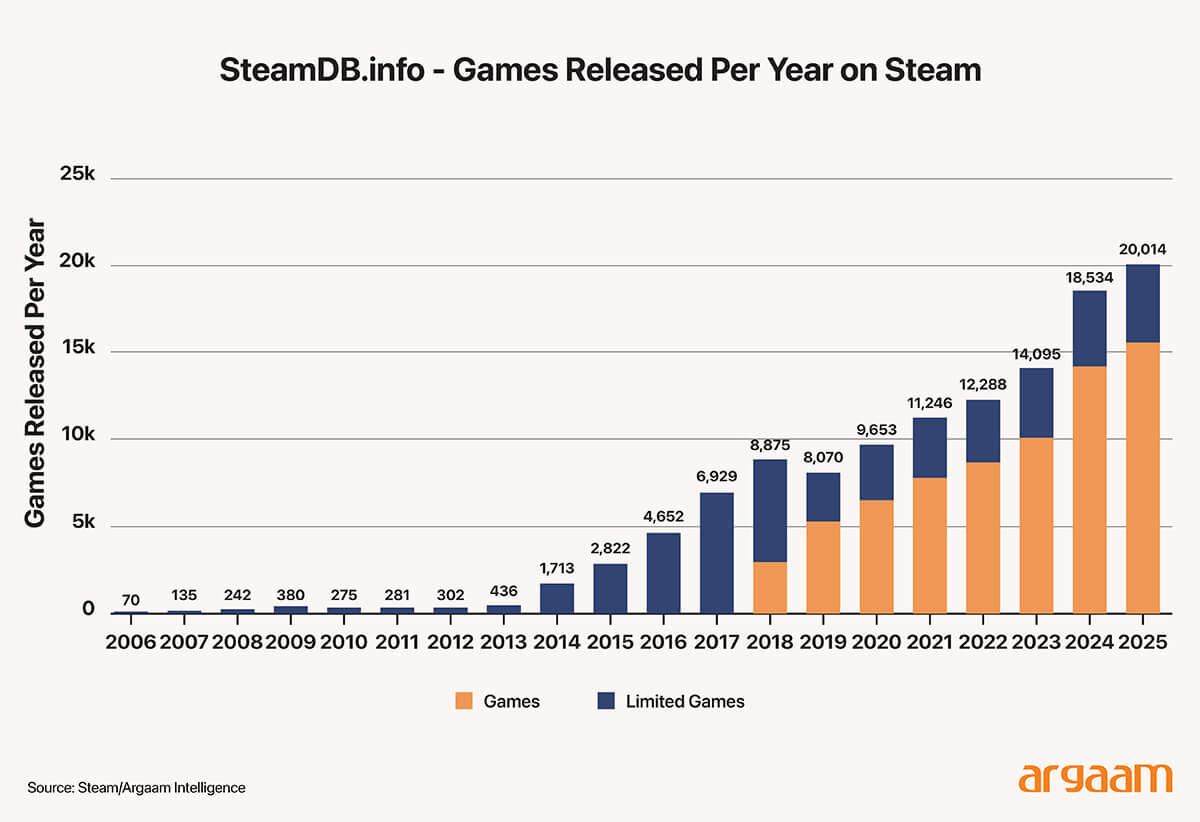

Annual Steam releases surged from 8,070 in 2019 to 20,014 in 2025—a 148%increase representing a 2.48x multiplier of the pre-pandemic baseline.

This avalanche of new games has triggered a severe discoverability crisis, evidenced by approximately 50% of 2025 releases receiving fewer than 10 user reviews, indicating near-zero market penetration for half of all new titles.

Note Limited Games indicate a subset of game releases characterized by limited scope, scale, or accessibility, distinguished from mainstream or large-scale titles.

Note Steam refers to a digital distribution platform developed by Valve Corporation. It is one of the largest online platforms for purchasing, downloading, and playing video games.

Steam provides a marketplace where developers can publish their games, and players can access a vast library of titles across various genres.

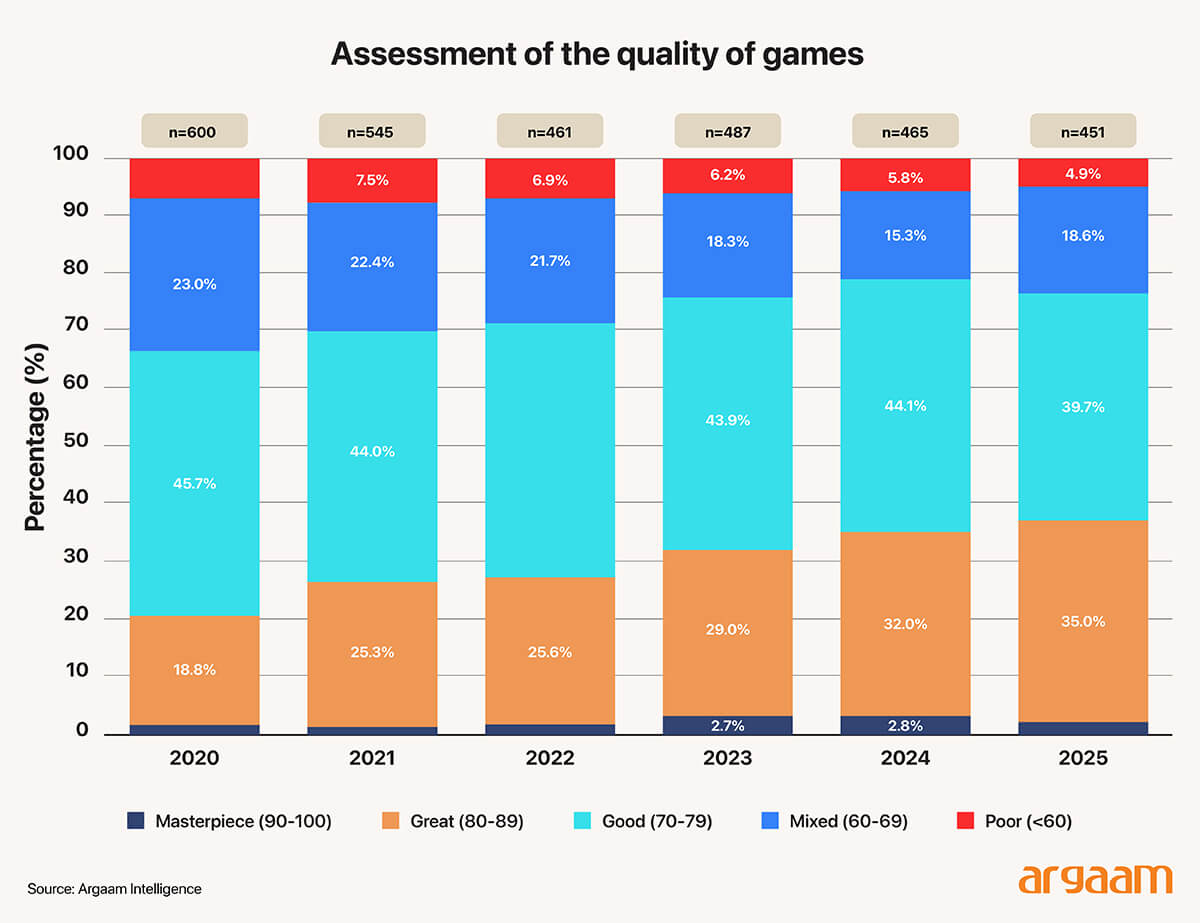

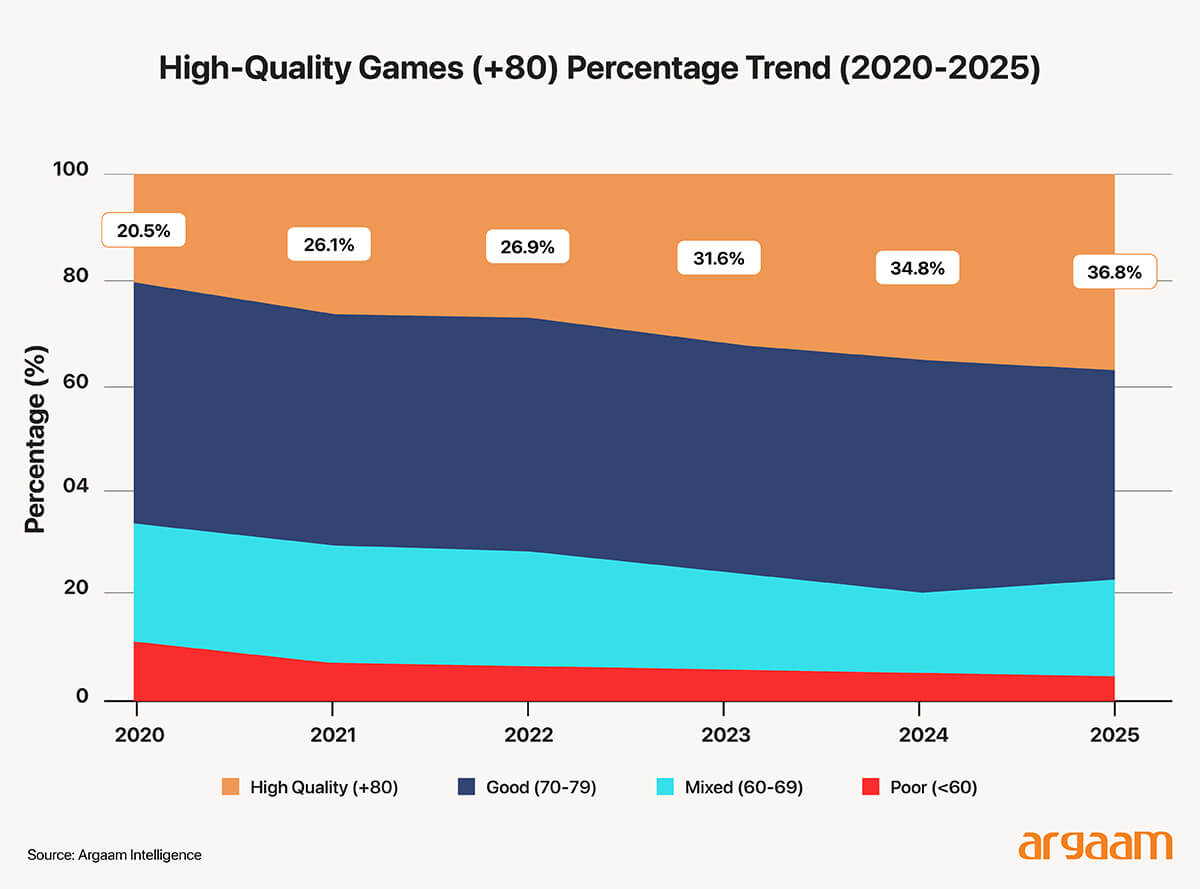

The Paradox of Quality Inflation in the 2025 Gaming Market

In 2025, 166 games achieved Metacritic scores of 80% or higher, representing 36.8% of the 451 titles reviewed—a historical peak for critically acclaimed releases.

Note Metacritic is a review aggregation website that compiles reviews from critics and assigns a weighted average score, known as the Metascore, to movies, TV shows, albums, and video games.

However, this quality inflation has created a commercial paradox: scoring +80% no longer ensures financial viability. The data reveals a stark split within this tier.

The 80-89% "Great" category reached saturation with 158 games (35% of all releases), expanding 40% since 2020, while the +90% "Masterpiece" tier significantly shrank to just 8 games (1.8%)—down from 13 in both 2023 and 2024.

This situation results in a "crowded middle"—many games receive high critical praise but do not necessarily lead to strong sales or player engagement.

French video game company Ubisoft's fiscal struggles exemplify this dilemma.

Despite producing AAA titles with massive budgets, the company reported near break-even operating performance in 2024-25, with total value of sales (after subtracting any cancellations, discounts, or returns) of €1.85 billion falling below targets.

The mismatch between development investment and returns forced Ubisoft to implement a €200 million cost reduction program, including team restructuring and project cancellations.

This pattern shows the industry's main issue: the costs to develop new games have grown a lot, but the money made from sales has stayed the same.

This creates a difficult situation where hitting a certain quality or success level—once a dependable sign of commercial success—now feels like a matter of luck.

With 158 games competing in the "great but not masterpiece" tier and only 8 breaking into the +90% commercial safety zone, investors face a 98.2% probability of missing the level of quality, uniqueness, or standout features that a game must have to distinguish itself from the competition and achieve commercial success.

ℹ︎

Signals: Oversaturation undermines ROI

Shifting focus to revenue from live services and subscriptions

optimizing existing assets over aggressive growth strategies.

Increasing CAC due to heightened competition in oversaturated markets.

Decreasing LTV as player loyalty wanes and preferences shift ● The focus should be on optimizing existing assets for sustainable long-term value rather than just investing in new titles.

Embracing a New Path in a Slow-Grow Industry

The gaming industry experienced explosive growth during the pandemic, achieving 11% annual revenue expansion from 2018-2021, catapulting global revenues from $142 billion to $193 billion.

However, this growth trajectory collapsed dramatically in the post-pandemic correction. The 2024 market generated $187.7 billion with merely 2.1% year-over-year growth, while 2025-2026 projections indicate a persistent deceleration with Newzoo forecasting 2.8% CAGR through 2028—representing a 75% slowdown from pandemic rates. When adjusted for 4.2% projected inflation, the market is essentially flat.

In 2024, the video game industry experienced around 14,800 layoffs.

So this data-driven context demonstrates that investing in a video gaming company should prioritizes stability and steady income over aggressive growth.

It is because traditional growth metrics—the usual ways companies measure success like selling more games—are becoming less reliable as industry growth slows down.

The annual growth rate Compound Annual Growth Rate of the industry has fallen sharply to between 2.1% in late 2024 and 4.4% in 2025, a very low rate compared to previous years of 13% (2016-2021).

Because of this significant decline in the industry growth, companies need to shift their focus from just selling more new games in a highly saturated market to increasing revenue from live services and in-game subscriptions.

This is crucial to be maintained by the Saudi-acquired companies to survive in a low-growth environment. If they cannot sustain this new shift, which they already began, they risk falling behind or failing because their traditional way of measuring success (more game sales) is no longer enough to sustain them.

Concluding thought:

ℹ︎

1.8%

● Only a tiny fraction of new titles (1.8%) achieve top-tier excellence and find way to profitability. ● Substantial investments in new, high-quality games do not guarantee commercial success. ● The minimum level for categorizing a game as high-quality is a score of 80 out of 100.

For Saudi policymakers, a strategic reconsideration of the business model in the online gaming industry should involve analyzing the relationship between Customer Acquisition Cost (CAC) and Lifetime Value (LTV).

In oversaturated markets, CAC tends to increase as companies compete harder for players’ attention. Meanwhile, LTV—reflecting the total revenue expected from a customer over their engagement period—may decrease if players become more selective or less loyal due to market saturation or changing preferences.

Reconsidering this relationship under the new data and circumstances we explained this analysis helps assess whether current investment levels in new titles are financially sustainable or if optimizing existing assets may deliver more stable long-term value.

More this Weekend

Riyadh vs Dubai Real Estate: A Comparative Analysis of Demographic-Driven Investment Risk-Return Profiles

Riyadh and Dubai do represent two fundamentally distinct real estate investment models, differentiated by their demographic compositions and resulting risk-return characteristics. Permanent citizen populations generate predictable, compounding housing demand with lower volatility, while expatriate-dependent populations create higher growth potential coupled with cyclical sensitivity to economic shocks.

Valuation discipline in GCC M&A deals in context of broader market environment

The importance of maintaining valuation discipline in GCC M&A deals is exemplified in two notable transactions that took place in 2025.

In the first transaction, adherence to fundamental valuation principles appears to have limited downside risk and supported a more robust strategic rationale.

Analyzing Overproduction Trends and Their Impact on the Petrochemical Industry

Saudi Arabia's petrochemicals and cement industries are currently exhibiting signs of overcapacity, which may indicate a potential disconnect between supply and demand. In the petrochemicals sector, recent financial performance has transitioned toward substantial losses, reflecting structural challenges related to excess production.