Saudi Arabia's petrochemicals and cement industries are currently exhibiting signs of overcapacity, which may indicate a potential disconnect between supply and demand. In the petrochemicals sector, recent financial performance has transitioned toward substantial losses, reflecting structural challenges related to excess production.

ℹ︎

Not all production surpluses are alike:

● Cyclical surplus: tied to the economic cycle and generally absorbable.

● Structural surplus: capacity that exceeds long term attainable demand.

● External policy driven surplus: resulting from industrial policies in other countries (such as China).

The risk:

Using cyclical tools to address a structural surplus can lead to value destruction.

This situation has been influenced by ongoing global capacity additions that have resulted in oversupply, reduced utilization rates, and increased price pressures in polymer markets.

Similarly, the cement industry is experiencing a period of oversupply, with installed capacity significantly exceeding actual demand. Industry data suggests that utilization rates are expected to remain below optimal levels for an extended period, and high inventory levels—comparable to nearly a year's worth of demand—highlight the need for strategic adjustments.

Currently, average selling prices are below regulatory caps and only slightly above production costs, emphasizing ongoing challenges in balancing supply with market demand.

Petrochemicals: global overcapacity drives margin collapse

Saudi petrochemicals face unprecedented financial stress from global overcapacity that has fundamentally altered competitive dynamics. Notably, China's massive capacity expansions flooding global markets with low-cost output distinguish this from cyclical downturns.

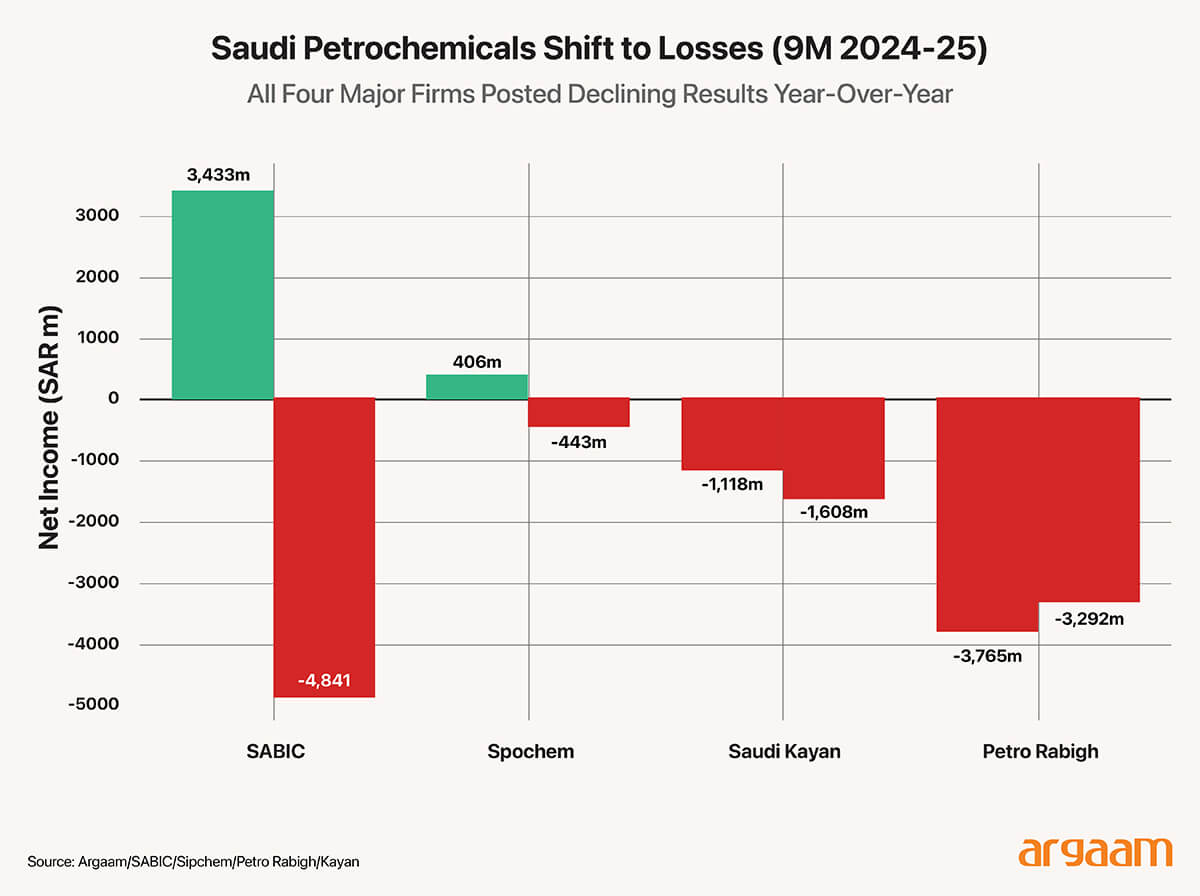

SABIC, which is 70% owned by Saudi Aramco, reported a net loss of SAR 4.84 billion in the first 9 months of 2025, reversing from a profit of SAR 3.43 billion in the first 9 months of 2024. In Q3 2025, revenue fell 7% y/y to SAR 34.33 billion; net income collapsed 56% y/y to SAR 435 million.

SABIC recorded SAR 3.78 billion for closing its Teesside cracker in the UK, SAR 1.07 billion in restructuring costs, and SAR 925 million in European joint venture writedowns.

Sipchem (Sahara International Petrochemical Company) swung from a profit of SAR 406 million in 9M 2024 to a loss of SAR 443 million in 9M 2025, with Q3 2025 posting a loss of SAR 469 million versus a profit of SAR 103 million a year earlier. The company recognized SAR 300 million in asset impairments including SAR 200 million for ethyl acetate plant mothballing.

Further, revenues declined 16% y/y in Q3 2025 as gross income turned negative, driven by lower prices and rising feedstock costs—Saudi Aramco raised ethane prices from $2.50/MMBtu to $3.00/MMBtu in January 2025, a 20% increase eliminating the region's traditional cost advantage.

Petro Rabigh recorded net losses of SAR 3.29 billion in 9M 2025, with accumulated losses reaching SAR 8.57 billion. Saudi Kayan reported losses of SAR 1.61 billion in 9M 2025, with accumulated losses reaching SAR 5.84 billion.

ℹ︎

When does surplus turn into value destruction?

● Production costs converge toward the selling price.

● Feedstock costs exceed total revenues.

● Repeated asset impairments.

● Operating at 75–80% capacity for extended periods.

These are not symptoms of a short cycle, but indicators of a structural breakdown in return on capital.

China's Role in Global Overcapacity

Between 2020 and 2025, global ethylene capacity expanded by more than 40 million tonnes, with approximately 70% of this new capacity—roughly 28 million tonnes—built in China. During the same period, demand grew by approximately 27 million tonnes, creating a fundamental supply-demand imbalance.

China's domestic demand plateaued—no longer growing fast enough to absorb its own output—forcing Chinese companies to export surplus at low prices.

Polypropylene margins collapsed over 95% between 2019-2021 and 2022-2024. Chinese PP plants reduced operating capacity to approximately 75% by 2025, yet production still floods global markets.

Polymer Price Deflation and Plant Closures

Polypropylene prices declined by 3-5% globally through 2025, with North America's sharpest 2025Q2 correction of 10.9% q/q and Europe's 6.9% decline. By June 2025, US PP spot prices reached multi-quarter lows.

Margin pressure forced global producers to permanently close facilities. Beyond SABIC's Teesside closure, Dow idled three European facilities, Eni shuttered its last two Italian steam crackers, and South Korea targeted a 25% domestic capacity cut.

ℹ︎

Stress Test Which scenarios shift the equation?

Test the sector under:

1) A partial Chinese recovery

2) Continuation of China’s current industrial policy

3) Local energy or financing tightening

Then ask:

● Who regains their margins?

● Who remains value negative?

● Who requires an exit or consolidation?

Cement: structural oversupply and the inventory buildup

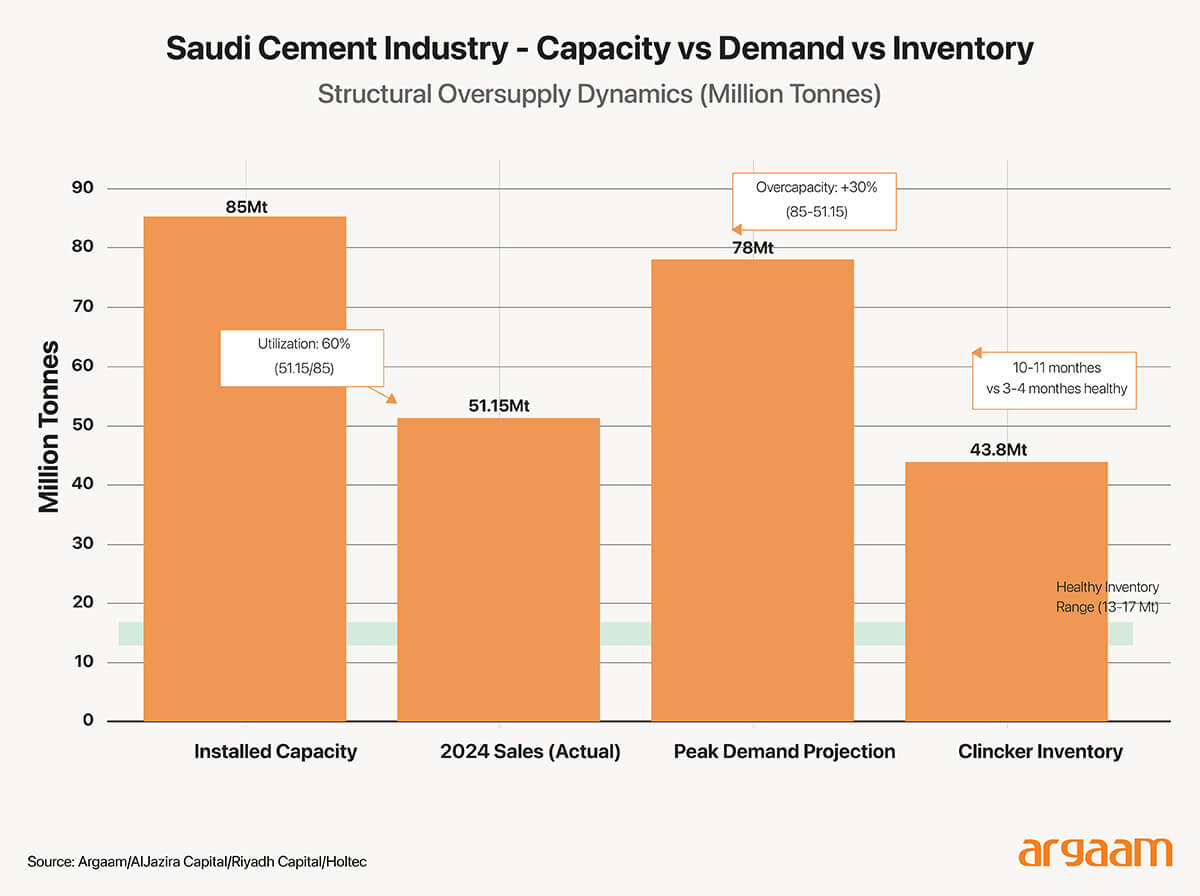

Saudi Arabia's cement industry faces clear overproduction: massive installed capacity, utilization rates stuck in the low-60% range, inventory levels representing nearly a year's supply, and pricing pressure leaving razor-thin margins despite a regulatory cap.

Saudi Arabia maintains 85 million tonnes of installed cement production capacity, while actual sales in 2024 totalled 51.15 million tonnes, creating an overcapacity of approximately 40%.

Capacity utilization in 2024 averaged approximately 60% (rounding off) - well below the 80% threshold necessary for healthy margins and returns on invested capital (ROIC).

By January 2025, Saudi cement companies held 43.8 million tonnes of clinker stock—approximately 10-11 months at current sales rates. Healthy inventory typically ranges 3-4 months.

This buildup—nearly triple healthy levels—reflects intense competition among 17 producers driving high production to capture market share despite weak profitability, stockpiling in anticipation of megaproject demand spikes, and declining export demand trapping surplus production domestically.

ℹ︎

The Single Producer Dilemma

It may seem reasonable for an individual company to increase production to defend its market share. But the collective outcome is a larger surplus, lower prices, and weaker margins for everyone.

This is a classic dilemma that can only be resolved through:

● Consolidation

● Exit

● Regulatory intervention

Pricing Pressure and Margin Compression

Average cement production costs in Saudi Arabia reached SAR 150-160 per tonne in early 2025, driven primarily by fuel cost inflation—Saudi Aramco's fuel price increases including an 8-10% hike in January 2025 significantly impacted producers' cost structures.

Despite rising costs, market prices remain constrained. The Ministry of Commerce effectively caps ex-factory prices at approximately SAR 240 per tonne.

However, intense competition has driven average realized prices to approximately SAR 190 per tonne—substantially below the regulatory cap and only SAR 30-40 above production costs.

Yamama Cement dropped realized prices 10% q/q in Q2 2025 while aggressively pursuing market share, expanding from 12% in 2024 to 17% in August 2025. This pricing competition forced other Central region producers to respond, creating deflationary pressure in the market's highest-growth region

Production Behaviour and Consolidation Pressure

Producers continued high production, despite overcapacity and margin pressures. Clinker production in Q4 2024 increased 7% y/y to 14.89 million tonnes even as inventories soared.

Individual producers maintain output to defend position, yet aggregate production exacerbates overcapacity, inventory buildup, and pricing pressure harming all key players in the industry, individual producers, suppliers, distributors

Compounding the problem, several producers announced or are implementing capacity expansions totalling approximately 12 million tonnes by 2028, bringing total capacity toward 90-100 million tonnes, further depressing utilization rates absent extraordinary demand growth.

Prolonged overcapacity and margin pressure create conditions favouring consolidation. Qassim Cement's acquisition of Hail Cement represents the first major consolidation move, capturing approximately 13% market share in 9M 2024 - becoming the largest producer.

Additional consolidation appears inevitable, given structural overcapacity. Smaller, less efficient producers with limited financial buffers face unsustainable conditions if current dynamics persist for 5-10 years as projected.

Resource misallocation and forward-looking implications

The overproduction and resulting market dynamics in Saudi petrochemicals and cement may reflect opportunities for enhanced resource optimization and strategic adjustment within the sectors.

Tens of billions of dollars in capital have been deployed toward production capacity generating negative returns and sometimes returns lower than the minimum level necessary to cover the costs of production.

In petrochemicals, Saudi Arabia and other Gulf producers invested heavily in crackers and downstream facilities during 2015-2020, anticipating continued strong global demand growth and relying on feedstock cost advantages. Simultaneously, China invested even more extensively in petrochemical capacity expansion.

The result: capital invested in facilities now operating at 75-80% utilization with negative margins as the operating costs or expenses of the facilities exceed their revenues, resulting in losses rather than profits.

Labour and Raw Material Misallocation

Both industries employ thousands of workers producing output that meets non-existent demand or sells below economic cost.

Petrochemical facilities operating at 75-80% capacity maintain workforce levels comparable to facilities running at 90%+ utilization, meaning substantial labour capacity operates below efficient productive levels.

In cement, 17 producers collectively employ labour sufficient to operate at 90%+ utilization if capacity were rationalized.

Petrochemical producers convert ethane, naphtha, and other feedstocks into polymers sold at prices that fail to cover full costs including capital charges.

This represents fundamental resource misallocation: valuable hydrocarbons converted into products sold at losses would be better deployed elsewhere or left in the ground.

Cement producers convert limestone, gypsum, and fuel into products sold barely above cash costs and below full economic costs. Clinker inventories of 43.8 million tonnes represent approximately SAR 6-7 billion in working capital tied up in slow-moving inventory, based on production costs of SAR 150-160 per tonne.

China Parallel and Policy Implications

China's experience demonstrates risks of capacity-driven industrial policy absent validation of demand. Chinese petrochemical capacity expansions driven by import substitution and state-directed investment created overcapacity that depressed global margins.

The Center for International Environmental Law reports that China's polypropylene plants reduced operating capacity to approximately 75% by 2025, well below levels needed for healthy margins.

The difference is that China's overcapacity actively drives global margin compression making even low-cost Saudi production uneconomic—an externality imposed by one country's industrial policy on global competitors.

For petrochemicals, solutions require either global capacity rationalization, Chinese demand recovery absorbing current overcapacity (possible, but uncertain), or Saudi producers exiting unprofitable segments and shifting toward higher-value specialty chemicals where margins remain viable.

For cement, solutions require either dramatic demand acceleration from megaprojects (possible in late 2020s), market consolidation through facility closures, or government intervention facilitating rationalization.

Both industries face multi-year periods of margin pressures and potential further capacity rationalization. Wood Mackenzie projects that the timeline for the petrochemical industry to achieve satisfactory profitability levels will likely extend into the early 2030s - with global polypropylene operating rates at approximately 80%. Cement industry experts project utilization below 80% for the next decade, implying sustained margin pressure and likely consolidation.

●

This analysis: Does not assume that losses are permanent.

●

Does not assume managerial failure.

●

Only tests the logic of capital allocation under a prolonged surplus.

|

Conclusion

In the petrochemicals industry, options are somewhat limited: international coordination among producers is unlikely without collaborative efforts; the recovery of Chinese demand to help absorb excess supply is still uncertain; and maintaining healthy margins will likely require a strategic shift toward specializing in higher-value chemical products.

In the coming years, Saudi producers have the opportunity to adapt successfully by focusing on operational efficiency and strategic consolidation in anticipation of a market recovery. Alternatively, there may be a need for measures to balance capacity, which could involve some adjustments to avoid potential inefficiencies.