Saudi Arabia has the opportunity to redefine the role of its historic or specialized charity funds conceptually and pragmatically.

Through the conceptual framework, we redefine for charity outcomes as ‘assets’ focused on value creation and long-term benefits to society without profit motives.

On the other hand, instead of viewing charity funds primarily as passive capital pools for social projects or endowments to sustain specific sectors, this approach advocates for deliberate, strategic interventions in broader macroeconomic stabilization efforts especially in helping paying off national debt.

The kingdom’s debt reached around SAR 1.4 trillion by the end of 2025, representing around 31.7% of the GDP.

Our strategic rationale is based on the fact that the total volume of Saudi Arabia’s charity and endowment assets is estimated to be more than SAR 430 billion.

Endowment assets alone amount to SAR 1.7 billion as of 2024, with an average annual growth rate of 65% over the past five years.

The total contributions from various sectors—such as charities, endowments, volunteering, and cooperative societies—reach a combined economic contribution exceeding SAR 100 billion.

Reframing Nonprofit Funding Through Lifetime Economic Benefits

A nonprofit running job training programs in Riyadh, for example, usually gets funding based on how many people they train or certificates they give.

But if we can measure how much the program increases people’s earning ability and assign a riyal value to that, funders can see the real benefit. So, for every riyal spent might help someone earn enough extra wages over their lifetime to be worth three riyals.

This mean that the additional wages or benefits someone gains from the charity program are valued at three times the original amount spent or invested. This actually makes the one riyal spent effectively worth three riyals in benefits over time.

By valuing these social benefits like assets, funders can then better decide which programs give the most value for their money, ensuring resources go to the most effective uses.

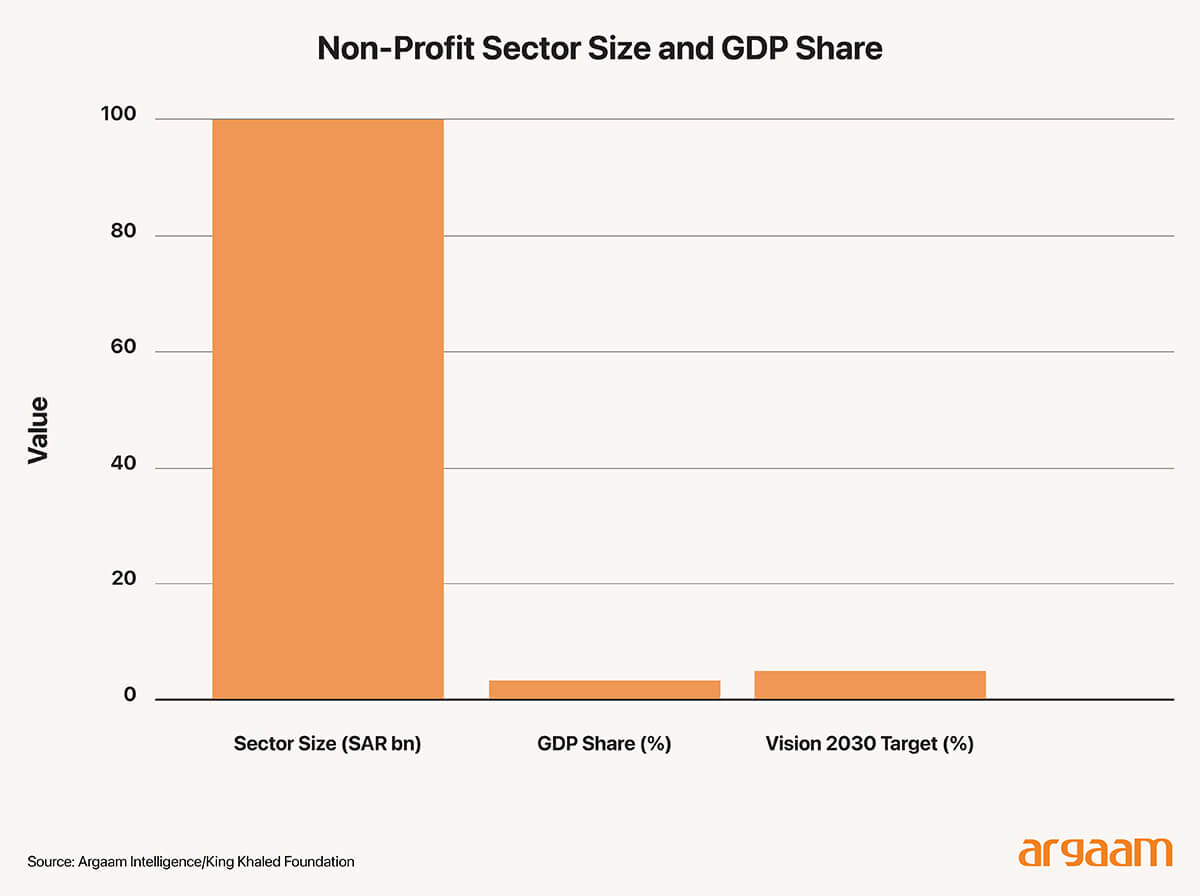

The non-profit sector has surpassed SAR 100 billion for the first time, accounting for 3.3% of GDP, and is expected to meet the Saudi Vision 2030 target of 5% of GDP two years ahead of schedule.

Education and research organizations ranked first in revenue (over SAR 19 billion), while health organizations topped expenses (SAR 15 billion), driven by the transfer of government assets.

Digital donation platforms raised over SAR 15 billion in 2024, with small donations (SAR 1, 10, 100) accounting for the largest contribution, while donors of high value (over SAR 100K) made up 26% of donations.

Business-Style Incentives

Many nonprofits operate under traditional funding models characterized by input-based metrics—e.g., number of beneficiaries served, number of programs implemented, or discrete outputs, rather than holistic impact measures.

These models, while useful, often lack alignment of incentives with long-term value creation, and can suffer from issues like adverse selection.

The real question is whether using money and reward systems similar to those in business —based on results—can help improve how charities are run and how accountable they are, without hurting their ethical values or long-term goals.

So, charities, we argue, could involve giving donors or investors some kind of financial incentive or reward based on the results or outcomes that charities achieve, much like how companies earn profits or investors get returns based on performance.

Who’s Really Being Marketised

Marketisation begins only when these measured outcomes start to play a more active role in decision-making—when they are compared across programmes, embedded into funding contracts, or used to guide how capital is allocated.

In this sense, financialisation refers less to monetisation and more to valuation: the use of financial logic to rank, assess, and prioritise social results.

Importantly, treating outcomes as assets does not imply that they must generate profits. Outcomes resemble assets because they are forward-looking, uncertain, and capable of producing long-term social or fiscal value, not because they deliver distributable financial returns.

Financial reasoning enters as a discipline—introducing comparability, risk awareness, and accountability—rather than as an end in itself.

This distinction matters for policy design. Conflating outcome valuation with profit maximisation risks oversimplifying the debate. The real question is not whether charities should become market actors, but how far market-based tools should shape charitable governance, and where clear institutional limits should be drawn.

Under such conditions, taxation alone struggles to function as an effective economic deterrent, pointing to the need for complementary financial and structural policy measures.

Dimension

Traditional Charity Measurment

Outcome-Based / Marketised Measurement

Primary focus

Inputs and activities

Verified outcoms and results

Success definition

Funds spend as intended

Outcomes achieved against targets

Key metrics

Beneficiaries served, programme reach

Cost per outcome, outcome achievement rate

Time horizon

Annual / short-term reporting

Medium - to long-term outcome cycles

Accountability

Donors and trustees

Policymarkers, funders, and captial providers

Risk treatment

Operational risk borne by charity

Execution risk partially shifted to funders/investors

Role of financial data

Transparency and stewardship

Efficiency benchmarking and risk calibration

Financial performance operates as a benchmark—a discipline used to assess efficiency, risk, and sustainability—rather than as an objective in its own right.

Research on nonprofit performance measurement shows that charities are increasingly expected to demonstrate not only what they do, but how efficiently they do it.

Actually, the combined use of financial and non-financial performance indicators is positively associated with organisational effectiveness, suggesting that financial metrics play a meaningful role in guiding decision-making and accountability, even when profit is not the goal.

In practice, this has translated into growing attention to measures such as cost per outcome, overhead ratios, and resource allocation efficiency across large nonprofit organisations.

Financial benchmarks also serve as a calibration tool for risk. Outcome-based arrangements often shift execution risk away from governments or donors and toward external funders.

Financial analysis helps assess whether this risk is being priced realistically, and whether expectations—explicit or implicit—around repayment or compensation are aligned with the underlying uncertainty of social outcomes.

Financial Logic as the Anchor of Institutional Resilience

Financial performance functions as a stress test for institutional sustainability. Outcome verification, data systems, and contractual governance introduce real administrative costs.

Sector guidance consistently notes that without basic financial discipline, even well-designed impact frameworks can become difficult to sustain.

Viewed in this way, financial logic does not redefine success in commercial terms; it constrains excess, clarifies trade-offs, and supports more disciplined governance in outcome-focused charitable systems.

But what conventional financial statements typically do not reveal is whether spending is translating into comparable, verifiable outcomes across programmes. This is where outcome-based marketisation can add value—if designed carefully.

Using audited accounts and annual reports as a baseline, policymakers could require a sharper link between programme costs and outcome units (e.g., cost per successful placement, cost per sustained beneficiary outcome), enabling comparisons across interventions rather than across budgets.

The Challenge of Measuring Social Change

Outcome-based funding, which allocates resources based on measurable results, can unintentionally change how organizations plan and spend their money. It usually favors projects that can show quick, clear, and easy-to-verify results.

But many important social changes—like improving people's skills, promoting social inclusion, or changing behaviors—take a long time and don’t follow straightforward paths.

This means that if funding is mainly based on short-term results, organizations might focus only on projects that produce fast results, even if those projects don’t bring about the most meaningful long-term change.

Why is this important financially? Because it can lead to a lot of money being spent on smaller, quick wins instead of bigger, more impactful efforts that need time to develop.

In the long run, this might limit the kind of social progress that can be achieved, and resources might not flow to the projects that could truly make a difference over many years.

If a charity is funded based only on quick results, like the number of people served in a month, it might skip important but slower projects, such as building new schools or training programs that need years to show results.

For example, a charity helping families get jobs might focus only on how many people find work within three months to get funding, instead of supporting long-term job training programs that improve communities over years.

Concluding thought:

Despite its substantial growth and importance in social development, the non-profit sector is often viewed as a complementary rather than a core driver of macroeconomic policies and overall economic stability.

Its focus tends to be on social services, philanthropy, and community support, which typically do not influence economic policy, at the scale of main economic sectors in the kingdom.

Consequently, its role in shaping macroeconomic policies remains limited, even as its social and economic contributions continue to grow.

More this Weekend

Riyadh vs Dubai Real Estate: A Comparative Analysis of Demographic-Driven Investment Risk-Return Profiles

Riyadh and Dubai do represent two fundamentally distinct real estate investment models, differentiated by their demographic compositions and resulting risk-return characteristics. Permanent citizen populations generate predictable, compounding housing demand with lower volatility, while expatriate-dependent populations create higher growth potential coupled with cyclical sensitivity to economic shocks.

Valuation discipline in GCC M&A deals in context of broader market environment

The importance of maintaining valuation discipline in GCC M&A deals is exemplified in two notable transactions that took place in 2025.

In the first transaction, adherence to fundamental valuation principles appears to have limited downside risk and supported a more robust strategic rationale.

Analyzing Overproduction Trends and Their Impact on the Petrochemical Industry

Saudi Arabia's petrochemicals and cement industries are currently exhibiting signs of overcapacity, which may indicate a potential disconnect between supply and demand. In the petrochemicals sector, recent financial performance has transitioned toward substantial losses, reflecting structural challenges related to excess production.