Despite one of the highest tobacco tax burdens globally, Saudi Arabia continues to observe sustained profitability among multinational tobacco companies. This apparent policy paradox raises a critical question: why has aggressive taxation failed to function as an effective deterrent to tobacco profitability?

The effectiveness of tobacco control in Saudi Arabia now depends less on further increases in headline tax rates and more on the design of economic and financial instruments that directly constrain pricing strategies, entry-level affordability, and profit migration toward alternative nicotine products.

By examining Saudi Arabia’s current tax framework, corporate financial behaviour, and international policy experiences, this analysis outlines policy options better suited to the Kingdom’s institutional and market environment.

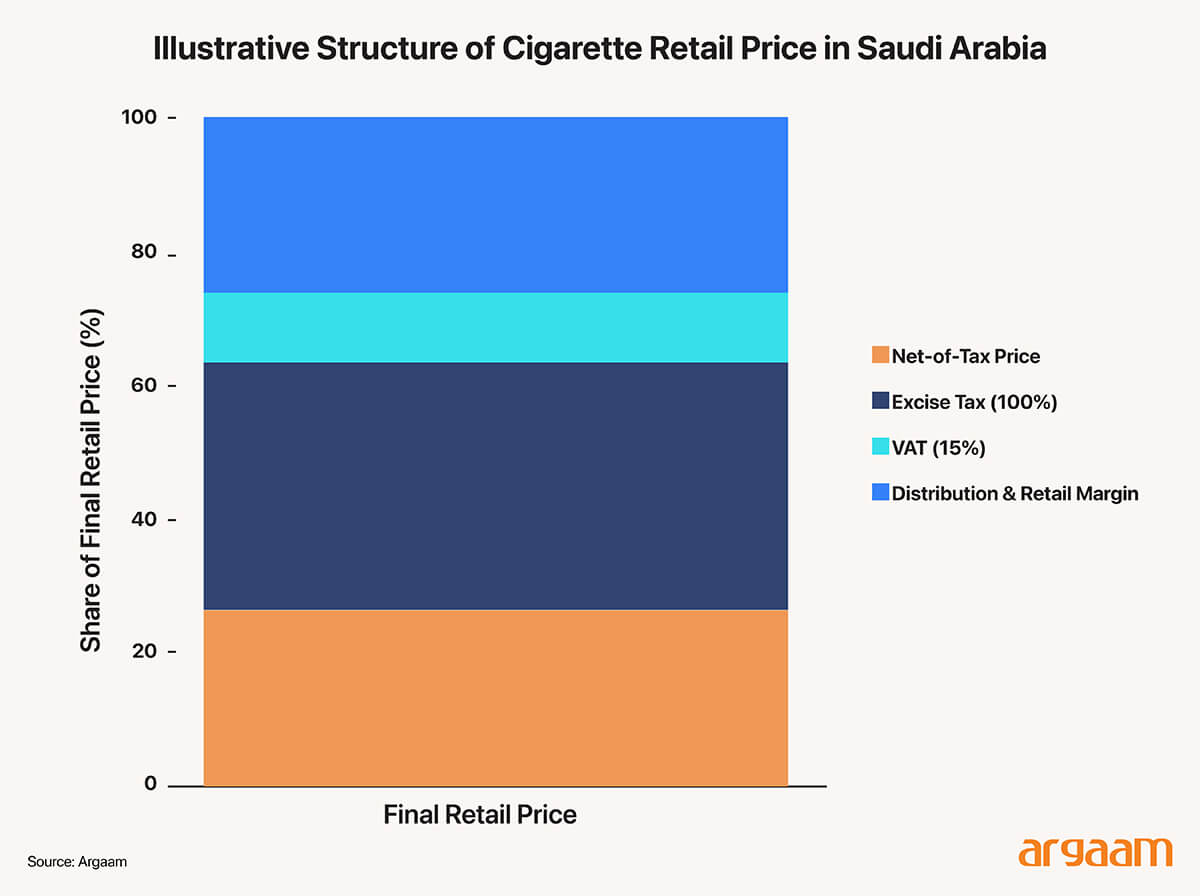

Saudi Arabia has implemented one of the most aggressive tobacco taxation regimes in the region, combining high statutory rates with broad product coverage. Since 2017, tobacco products have been subject to a 100% selective excise tax,(ZATCA,2019) levied at the production or import stage, effectively doubling the pre-tax price of cigarettes and other tobacco products.

In addition, a 15% value-added tax (VAT) is applied to the final retail price,(ZATCA,2020) including the excise component. As a result, taxation in Saudi Arabia operates through a cascading structure, where

VAT is charged on top of excise duties.

This framework produces a very high effective tax burden at the retail level. According to latest available data from World Health Organization, the combined share of excise tax and VAT accounts for over 70% of the final retail price of the most-sold cigarette brand, placing Saudi Arabia among the highest-tax jurisdictions globally. (WHO,2024)

Importantly, the tax base extends beyond traditional combustible cigarettes to include other tobacco products and, more recently, electronic nicotine delivery systems, reflecting an effort to prevent simple substitution across product categories.

🔦

The Hidden Math of Tobacco Costs

From a headline perspective, Saudi Arabia’s tobacco taxation is therefore neither weak nor incomplete. But the structure relies predominantly on ad valorem taxation (Ad valorem rates are a way of charging taxes based on the value or price of something. This type of tax scales with the price of the item rather than being a fixed amount.), without a binding minimum excise or retail price floor.

This design leaves room for price dispersion across brands and segments, allowing firms to absorb tax increases on low-priced products while over shifting taxes on premium offerings. As the next sections show, this structural feature plays a central role in limiting the profit-deterrent effect of high taxation.

High tobacco taxes do not automatically undermine corporate profitability. In markets where demand is addictive and relatively insensitive to price changes, tax increases are often passed on to consumers with limited impact on overall sales volumes. A large body of economic academic research shows that tobacco excise taxes tend to be shifted forward into retail prices, meaning that firms can preserve their underlying profit base even as headline prices rise (University of Illinois at Chicago, 2019).

One of the most important strategies used by multinational tobacco companies is price segmentation. Firms typically operate multi-tier product portfolios, ranging from premium international brands to low-priced entry-level cigarettes.

When taxes increase, prices of premium brands are frequently raised by more than the tax increase itself—a practice widely documented as tax over shifting—allowing companies to maintain or expand margins at the top end of the market (NIH, 2013).

At the same time, producers may absorb part of the tax burden on cheaper brands to keep entry prices low and accessible to price-sensitive consumers, including young and low-income smokers. This asymmetric pricing response enables firms to protect aggregate net revenues while sustaining consumption across different income segments.(University of Bath,2021)

Tax Shifts Turn Demand Gaming into Profit Reallocation

Taxation can also be neutralized through product substitution. As traditional cigarettes become more expensive, tobacco companies increasingly promote alternative nicotine products such as electronic cigarettes, heated tobacco products, or oral nicotine.

When these substitutes face lower or differently structured taxes, profitability is not eliminated but instead reallocated across product categories. Empirical studies suggest that, without coordinated taxation across combustible and non-combustible products, high cigarette taxes may simply redirect demand and profits rather than reduce them.

These dynamics help explain why countries with very high tobacco taxes—including Saudi Arabia—can still observe sustained corporate profitability. When tax systems rely primarily on ad valorem rates without minimum price floors or aligned treatment of substitutes, firms retain considerable flexibility to manage prices and protect margins.

Under such conditions, taxation alone struggles to function as an effective economic deterrent, pointing to the need for complementary financial and structural policy measures.

Despite Steep Tax Hikes, Tobacco Giants See Revenue Rise

The financial reports of multinational tobacco giants also provide strong evidence as to why the current tax system has not been as effective as expected in curbing tobacco consumption.

In 2024 annual financial report (the latest data available), Philip Morris International reported net revenues of $37.9 billion. Excluding excise taxes and VAT, up nearly 8% year-over-year in spite of continued tax increases in many jurisdictions.

The net revenue growth is attributed to higher prices over and above tax increases. Furthermore, smoke-free products accounted for about 39% of net revenues, underscoring how product substitution can offset tax pressure on

traditional cigarettes