Saudi Arabia's 2021 short selling extension fundamentally transformed ETF pricing efficiency. Premiums-discounts that spanned up to 38 percentage points are now contained within 1–3%, arbitrage works faster, and investor confidence—measured by a tenfold AUM surge—has rebounded decisively.

The reform worked because it removed the main bottleneck: before 2021, retail investors couldn't short-sell, so mispricings went uncorrected for days.

While the system has worked well so far, it has also revealed some problems that limit future improvement. These include weak rules for market makers, unclear networks of authorized participants (APs), and divided markets with limited liquidity. These issues can be fixed, but it will require careful and planned action.

The Capital Market Authority now has an important decision to make: either build on their progress by finishing their infrastructure plans or risk slowing down because market liquidity stops growing.

Our analysis offers policymakers clear solutions to move forward. We suggest specific steps to improve regulations, increase transparency, and strengthen the market infrastructure.

The Pre-Reform Baseline: A Market Plagued by Severe Mispricing (2015–2019)

Saudi Arabia's March 2021 extension of short selling to all eligible investors fundamentally transformed the Kingdom's ETF market, eliminating severe pricing inefficiencies through activated arbitrage mechanisms.

Before the reform, the difference between the ETF's market price and its actual value (known as premium-to-Net Asset Value volatility) was extremely large and unpredictable.

In the Falcom 30 fund it was swinging wildly from a huge discount of 12.60% (−1,260 basis points) to a big premium of 7.19% (+719 basis points). This means the ETF's price often wildly strayed from its true value, making it very risky and unpredictable.

Before the reforms, it took a very long time—more than three days—for ETF prices to adjust and match their true value, with the correction happening very slowly.

However, after the reforms, the use of advanced computer algorithms that take advantage of small price differences now make up about 40% of daily trading activity, helping prices adjust faster and reducing the amount of time mispricings last.

Falcom 30 ETF exhibited a +101 bps average premium with an extremely worrying range of -1,260 to +719 bps—a 19.79 percentage point band.

The error correction coefficient of -0.12 indicated extremely sluggish arbitrage, with deviations persisting for at least three trading days.

HSBC 20 ETF exhibited extreme volatility, swinging from -2,283 to +1,592 bps (a 38.75 percentage point range). Its error correction coefficient of -0.05 was the slowest documented, signaling that institutional investors faced execution risk of 10–20% relative to underlying securities when purchasing or redeeming shares.

In contrast, iShares MSCI Saudi Arabia ETF (NYSE-listed) did exhibit a mere +16 bps average premium with a narrower -684 to +382 bps range and a -0.22 error correction coefficient—which was nearly four times faster than HSBC 20.

The greater efficiency reflected US market infrastructure: liquid secondary markets, multiple authorized participants, and—crucially—short selling availability.

The extensive research concluded that the restrictions on short selling, the concentration of authorized market participants, the increased cost for the creation and redemption of the ETF shares, and the lack of an active secondary market at that period created major limits to arbitrage.

With only three documented APs and retail investors barred from short selling, arbitrage capital was insufficient to correct mispricings.

The 2021 Regulatory Watershed: Unlocking Arbitrage Through Short Selling

On March 25, 2021, Saudi regulators allowed all eligible investors, including regular individual investors (retail investors), to engage in short selling. Before that, only certain large or professional investors could do this, while regular investors were barred.

This change means that now everyone who qualifies can participate in short selling, which is a way to make bets that a stock’s price will go down, helping improve market activity and liquidity.

Under the new reforms, individual investors can only hold short positions for up to 10 days' worth of the stock's usual trading volume, and the total amount of short selling across all investors can't be more than 10% of the company's available shares that are free to trade.

Without the ability to sell stocks you don’t own (short selling), the process that keeps ETF prices in line with their true values doesn’t work properly. As a result, when ETF shares trade at a lower price than their actual value (a discount), this difference isn't corrected and can remain for longer.

The reforms helped ensure that ETF prices accurately reflect the value of the underlying assets. When the arbitrage mechanism functions properly, any significant price deviations—such as discounts or premiums—are quickly corrected through trading activity, keeping the ETF price aligned with its actual worth.

This maintains market efficiency, reduces mispricing risks, and provides investors with reliable and fair prices for buying or selling ETF shares.

The reforms also enhanced the CMA disclosure requirements (effective April-May 2021) mandated daily NAV and portfolio holdings publication, facilitating real-time arbitrage calculations alongside the market's existing T+2 settlement infrastructure (implemented April 2017)

Current State Analysis: Dramatic Improvement in Pricing Efficiency (2024–2025)

As of January 2026, the transformation is actually empirically undeniable. Yaqeen 30 ETF (9400), Falcom 30's successor, trades at -2.1% to NAV (SAR 47.31), with AUM of SAR 38.87 million—a dramatic compression from pre-reform +101 bps average and -1,260 to +719 bps volatility.

SAB Invest MSCI Tadawul 30 ETF (9402) trades at +1.4% to NAV (SAR 43.86), with AUM of SAR 22.81 million (as of January 2026), eliminating pre-reform extremes of -2,283 to +1,592 bps.

Albilad MSCI Saudi Growth ETF (9408), launched 2024, trades at +0.8% to NAV (SAR 8.65), demonstrating post-reform structures support efficient pricing for new products. iShares MSCI Saudi Arabia ETF (KSA) now trades at 0.02% premium—NAV parity—with $754.65 million AUM and 3.48% dividend yield.

Saudi ETF pricing efficiency has improved dramatically post-2021 reform, with premium/discount volatility collapsing from extreme ranges to narrow, stable deviations consistent with active arbitrage.

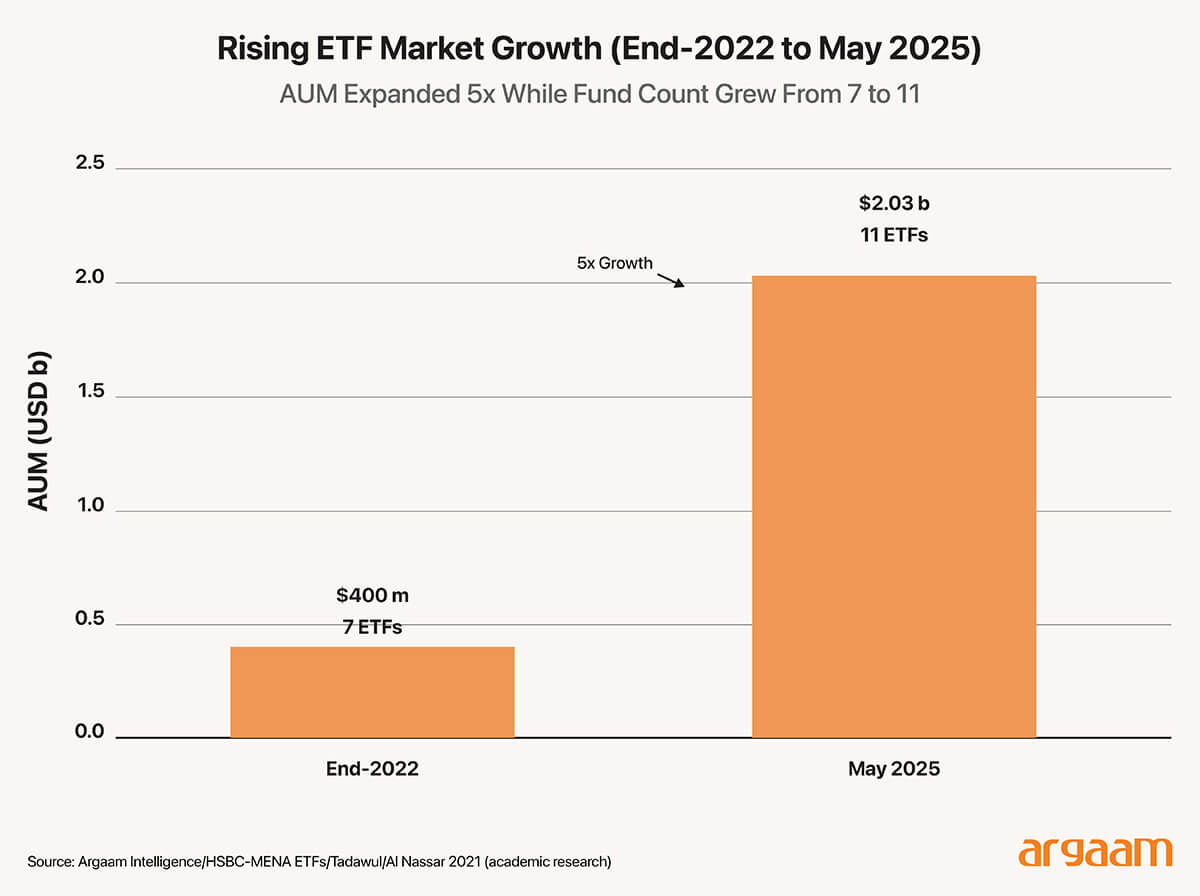

ETF AUM surged from SAR 644.77 million (2023) to SAR 6.69 billion (2024)—a tenfold growth. Industry reports document approx. $400 million (end-2022) rising to $2.03 billion (May 2025). Three new ETFs launched in 2024, expanding the total to 11 funds.

Saudi ETF market experienced explosive growth post-reform, with AUM surging from $400 million (end-2022) to over $2 billion (May 2025) and the number of listed funds expanding from 7 to 11.

The trading value increased by 39.7% y/y, international investors contribute 25% of daily liquidity, and algorithmic traders account for 40% of activity—signaling market maturation.

However, it should be noted that liquidity fragmentation persists. While the largest ETFs (Yaqeen 30, SAB Invest) maintain stable pricing, smaller funds struggle with liquidity: Yaqeen ESG ETF (9409) recorded only 66 shares traded on certain days with negligible AUM, indicating micro-level structural constraints remain despite macro pricing efficiency improvements.

What Succeeded, What remains a challenge, and Why: A Comparative Assessment

1) What Succeeded: Pricing Efficiency and Arbitrage Velocity

The reform achieved its primary objective: eliminating severe ETF mispricings. Pre-reform, price-NAV deviations exceeded 20% in extremes; post-reform, deviations stay within 1–3% even during market stress.

This compression reflects how short selling unlocked arbitrage: traders can now profitably exploit smaller mispricings, which tightens bid-ask spreads and shortens how long deviations persist.

The extreme volatility in Saudi ETF premium/discount ranges documented pre-reform (spanning 38.75 percentage points for HSBC 20) has collapsed to narrow bands of 1-3%, demonstrating the effectiveness of short selling in enabling arbitrage

Error correction speeds—though have not yet been subject to formal econometric analysis—are implied to have accelerated dramatically. Pre-reform persistence of +3 days is inconsistent with current behaviour, where premiums-discounts fluctuate daily. Algorithmic traders (40% of daily liquidity) exploit arbitrage within seconds, not days.

2) What Partially Succeeded: Liquidity Depth and Market Maker Development

Liquidity remains unevenly distributed. The largest ETFs command bulk trading activity; thematic funds struggle. The root cause is structural: market maker regulations remain incomplete.

The September 2025 draft amendments propose mandatory agreements and performance incentives, however, as of January 2026, regulations are not finalized—leaving frameworks underdeveloped relative to US markets where designated market makers provide continuous two-sided quotes.

Shortcomings that need to be addressed: Transparency and Authorized Participant Disclosure

The most glaring deficiency is the absence of AP network disclosure. Pre-reform, only three APs were documented; post-reform, no public data exists on AP count, identity, or activity.

This opacity does contradicts international best practices where AP lists appear in prospectuses. Importantly, Institutional investors cannot assess whether sufficient arbitrage capital exists during stress periods, and there’s no data to evaluate AP ecosystem expansion.

Similarly, creation-redemption volumes are undisclosed, preventing arbitrage mechanism analysis. In mature markets, this data signals real-time arbitrage activity; its absence is a significant transparency gap.

Sources of Financial and Economic Pressure

Macroeconomic headwinds constrained ETF performance despite microstructural improvements. Saudi equity markets gained just 0.6% in calendar 2024—which is substantially below the historical average and reflecting constrained investor sentiment from lower oil prices and fiscal consolidation.

iShares MSCI Saudi Arabia returned +0.54% in calendar 2024, underperforming its benchmark by 75 bps due to sector allocation effects and tracking inefficiencies. Trade surplus contracted 36% y/y from $113.1 billion (2023) to $72.5 billion(2024) on lower hydrocarbon revenues, dampening retail investor enthusiasm in spite of improved pricing efficiency.

Signals to Policymakers: Completing the Unfinished Agenda

The CMA has achieved landmark success with the 2021 reform. Sustaining progress requires completing the structural agenda:

First, Market makers provide continuous liquidity for new ETF launches and prevent smaller fund liquidity traps. Performance-based incentives—reduced trading fees, rebates for meeting bid-ask targets—should be codified.

Second, Transparency enhances investor confidence and enables empirical evaluation of ecosystem expansion. Further, encouraging foreign broker-dealer entrants with global arbitrage capabilities will deepen liquidity.

Third, Fund managers should disclose daily or weekly creation-redemption unit volumes, providing real-time arbitrage dynamics insight and allowing investors to assess mechanism functionality.

Fourth,Reduce creation-redemption costs. Industry analysis indicates that differing creation-redemption protocols across regional markets force issuers to run bespoke processes, inflating costs and widening price-NAV deviations. Streamlining via standardized agreements and electronic basket delivery will lower arbitrage barriers and improve pricing efficiency.

Fifth, Retail investors often lack NAV-based pricing understanding. Public campaigns via Tadawul Academy and licensed brokers will improve arbitrage participation and lower behavioural mispricings.

More this Weekend

Analyzing the EU’s Carbon Tariffs and Their Impact on Saudi Metal Exports

The European Union's Carbon Border Adjustment Mechanism (CBAM), entering full implementation on January 1, 2026, imposes carbon levies on imports of iron, steel, and aluminum that do fundamentally alter Saudi Arabia's €475 million ($515 million) annual metals trade with the block.

Understanding the Interplay between Tobacco Tax Policies and Firm Strategies in Saudi Arabia

Despite one of the highest tobacco tax burdens globally, Saudi Arabia continues to observe sustained profitability among multinational tobacco companies. This apparent policy paradox raises a critical question: why has aggressive taxation failed to function as an effective deterrent to tobacco profitability?