|

The European Union's Carbon Border Adjustment Mechanism (CBAM), entering full implementation on January 1, 2026, imposes carbon levies on imports of iron, steel, and aluminum that do fundamentally alter Saudi Arabia's €475 million ($515 million) annual metals trade with the block.

CBAM's definitive phase requires EU importers to purchase carbon certificates matching embedded emissions of covered goods at prices linked to EU Emissions Trading System (ETS) allowances.

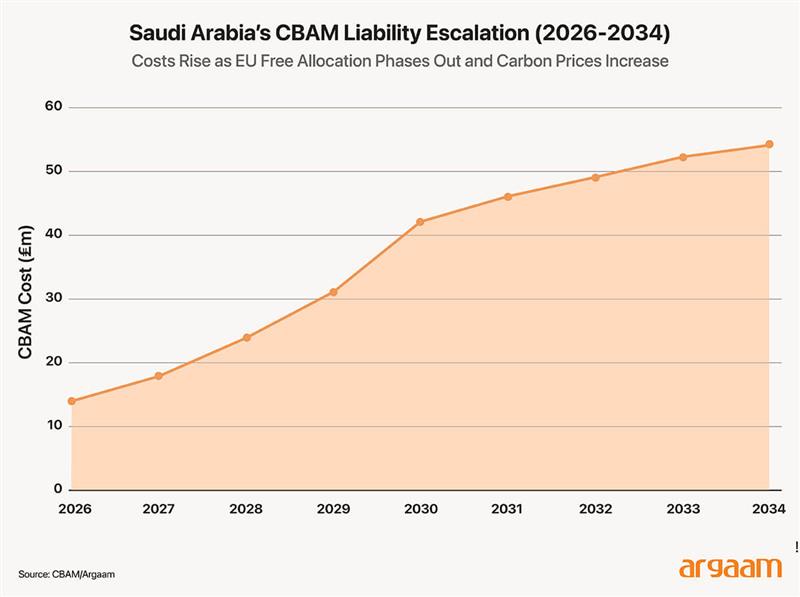

As of December 2025, certificates traded at €83.90 per tonne CO₂, with projections reaching €130 by 2030 and €180 by 2040. The finalized benchmarks—1.423 tCO₂/tonne for primary aluminum and 1.033 tCO₂/tonne for DRI-EAF steel—do create penalty structures that disproportionately impact producers exceeding EU performance standards - even when their absolute emissions remain globally competitive.

Saudi Production Advantage: The Competitiveness Paradox

Note: BF-BOF stands for Blast Furnace-Basic Oxygen Furnace, which is the traditional and most common method used in steelmaking.

This reveals the mechanism's design bias: benchmarks reward relative performance within European conditions rather than absolute global emissions reductions. Saudi steel avoiding 0.67 tonnes CO₂ versus the global average pays CBAM penalties, while European mills at 1.03 tCO₂/tonne receive free allocation, despite both of them utilizing fossil-based energy.  The Pre-CBAM export economics for Saudi steel and aluminum reflected 8-12% margins on international sales. Post-CBAM fundamentally does alters this calculus. For Saudi steel exporters with 1.65 tCO₂/tonne intensity shipping 50,000 tonnes annually to Germany, the 2026 liabilities start at €129,000 but escalate to €2.0 million in 2030 and €4.5 million in 2034. And, Per-tonne, the carbon levy grows from €2.58 in 2026 to €40 in 2030 and €90 in 2034, eroding the $20-70/tonne margin cushion until European sales become unprofitable. Having stated the above, Saudi Arabia faces three strategic pathways to address EU carbon requirements: ● The first pathway is incremental optimization: investing $50-100 million per facility in process efficiency improvements to reduce emissions by 10-15%, and lowering carbon intensity from 1.65 to 1.40-1.49 tCO₂/tonne with 5-7 year payback periods. This approach reduces but does not eliminate CBAM costs. ● The second pathway is full green hydrogen transition: replacing natural gas with electrolytic hydrogen to achieve 0.3-0.5 tCO₂/tonne intensities, which eliminates CBAM liabilities entirely. But this requires $2-3 billion capital investment per facility, and at hydrogen production costs of $3-5/kg with consumption of 55-60 kg per tonne DRI, operating expenses increase by $165-300/tonne compared to gas-based routes. ● The third pathway is market redirection: shifting exports away from Europe toward Asian markets. This eliminates CBAM costs entirely while accessing faster-growing demand (4-5% annually in Asia versus 0-1% in Europe), requiring only $10-20 million in market entry costs. Chinese steel imports from Saudi Arabia surged 41% in the first nine months of 2025. Asian prices now exceed European levels when accounting for CBAM-adjusted net realizations. Chinese HRC domestic prices of $570-600/tonne plus Southeast Asian premiums ($620-680/tonne upon delivery) compete favourably with European import prices of €480-520/tonne minus (-) €40-90/tonne CBAM costs (net $482-526/tonne after converting from euro to US dollar). The profit margin differential—Asian sales generating $620-680/tonne versus European post-CBAM $482-526/tonne—creates $94-198/tonne advantage for redirection to the Asian market. Market redirection analysis does demonstrate that Asian markets offer Saudi steel and aluminum exporters superior net realized value when compared to CBAM-burdened EU exports, with China and broader Asian demand growing at 13-24% annually while requiring no carbon compliance costs or verification infrastructure.

Asian Markets as Strategic Alternative Chinese steel demand from Saudi Arabia grew 41% y/y in the first nine months of 2025, supplying 4.06 million tonnes compared to 0.15-0.20 million tonnes to the EU. Chinese domestic HRC averaged $442 per tonne, with import prices for Middle East material at $560-580/tonne fob, generating healthy margins without carbon penalties. Southeast Asian markets show similar dynamics: Malaysia's steel imports surged 17.3% with domestic capacity utilization below 35%. Aggregate Southeast Asian steel consumption grows 6-8% annually through 2030, outpacing the EU's 1-2% trajectory. China's aluminum production cap of 45 million tonnes annually, with domestic consumption exceeding 47 million tonnes, creates a structural deficit of 2-3 million tonnes. Further, Indian aluminum scrap imports from Saudi Arabia jumped 37% y/y. Transition costs for market redirection to Asia remain manageable: establishing presence in China and Southeast Asia requires $10-20 million per facility—substantially lower than $2-3 billion green hydrogen per facility for EU compliance (especially considering the scale and complexity of developing green hydrogen infrastructure. Green hydrogen projects typically involve significant investment in renewable energy sources.). The protectionism diagnosis: EU policy contradictions The EU's December 2025 reversal of its 2035 internal combustion engine ban provides definitive evidence of selective climate policy application. The December 16, 2025 proposal to reduce automotive sector emission targets from 100% to 90% by 2035—permitting continued hybrid vehicle sales—represents a retreat from environmental stringency when domestic economic interests do face pressures. This flexibility for domestic manufacturers contrasts sharply or markedly with CBAM's rigid application to foreign producers. Importantly, European manufacturers benefit from €1.8 billion in Battery Booster support for automotive supply chains, which includes preferential treatment for low-carbon steel 'made in the EU,' alongside continued free European Emissions Trading System allowances through 2034, while foreign producers face full carbon pricing. The automotive package's requirement that "low-carbon steel made in the EU" qualifies for emissions offsetting explicitly discriminates against imported green steel, including Saudi material produced at 0.3-0.5 tCO₂/tonne.

Steel safeguard measures intensified concurrent with CBAM: the October 2024 proposal cut tariff-free import quotas around 45% from 33 million to 18 million tonnes annually and doubled out-of-quota tariffs from 25% to 50%. If CBAM effectively prices carbon, additional quantitative restrictions become redundant - unless the true objective is limiting market access. This reflects intense competition, which is clearly evident in the distribution of market shares across the sector players. Strategic Recommendations and Financial Impact Assessment A. Why Saudi Arabia should not fully align with EU rules The financial arithmetic decisively argues against full EU compliance. Green hydrogen investment requires $2-3 billion capital per facility with 7-10 year payback periods serving markets growing at 0.5-1% annually, while Asian markets offer immediate $94-198/tonne margin premiums with 4-5% demand growth and zero compliance costs. Importantly, the EU's December 2025 automotive rollback demonstrates Brussels relaxes climate stringency when domestic interests are threatened, rendering long-term compliance investments vulnerable to arbitrary benchmark revisions. Further, Importantly, a policy framework that demands $2-3 billion investments while simultaneously cutting import quotas around 45% and doubling tariffs reveals protectionist intent rather than climate consistency. Moreover, Saudi Arabia's existing production achieves carbon intensities 29% below global averages—a substantial environmental contribution penalized rather than rewarded by CBAM's relative benchmarking system. A full alignment would divert capital from diversification priorities of Vision 2030 toward satisfying European regulatory demands that shift unpredictably, as evidenced by the ICE ban reversal after years of automotive industry planning for full electrification by 2035. B. Why limited strategic alignment makes economic sense Partial compliance targeting 15-20% of production for European premium automotive segments preserves optionality, while developing hydrogen technology capabilities aligned with Vision 2030. European automakers pay $150-250/tonne premiums for certified green steel in luxury and performance vehicles where environmental credentials constitute brand differentiation. Investing an amount of $500-800 million in pilot-scale green hydrogen facilities (150-250 MW electrolyzer capacity) producing 400,000-650,000 tonnes annually captures these premiums while maintaining the flexibility to serve Asian mass markets with conventional gas-based DRI production. This approach positions Saudi Arabia as credible climate participant in international forums and bilateral trade negotiations without bearing full decarbonization costs across entire production base. It exploits European willingness to pay for sustainability while maintaining cost competitiveness in Asian markets, effectively arbitraging between regional climate policy stringency levels. C. What Changes Under Market Redirection vs. EU Compliance If Saudi Arabia shifts 60-70% of its steel exports from Europe to Asian markets, it could boost its earnings by $35-50 million annually from 2026-2030 by increasing profit margins and avoiding €14-42 million in rising CBAM costs. It could also free up $2-3 billion for expanding traditional steelmaking (3-5 million tonnes), with high returns of 12-15%, compared to 6-8% for green hydrogen. While this move taps into Asia’s growing demand (4-5% yearly growth in China and Southeast Asia), it means sacrificing potentially higher-value European segments like automotive and aerospace, which are more profitable but smaller in volume.

If Saudi Arabia Maintains Full EU Compliance Strategy: |

|

|

|

|

|