|

In recent weeks, Riyadh has witnessed a notable decline in land values, particularly affecting large undeveloped parcels exceeding 5,000 meters. Last week, the CEO of Saudi Arabia's Real Estate General Authority, Engineer Abdullah bin Saud Al-Hammad, said in a TV interview with prominent Saudi presenter and journalist Abdullah Al Modifer that around 80% of the neighbourhoods in Riyadh witnessed a decrease in land value in recent weeks. He cited some examples of the recent decline in land prices: In Al-Khair district, the average price per square meter was about 2,440 riyals, and today it has dropped to around 1,820. In Aridh district, the average price was about 1,050 riyals, and now it has fallen to around 800 riyals or slightly more. In one of the suburbs, the average price was about 1,440 riyals, and now it is approximately 1,200 riyals or a little higher. His interviewer Al Modifer cited a higher decrease in land prices based on his interviews with many landlords across Riyadh who told him that the decrease ranged from 30% to 35%. Tax interventions targeting vacant or underutilized land tend to increase holding costs for owners, and exert downward pressure on the prices of taxed lands since owners look to sell or develop to avoid taxation. Let’s assume that there’s a piece of land of 6000 metres in the prime Al Malqa neighbourhood with the metre price around SAR 18,000 as advertised on Aqar on November 18. The asking price today is SAR 108,000,000. Since the neighbourhood falls under the first category of taxation, which’s 10% of the value of the land annually, this means that the owner will pay around SAR 10,800,000 per year if the owner keeps it. This massive recurring expense reduces the attractiveness of holding land idle, especially if the owner is not generating any income or return from the land in its undeveloped state.

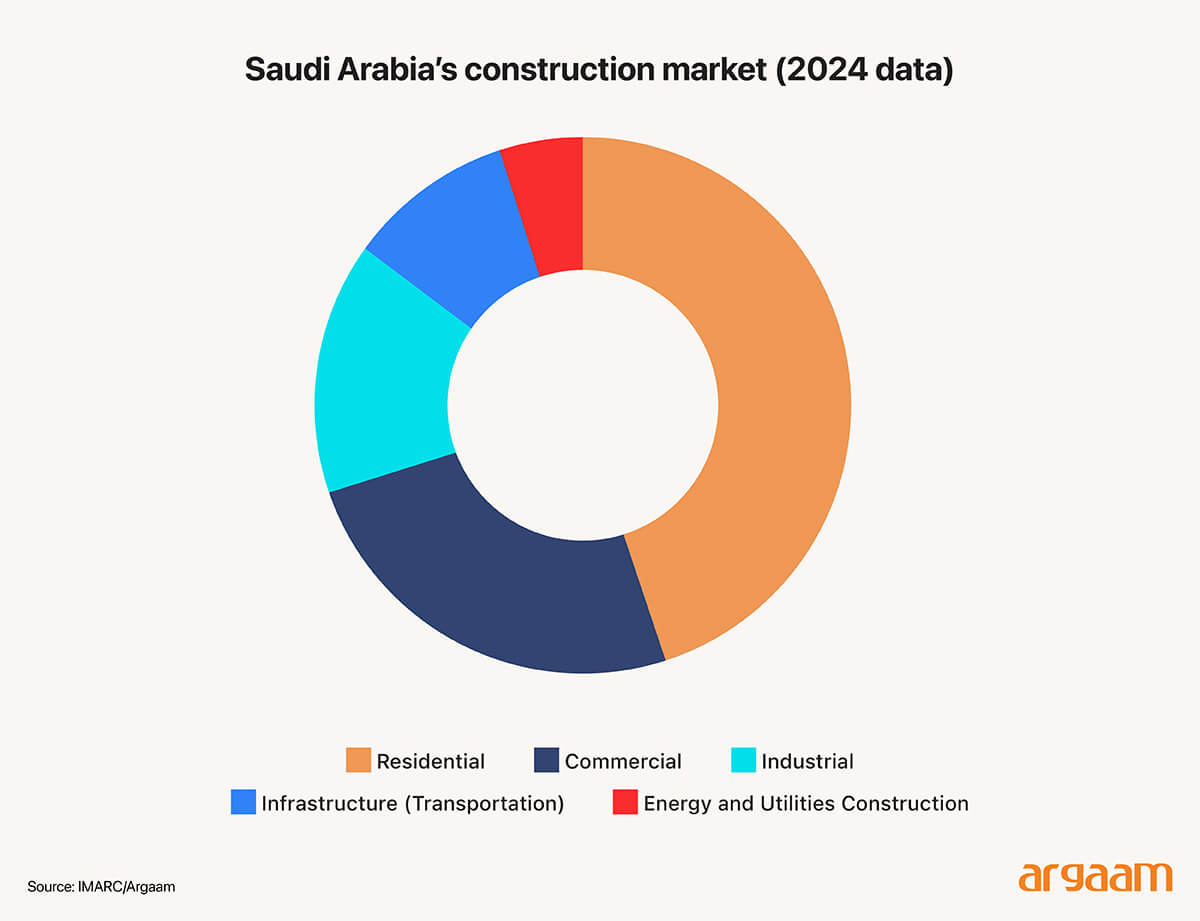

0.5% Value Surge per Acre Implementing a two-rate property tax system—raising the tax rate on land while lowering the tax rate on buildings—results in an increase in assessed land value per taxable acre, according to academic research and surveys of the system in the United States. (Journal of Housing Economics). The system dynamically raises land values as the demand for developed land increases with more construction and economic opportunity. A 1% increase in the adjusted tax differential (land tax rate minus building tax rate) leads to a 0.5% increase in assessed land value per taxable acre. The increase in land value occurs because lowering the tax on buildings encourages improvements or development, raising the value of underlying land. This system is built on the premise that the higher tax on land reflects the land's inherent value, which largely arises from its location and public investments, rather than the owner's actions. (Taxation of Vacant Urban Land, International Growth Centre, 2017). Even after development, the land itself retains significant value due to its location, scarcity, and public infrastructure, and taxing this value helps recover community-generated wealth. This means the increased value of land is largely created by factors outside the control of the landowner, such as public investments in infrastructure (roads, schools, utilities), services, and overall urban development driven by the collective efforts of the community and government. From the perspective of economics, it’s important to clarify that this system is not a double tax on the same value but rather two distinct taxes reflecting different components of property wealth. In a uniform property tax, taxing buildings and land at the same rate discourages improvements because additional development immediately increases tax. The two-rate system balances these incentives by making the cost of holding land high, but the cost of improving land relatively low.  This encourages expansions in the housing supply and commercial infrastructure, addressing shortages and facilitating economic scale. Saudi Arabia needs to build approximately 115,000 new homes per year until 2030 to meet demand and achieve its Vision 2030 goal of increasing homeownership to 70%. This requirement is driven by a young and growing population. The two-rate taxation raises the capital-to-land ratio, meaning that investments in buildings, machinery, and infrastructure increase relative to land. More construction activity leads directly to increased employment in the construction sector and related industries (manufacturing, materials, services). This contributes positively to aggregate demand and macroeconomic output in the short to medium term. The Saudi Arabia construction market size was valued at USD 101.4 Billion in 2025. Looking forward, the market to reach USD 138.4 Billion by 2034, exhibiting a CAGR of 3.52% from 2026-2034. (IMARC Group, 2025 report).

✂️ The scissors dynamics in the housing market The Kingdom’s real estate market has emerged as a cornerstone of economic activity, with total transaction value reaching SAR 267.8 billion in 2024 across 236,690 deals —representing exceptional growth of 37% y/y in volume and 27% in value – highlights a liquidity-rich market capable of digesting rapid supply increases without price dislocation. Housing markets function like any other market where the amount consumers are willing to pay and the amount suppliers are willing to supply are balanced at a certain price. This equilibrium price results from the continuous and simultaneous interactions of supply and demand - much like the two blades of a pair of scissors that together determine the cut (price), as famous British Alfred Marshall metaphorically suggested. (supply and demand, microeconomics 1890). Apartment prices in Riyadh have surged by 75% since 2019, while villa prices have increased by 40% in the same period. For 2024 alone, apartment prices climbed almost 11% and villa prices by around 6%, underscoring a market where demand consistently exceeds supply. As far as the relationship between the decrease in land prices in Riyadh and house prices, academic research shows that a change in land prices influences house prices slowly and to a smaller degree. (Town Planning Review, 2022). This slower adjustment happens because new housing supply adjusts with a significant time lag due to development processes, planning permissions, and construction times. So house prices do not respond quickly or proportionally to land price changes. The housing market further includes transactions of existing homes with prices determined by the interaction of supply and demand.  The real estate sector in Saudi Arabia lies at the heart of Vision 2030. The scale and continuity of the Kingdom’s real estate and infrastructure projects indicate that it has already moved from the vision phase to the execution phase. This transition is supported by sustainable financing mechanisms that align with societal needs and global standards of governance and environmental responsibility—instilling confidence in both local and international developers and investors. Click Here to Read Complete Report

As far as demand is concerned, it’s determined by the growing population in Saudi Arabia and the government schemes to facilitate home ownership to Saudi citizens, especially to get a mortgage. For Saudi Citizens (First-Time Homebuyers), the maximum LTV ratio is typically 90% (requiring a minimum 10% down payment). This cap was raised from lower percentages (70% in 2014 and 85% in 2017/2018) as part of government efforts under Vision 2030 to increase homeownership among citizens. Government-backed programs, such as the Sakani program, can also offer additional support, potentially covering interest for eligible low-income individuals. Expats generally face stricter lending criteria and higher down payment requirements, often needing to put down at least 30-35% (implying a 65-70% LTV ratio). |

|

|

|

|

|