|

In a surprising turn of events, Dubai-based Dubizzle Ltd. abruptly postponed its much-anticipated initial public offering at the Dubai Financial Market—just one day before the bookbuilding process was set to kick off. Valued at an estimated $2 billion, this move has left both stock market analysts and investors alike scrambling for answers. The company reported net losses between 2022 and the first half of 2025, mainly due to one-off items such as share-based payments to employees and tax charges. On an adjusted basis, it was profitable in 2023, 2024, and the first half of 2025, according to its IPO prospectus. Dubizzle operates classifieds portals across the Middle East and North Africa. It generates 89% of its revenue in the UAE and entered Saudi Arabia in 2024. While no official explanation has been provided, we believe the prevailing unfavorable conditions in the IPO landscape played a decisive role in this sudden withdrawal. Yet, as we delve deeper, this analysis uncovers a web of underlying factors that have historically led to IPO cancellations, drawing on compelling case studies from major stock exchanges across the US and Europe. And what becomes of companies that step back from their IPO ambitions? A staggering discovery lies beneath the surface, hinting that only a mysterious fraction ever returns to the market for a successful offering. The answer is at the end of our analysis.

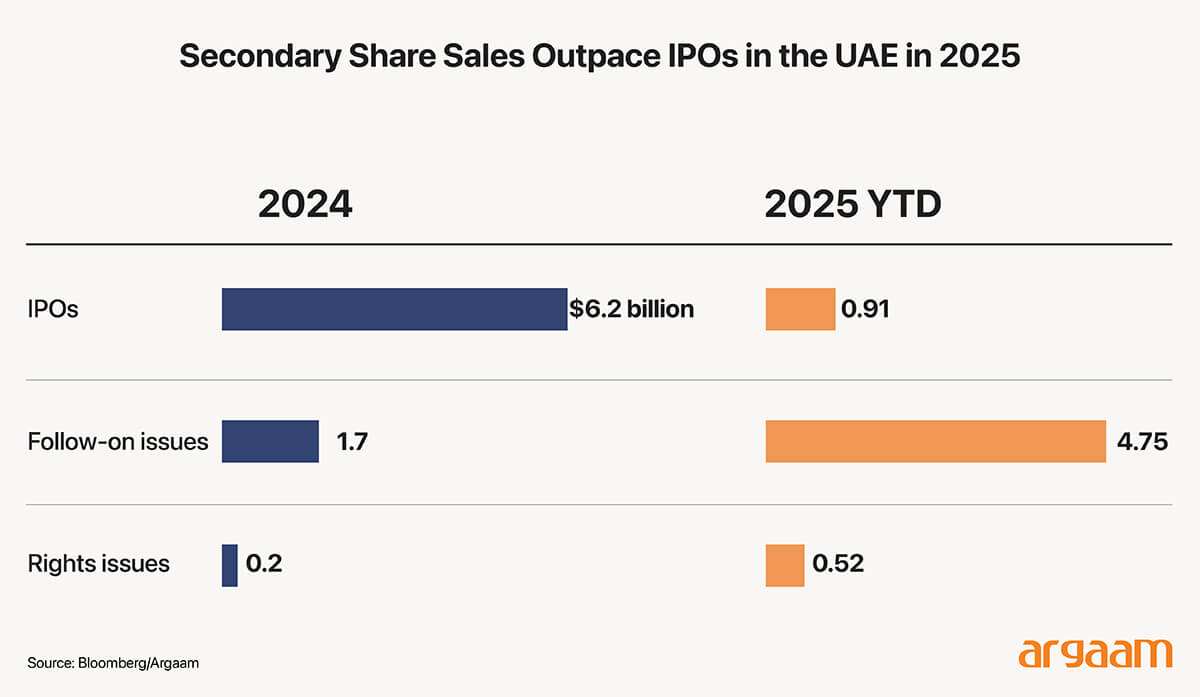

Secondary share sales outpaced new listings in UAE The region continued to demonstrate healthy activity and investor interest, with 11 initial public offerings (IPOs) raising US$0.7b in total proceeds. The number of listings increased by 120% when compared with the same quarter last year. (EY MENA IPO Eye Q3 2025 report). The Kingdom of Saudi Arabia remained the most active market with eight IPOs that together raised $ 637 million. But in the UAE, the IPOs were eclipsed by the issuance of additional shares for slae by already listed companies. This issuance is called ‘follow-on offering’. Proceeds neared $5 billion this year and surpassed initial share sales. (Bloomberg).

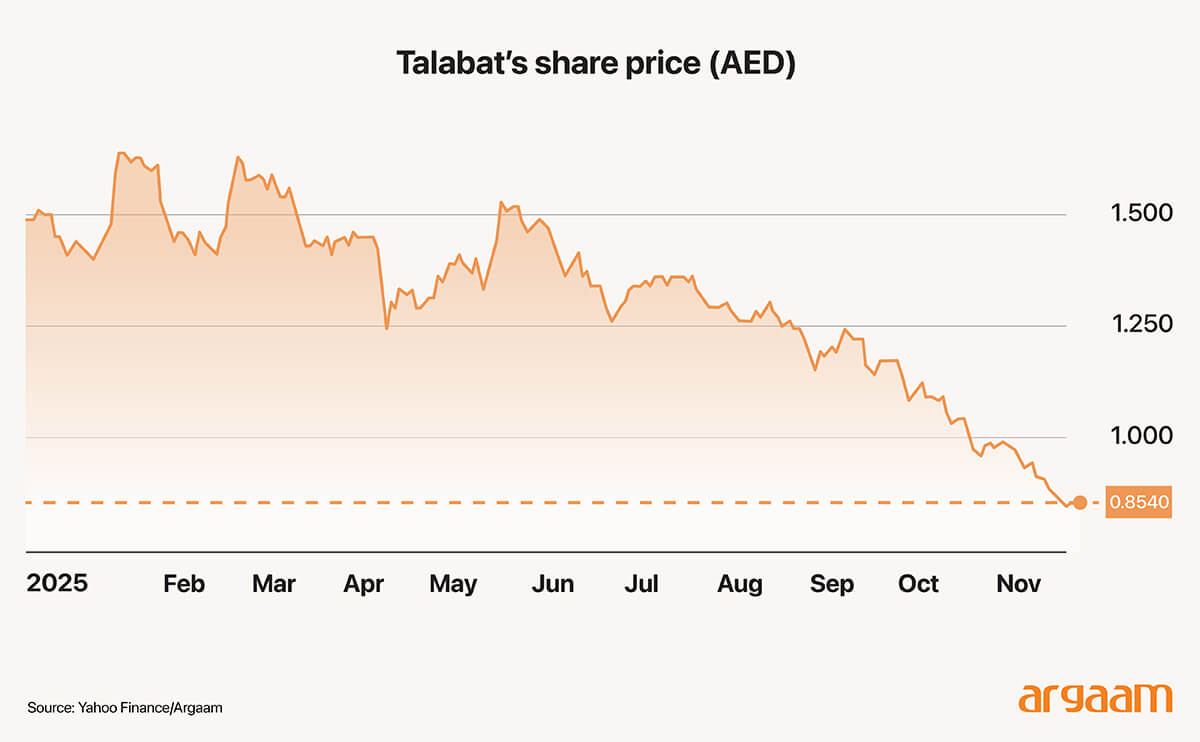

So we understand that the demand on the follow-on deals rather than new listings over the past year implies that investors’ attention and capital may be diverted toward follow-on deals rather than new listings. Such competition could reduce demand for Dubizzle’s shares and impact the success of its IPO. Also, the current trading prices of the shares of the two largest IPOs over the past 12 months, Talabat Holding Plc and Lulu Retail Holdings Plc, are lower than the prices at which the shares were originally offered to investors during their IPOs as we see in the two charts below.    The fact that the two largest recent IPOs in the UAE—Talabat Holding Plc and Lulu Retail Holdings Plc—are trading below their offer prices suggests negative investor sentiment or uncertainty regarding the valuations of newly listed companies. This can lead to subdued demand and downward pressure on the IPO price for Dubizzle. The trademark breadths factor Dubizzle primarily operates as an online marketplace and classified ads platform. This relatively focused trademark scope may signify to investors that its future options for brand extension across diverse product or service categories are limited and doesn’t have a greater trademark breadth. Empirical evidence from a study of 1510 European firms that went public between 2002 and 2015 demonstrates that greater trademark breadth is statistically associated with higher IPO valuation and better post-IPO performance. (Journal of business venturing, 2022). Greater trademark breadth means a firm’s trademarks legally protect its brand in a larger variety of product or service classes, thereby increasing the firm's flexibility and options to leverage the brand across multiple markets or industries.  A limited trademark breadth for Dubizzle means that this would likely limit its perceived real options value at an IPO. Investors might interpret this as less flexibility for future expansion or brand leverage, which could dampen its IPO valuation and the potential for strong post-IPO performance. In assessing the breadth of a trademark, we have to bear in mind two key IPO financial metrics: (Tobin’s Q Ratio and Firm Performance)

Tobin’s Q This is a number that compares how much a company is worth on the stock market (what investors think it’s worth) to how much it would cost to replace everything the company owns (its assets like buildings, equipment, and inventory). ● If Tobin’s Q is high, it means investors believe the company is worth more than just the value of its physical stuff—usually because it has valuable brands, technology, or growth potential. ● If Tobin’s Q is low, investors think the company isn’t worth much more than its physical assets. Simply put, Tobin’s Q measures how much extra value investors see in a company beyond its basic physical belongings. Buy-and-Hold Abnormal Returns (BHARs) This is a way to measure how well the stock does after a company’s IPO compared to what the overall market is doing. If a company like Dubizzle has a limited trademark breadth, investors might see less extra value beyond the company’s physical assets (lower Tobin’s Q) and the company’s stock might not perform as well compared to the market after going public (weaker BHARs). This means they might get a lower valuation at IPO and less rewarding investment returns afterward. A Look Into Historic Market Withdrawals Throughout history, numerous highly anticipated offerings have been withdrawn. Understanding these episodes provides valuable insights into the complexities and challenges that companies face on their path to going public. The American biopharmaceutical company Perlegen Sciences, Inc. made the decision to withdraw its $115 million IPO after careful consideration of certain billing matters related to a government contract. The company voluntarily addressed these matters by engaging independent counsel to conduct a thorough review and subsequently implemented recommendations to enhance its internal controls and compliance framework. These actions reflect Perlegen’s commitment to maintaining the highest standards of corporate governance and ensuring a strong foundation for future growth.(Reuters archive) These agreements would have restricted shareholders from selling or transferring shares for a period typically post-IPO to stabilize share prices. The company’s shift in strategic direction, including its plan to list on Nasdaq, compounded the decision to halt the offering. (Los Angeles Business Journal)

Goldman Sachs decided to cancel its planned initial public offering (IPO) primarily because financial sector stocks experienced a significant decline after the high-profile rescue of Long Term Capital Management (LTCM), a major hedge fund. (global capital) The LTCM crisis triggered market turmoil and heightened concerns about the financial health of leading commercial and investment banks due to trading losses and exposure to vulnerable emerging markets. This market instability led to a drop in stock prices, especially within the financial services sector, making it unlikely that Goldman Sachs could achieve its target valuation or raise the expected $3 billion to $4 billion in the IPO. For Goldman Sachs, forecasts had initially valued the firm up to $40 billion at the time of this cancelled IPO in 1998, but in a declining market, the valuation was likely to fall to around $15 billion.

The Long Shadow on Future Capital Raises A withdrawn IPO leaves a reputational blemish on a high-growth venture. This stigma signals to investors and the market that the company faced significant issues. When these firms finally do go public, they tend to raise substantially less capital than they might have in their initial attempt. (Journal of Business Venturing Insights, June 2024). The initial withdrawal signals to investors and the market that the firm faced substantial challenges, like the ones we explained earlier in this analysis, but also perhaps due to internal disagreements about the valuation. Founders often believe the firm's prospects and intrinsic value are higher, while investors or underwriters may propose more conservative valuations based on market conditions and investor feedback. When consensus cannot be achieved, firms may choose to withdraw the IPO rather than risk going public at a price that founders or major shareholders perceive as a loss of value or dilution of control.  This negative signal lingers, affecting investor confidence in subsequent offerings and market performance. A survey published in the Journal of Business Venturing Insights in 2024 found out that between 1997 and 2021, approximately 17% of IPO attempts in the NASDAQ and NYSE markets were withdrawn, amounting to nearly $150 billion in unrealized offer proceeds. This example highlights the financial magnitude of such failures. To isolate firm-level dynamics contributing to withdrawal, the survey was performed on the pharmaceutical manufacturing industry, the second most frequent IPO sector, mitigating distortions from volatile industries like technology during the late 1990s bubble.

The 9% return rate and the ‘lemons’ problem Another survey used data from the Thomson Financial Securities Data (TFSD) and covered U.S. firms filing for firm commitment to IPOs between 1985 and 2000. (Journal of financial economics, 2007). It found out that only about 9% of these firms eventually return to the market for a successful IPO offering. This low return rate indicates that once a firm withdraws its IPO application, the likelihood of successfully going public later is limited. The average time taken for a withdrawn IPO to return successfully is around 2 years, with a broad range from as little as a few months up to nearly 10 years.  This suggests that firms may need significant time to address issues that led to withdrawal before returning successfully. Firms with venture capital backing are more likely to return successfully. Venture capitalists serve as a form of certification or quality signal to the market. Because VCs typically conduct thorough due diligence before investing, their involvement reduces the information asymmetry between the firm and potential investors. This "certification" helps alleviate the classic "lemons" problem (adverse selection) where investors worry about overpaying for overvalued or risky firms. The survey further found that approximately 75% of firms that return for a successful IPO use a different underwriting bank than in their initial withdrawn attempt. This supports the notion that firms learn from their first experience and seek higher-quality partners to improve their success odds. |

|

|

|

|

|