Western Union's presence in the Middle East dates back to 2011, with a strong foundation built on a vast network of retail agent locations. The UAE was the UAE first country in Middle East, Africa to offer Western Union's international business payments service. (Western Union archived press release).

The time-honoured company, which was established in New York in 1851 as a telegraph company to network the different US states, started its operations in the Arabian Gulf, the Middle East and Africa to provide cross-border business payments and foreign-exchange solutions to small- and medium-sized enterprises (SMEs).

The company has opened physical locations throughout 174 years in more than 200 countries with more than 550,000 agent locations. (About Us – Western Union).

But Western Union’s dependence on brick-and-mortar outlets, especially in the Middle East, puts it at a competitive disadvantage in an increasingly digital financial ecosystem, where speed, convenience, and integrated financial services are paramount.

Today it’s facing a real disruptive challenge that’s different than any other disruption it has faced during its very long history: FinTech.

Unlike Western Union’s branch-based model, FinTech solutions leverage mobile devices, cloud computing, and data analytics to provide faster and more accessible services without the need for physical locations, reducing operational costs and improving customer experience. (International review of financial analysis, 2022).

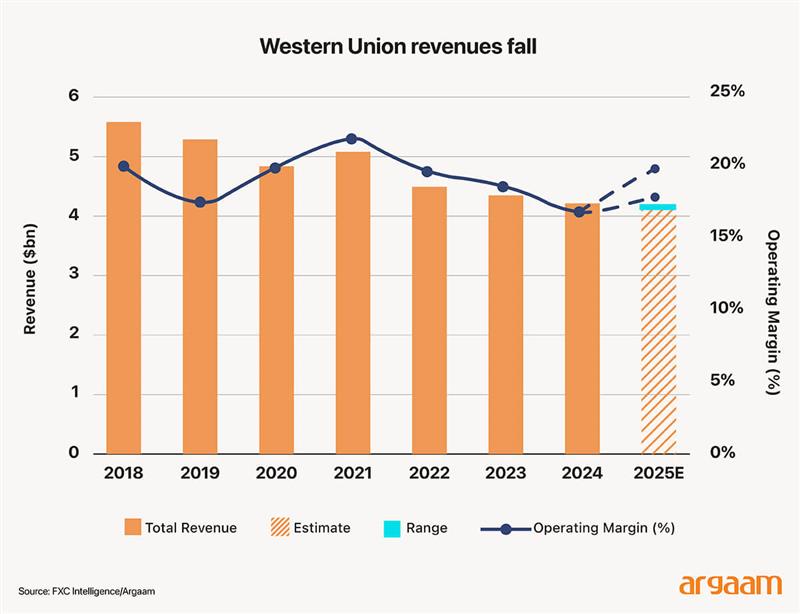

Middle East revenues take a hit

As of December 31, 2024, approximately 380,000 agent locations (physical stores) had conducted money transfer activity in the previous 12 months. (western union’s 2024 financial statement)

Revenues derived from physical stores are a significant component of the Consumer Money Transfer and Consumer Services segments and are emphasized as important to the overall business and revenue generation.

Consumer Money Transfer segment, which’s customer-to-customer payments, represents about 90% of total company revenues in 2024.

The Middle East, Africa, and South Asia (MEASA) region contributed to Consumer Money Transfer and Consumer Services revenue of $665.3 million (against a total of $829.8 million in 2023).

The MEASA region experienced a significant decline in revenue driven by a reduction in transactions originating from Iraq.

The 2024 Consumer Money Transfer revenue in MEASA decreased about 20%.

As we see in the chart below, across the company’s stores around the world, the consumer money transfer (CMT) revenue declined 4% in Q4 2024 to $ 939m, contributing to an overall 5% CMT decline for the full year to $3.8bn.

This highlights significant challenges for the company’s traditional physical store-based money transfer model. Physical stores alone no longer provide a sustainable competitive advantage in the rapidly evolving payments landscape.

Western Union’s Transaction Drop Reflects Shifting Consumer Habits

The company has not published a cumulative total number of consumer-to-consumer and business payments since its inception. It reports transaction volumes annually in its financial statements.

In 2024, Western Union handled nearly 290 million total transactions, compared to total transactions of 619 million transactions in 2014. (gurufocus, 2025, western union archived press release, 2015).

Accordingly, Western Union experienced approximately a 53.15% decline in total transactions over the 10-year period.

This sharp decline in Western Union's money transfer transactions can be attributed largely to its reliance on traditional methods that require customers to physically visit a location to send money.

This "old way" of transferring money contrasts with the growing trend of digital, instantaneous, and remote money transfer services enabled by FinTech innovations.

Why MENA Fintechs Are Outpacing Western Union’s Growth Surge

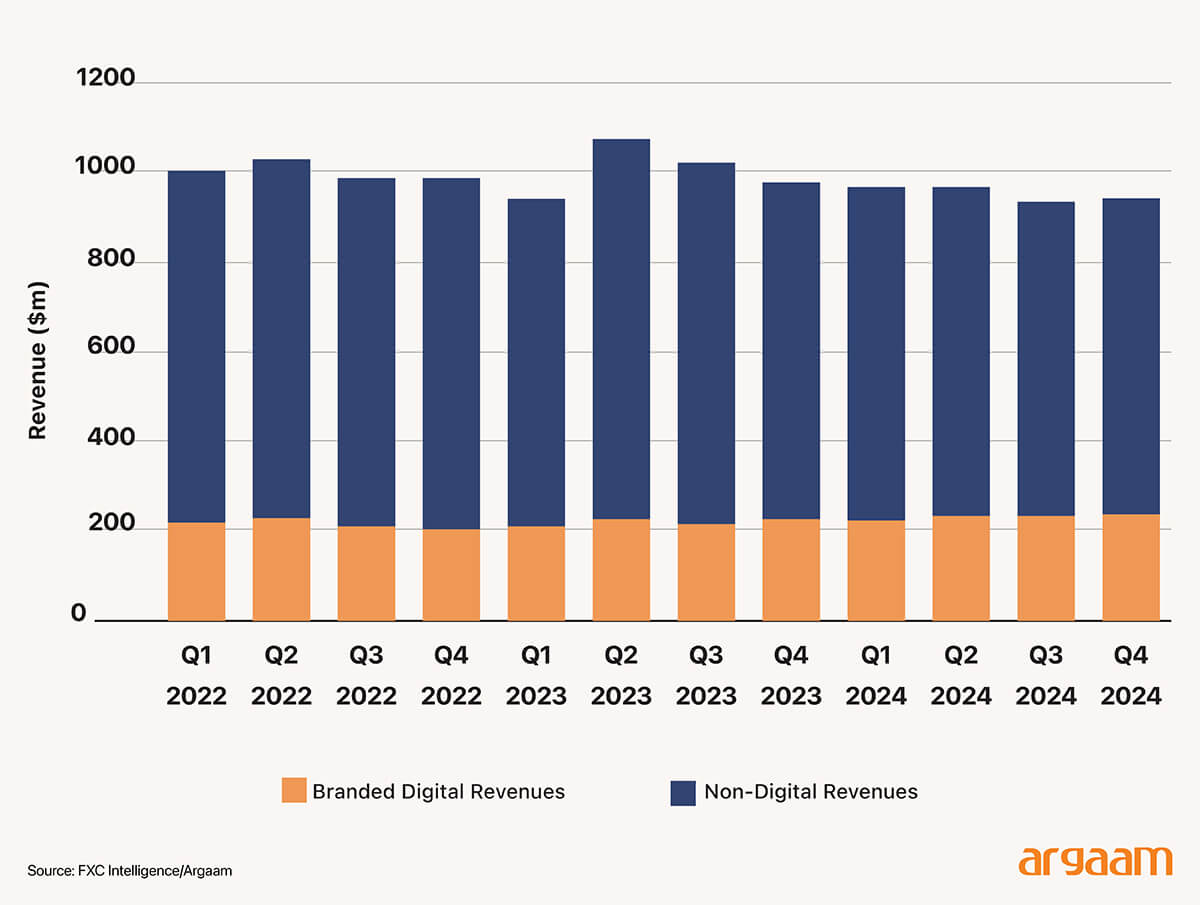

Within transfers, pushing digital growth remains a key part of the company’s Evolve 2025 profitability strategy. Branded digital revenue grew 7% in Q4 2024 to $235m, making up a 25% share of revenue versus 23% last year, with Branded Digital transactions growing 13% to make up 32% of total transactions. (FXC Intelligence, 2024).

The company has cited strong digital performance in Mexico, Japan, the UK and Chile, but not yet in the Middle East, the Arabian Gulf or North Africa.

For 2025, the company is forecasting a 0.5-2.8% decline in revenue on a GAAP basis to $4.09bn-4.19bn, with an operating margin of 18-20%.

PS: GAAP stands for Generally Accepted Accounting Principles. It is a standard framework of guidelines and rules used for financial accounting and reporting in the United States.

Though the company’s revenues from the new digital services increased by 8% year-over-year in the past five years with a 13% increase in transactions in 2024 compared to 2023, the comparison with the nascent Fintech companies in MENA, as it’s our region of interest in this analysis, show a yawning gap mainly due to improved brand recognition for these new companies with several managed to win the customer’s trust in a short period of time.

Though the company’s revenues from the new digital services increased by 8% year-over-year in the past five years with a 13% increase in transactions in 2024 compared to 2023, the comparison with the nascent Fintech companies in MENA, as it’s our region of interest in this analysis, show a yawning gap mainly due to improved brand recognition for these new companies with several managed to win the customer’s trust in a short period of time.

These Fintech firms are experiencing rapid expansion, with customer bases that have reportedly outpaced the number of traditional bank customers in the region.

Actually, some companies to efficiently amassed more than ten million customers each, rivalling the leading banks in the region.

The Saudi National Bank (SNB) is the largest bank in Saudi Arabia by number of customers, serving over 14.2 million as of March 2024.

Emirates NBD is the largest bank in the UAE by the number of customers, with over 9 million customers as of September 2025.

The National Bank of Egypt (NBE) is the largest bank in Egypt in terms of the number of customers with over 20 million customers.

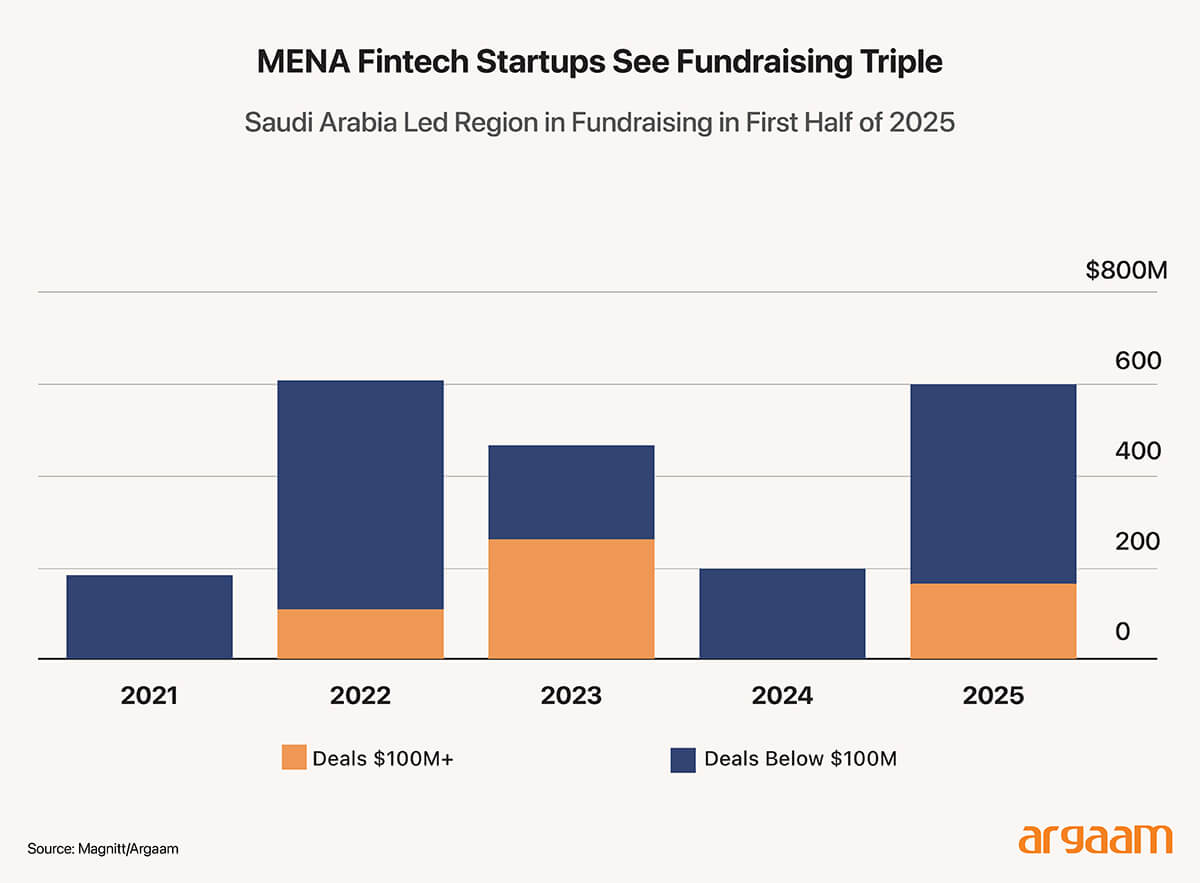

Over the last few years, the number of fintech companies has risen to more than 1,000. Four unicorns have emerged, many more are in the pipeline, and capital has continued to flow into the market, with $1.9 billion invested in 237 deals during 2023 and 2024. (McKinsey & Company 2025).

Saudi-based shopping and financial services app, Tabby, secured $160 million in a Series E funding round in February 2025. (Tabby press release, 2025).

This boosted its valuation to $3.3 billion, making it the region’s most valuable fintech startup. (PS: As of November 2025 Western Union has a market cap of $2.8 billion, (Trading Economics).

Egyptian e-payment company Fawry comes in second, boosted by its 53.1 million customers, followed by Saudi fintech and Insurtech company Rasan, which went public on the Saudi Exchange (Tadawul) in 2024, with its market cap hitting nearly $1.9 billion on February 20, 2025.

Going forward, MENA is expected to be the fastest-growing region globally, with 35% annual growth in fintech net revenue until 2028, compared with a global average of 15%.

Going forward, MENA is expected to be the fastest-growing region globally, with 35% annual growth in fintech net revenue until 2028, compared with a global average of 15%.

Before 2022, companies focused on growth and spent heavily on marketing. After 2022, they placed a much stronger emphasis on unit economics to balance growth with a path to profitability.

PS: Unit economics refers to the direct revenues and costs associated with a single unit of product or service sold by a company. It focuses on measuring the profitability and sustainability of each unit transaction to ensure that the business model is economically viable when scaled

Competing against nimble Fintechs that continuously introduce disruptive features and seamless onboarding processes remains a daunting challenge for Western Union. |