Food delivery platforms built the sector's foundations pre-COVID on an asset-light, commission-based model focused on GMV growth. The pandemic triggered an unprecedented acceleration but also a fundamental shift in business model — quick commerce emerged as a distinct category, with a wave of new entrants raising mega-rounds in 2021 on a "scale first, profit later" thesis, betting that owned dark store networks would prove impossible to dislodge.

The correction that followed was severe. As Covid-era demand normalised, unit economics collapsed at the same moment rising interest rates made capital scarce — platforms relying on cheap funding faced closed markets and weaker demand simultaneously. Leading players retreated, merged, or were dismantled.

Investor focus shifted decisively toward contribution margin and EBITDA breakeven discipline. Emerging markets, most notably India, offered a sharply contrasting picture.

The market consolidated around multiple viable scaled players, Blinkit, Zepto, and Instamart, rather than collapsing as it did in Europe. The dark store model's long-term viability was validated when Blinkit, the market leader with over 50% share, demonstrated a credible path to profitability at scale.

The GCC came to quick commerce later, benefiting from the lessons of both the Western collapse and India's more measured recovery, though competitive intensity has since tested investor patience.

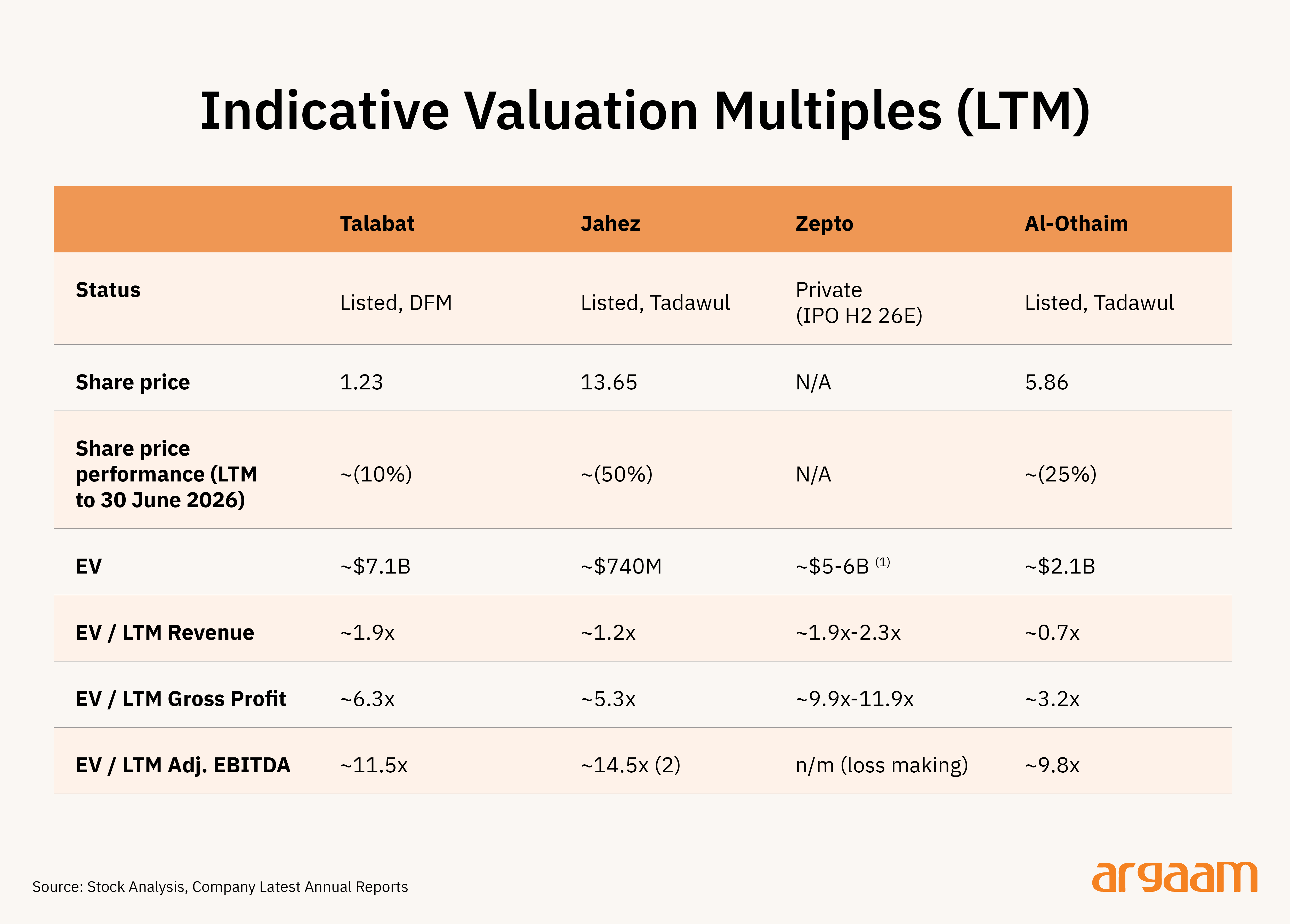

Talabat trades approximately 20-25% below its December 2024 IPO price, while Jahez has lost more than 40% of its value over the past year, despite both platforms growing GMV through the same period.

Editorial Note

1) It is worth noting that the GCC operates with structurally different economics — lower population density and higher operating costs offset by stronger consumer purchasing power and higher average order values, meaning the path to dark store profitability is driven by higher revenue per order rather than order volume density, and is likely to take longer to materialise than India's experience would suggest.

GCC q-commerce is expected to grow at approximately 22% annually, reaching an estimated $12.5 billion by 2031, but from a current base significantly smaller than India's, reinforcing that operators cannot simply transplant the India playbook and expect the same outcome.

2) The data presented in this analysis has been compiled to identify broad sector-level patterns and directional trends rather than to draw precise company-by-company comparisons. Business models and accounting disclosure standards vary sufficiently across operators to make direct comparison misleading in many instances.

A detailed analysis of Zepto and Al-Othaim — covering unit economics, operational performance, and competitive positioning — will be published as a separate standalone report by the Argaam Intelligence team.

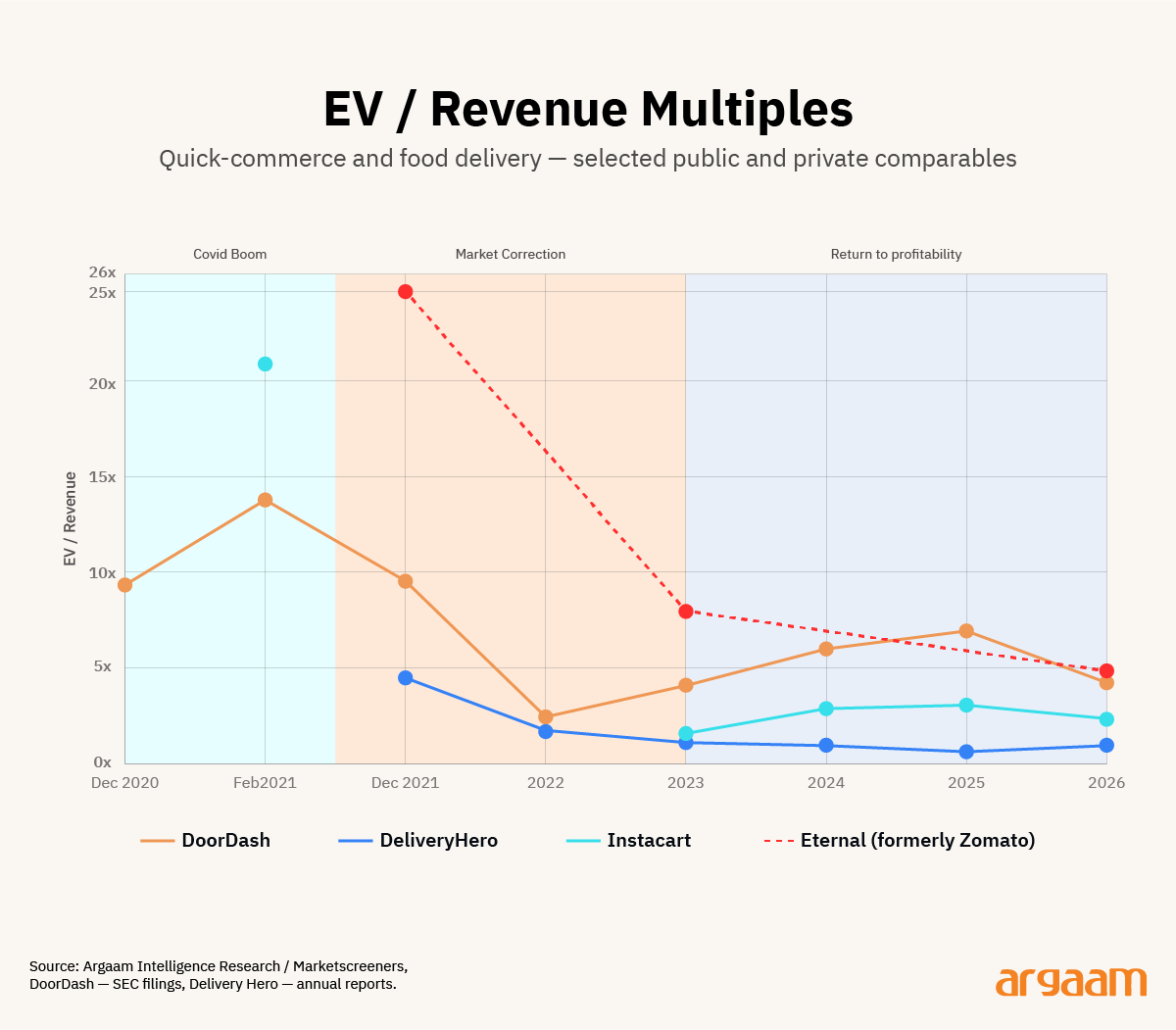

Deliveroo: £7.6 billion in 2021. £2.4 billion in 2025

At the sector's peak in 2021, most capital formation occurred through IPOs and private funding rounds rather than M&A — valuations were simply too high for strategic buyers to transact.

The few deals that did occur reflected peak sentiment: Just Eat's acquisition of Grubhub for $7.3 billion implied approximately 4.0x EV/Revenue (FY2020 revenue of ~$1.8 billion), an asset sold just a few years later for $650 million. (Equity value used for enterprise value, minimal debt/cash assumed.)

The recent era tells a starkly different story. Prosus acquired Just Eat Takeaway for an Enterprise Value of approximately €2.8 billion in February 2025, implying approximately 0.6x EV/Revenue (FY2024 Revenue of €5.1 billion). (EV is approximated as equity value of €4.1B less gross cash of €1.3B; the true EV may differ pending exact debt position.

DoorDash acquired Deliveroo for an enterprise value of approximately £2.4 billion in May 2025, implying approximately 1.2x EV/Revenue (FY2024 Revenue of ~£2 billion). — a significant discount to Deliveroo's 2021 IPO valuation in London Stock Exchange at £7.6 billion.

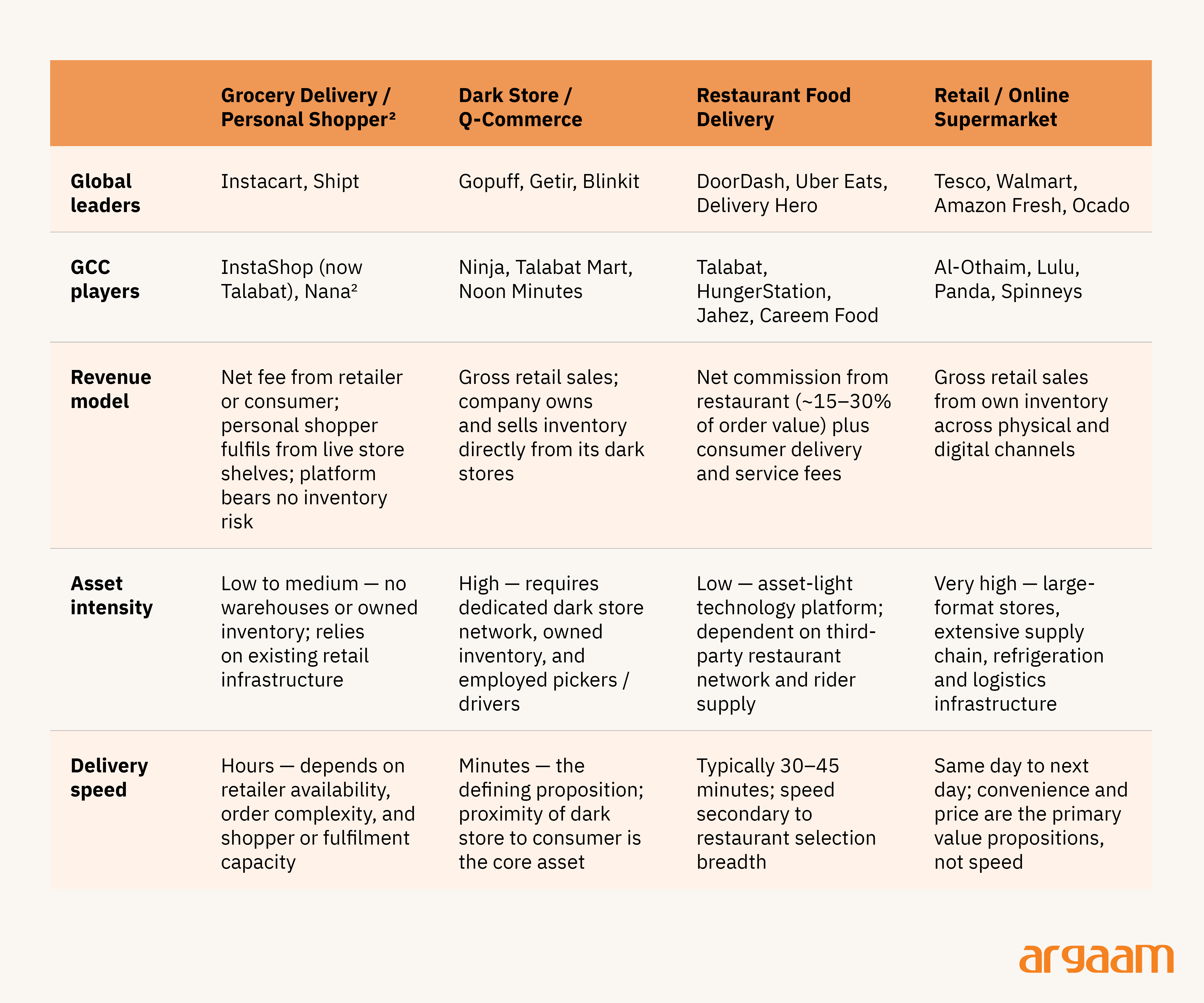

Sector Landscape

The on-demand delivery sector encompasses a spectrum of business models that differ fundamentally in how they source, store, and monetise goods. Understanding these distinctions is essential before drawing any cross-company comparisons.

Key Notes:

◈ Company names listed are selective. They are intended to represent the business model of each category rather than constitute a comprehensive market map.

◈ Delivery Hero retains an 80% stake in Talabat following the December 2024 DFM IPO which sold 20% for $2 billion.

◈ HungerStation sits outside the Talabat listed perimeter and is owned 100% directly through the Delivery Hero structure.

◈ Careem Food is the food delivery vertical within Careem Technologies, the super-app entity majority owned by e& with Uber as a significant minority shareholder (12.5% stake).

◈ Grocery delivery platforms assign a personal shopper to pick orders from live retail store shelves on the consumer's behalf (Instacart) or aggregate retailer inventory digitally through a partner fulfilment network (InstaShop).

In both cases, the platform owns neither the inventory nor the store infrastructure, and revenue is recognised as a net fee rather than gross retail sales.

◈ Nana entered financial reorganisation proceedings in April 2026, and its operational status remains uncertain.

Blended models and super apps

◈ Several players operate across multiple segments simultaneously. Talabat combines restaurant food delivery, grocery delivery, and dark stores.

◈ At the furthest end of the spectrum, super-apps such as Grab and Careem embed delivery within broader platforms spanning ride-hailing, financial services, and digital payments, where delivery is typically a secondary revenue line cross-subsidised by the wider platform.

◈ Evaluating any company in this sector demands a clear understanding of its underlying revenue mix and business model before any financial conclusions can be drawn.

Market Evolution: From Growth At All Costs To Sustainable Profitability

The q-commerce sector has undergone a dramatic transformation over the past five years. The chart below traces this evolution through select public company valuations and private funding rounds.

Peer Benchmarking

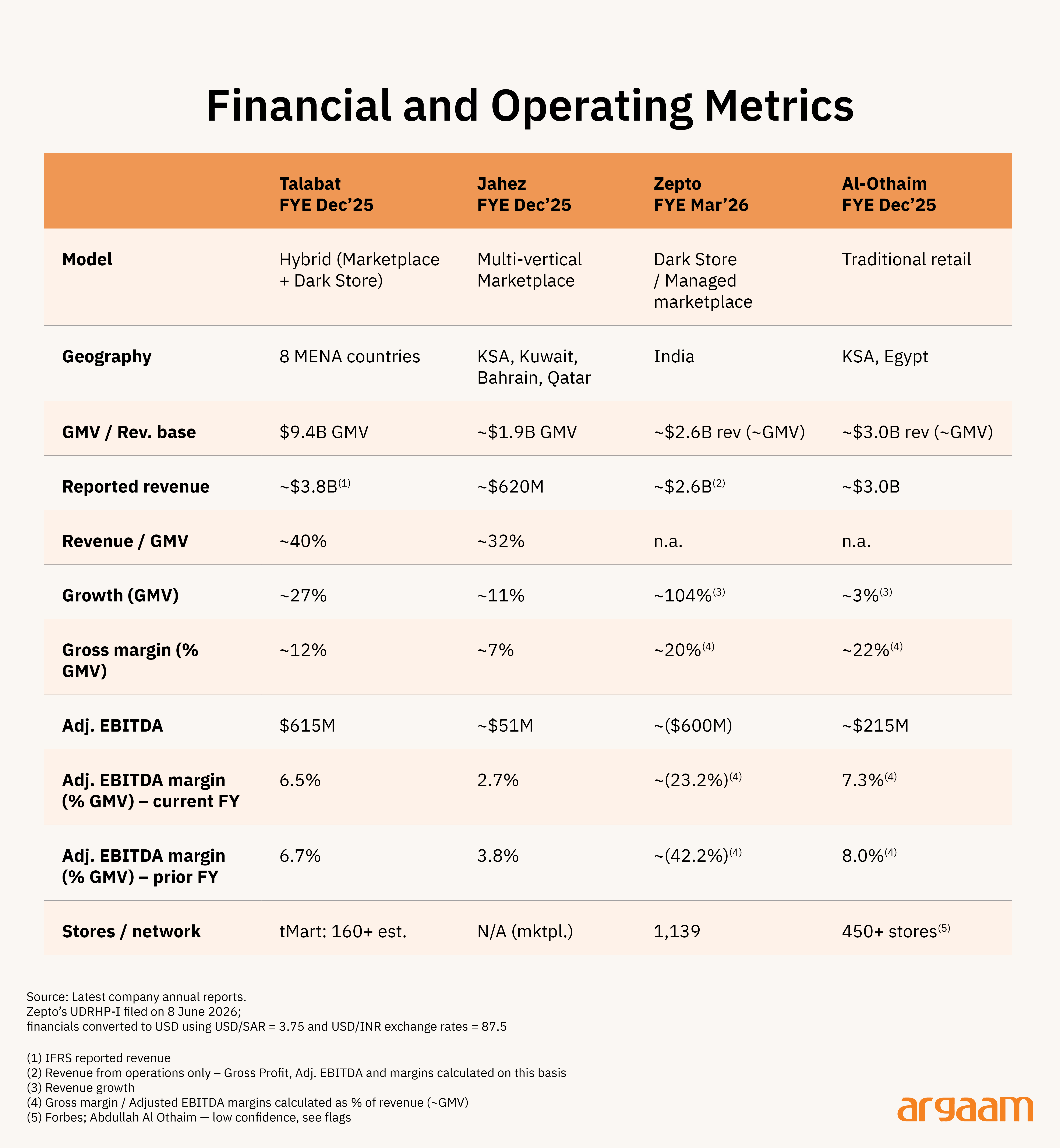

Four companies anchor this benchmarking exercise, selected to represent the principal business models across the sector landscape: Talabat (hybrid marketplace and dark store), Jahez (multi-vertical marketplace), Zepto (dark store operator), and Abdullah Al-Othaim Markets (traditional retail with an online channel).

Note: Market data as at 30 June 2026. All figures in USD except share price information (local currency).

◈ Indicative IPO valuation range based on recent market commentary. Zepto last raised $450m round at $7 billion valuation in October 2025.

◈ Jahez's EV/EBITDA of 14.5x should not be interpreted as a valuation premium relative to peers. The elevated multiple reflects a compressed EBITDA denominator.

FY2025 adjusted EBITDA margin declined to 2.7% of GMV as the company absorbed significant promotional spend to defend market position. EV/Revenue of ~1.2x is a more reliable comparator.

A note on comparability

The data in this table has been assembled to draw sector-wide themes and directional observations rather than precise cross-company comparisons.

The four companies operate fundamentally different business models, and their revenue recognition differs accordingly. Zepto and Al-Othaim report revenue at gross (≈GMV) as inventory owners, while Talabat and Jahez largely report net commissions from orders (=GMV).

Both, however, operate additional business lines, Talabat's tMart dark stores and Jahez's non-food verticals, that further complicate the picture. Revenue and EV/Revenue multiples are therefore not directly comparable. EV/Gross Profit and EBITDA provide a more meaningful basis, though both carry their own limitations as set out below.

Gross profit is a closer metric but still imperfect; cost of sales definitions differ across operators and require alignment before meaningful comparison can be drawn, as items such as rider and delivery costs may be treated differently across the peer set.

Gross margins are also calculated on different denominators (GMV vs. revenue), so they aren't directly comparable — even if we assume revenue ≈ GMV for the dark store/retailer business. EBITDA has become the primary metric investors focus on, but it should also be read with care.

Capital intensity profiles differ significantly across the four models, adjusted EBITDA definitions vary, and context/sustainability matter more than the headline number. An EBITDA decline driven by deliberate investment is not the same as one driven by structural margin erosion.

Ultimately, for q-commerce businesses, store-level or order-level unit economics, i.e., what each business earns per order after all directly attributable costs, is the metric that matters most, yet it remains the least disclosed across this peer set.

What the data tells us

1) Al-Othaim is best read as a floor, not a comp. As a diversified Saudi retailer, spanning supermarkets, wholesale, general merchandise and property, Al-Othaim is not a direct q-commerce comparable. Yet its ~3% revenue growth against a ~7% adj.

EBITDA margin is instructive. It reflects both the maturity of physical retail as a category and the structural pressure q-commerce is exerting on traditional retailers, which are struggling to match the speed and convenience of on-demand platforms for high-frequency, small-basket missions.

At 3.2x EV/Gross Profit and 9.8x EV/Adj. EBITDA it trades broadly in line with mature global retail peers, with the market pricing limited growth optionality.

2) Investors have converged on a materially more disciplined valuation framework across the q-commerce sector. The market still pays for growth without profitability, but the premium has narrowed considerably.

Even Zepto, the fastest grower in the table by a wide margin, isn't priced anywhere close to the premiums loss-making platforms commanded in 2021. Setting aside model differences, the full comp set sits within a relatively narrow EV/Revenue band of 1.0x to 2.0x (excluding Al-Othaim).

3) The growth-profitability trade-off remains unsolved. Zepto grew at 104% (revenue from operations) and posted a -23% adjusted EBITDA margin; Al-Othaim grew at 3% and earned a 7.3% margin. Talabat and Jahez sit somewhere in between.

Whilst a small sample, this mirrors a central tension running through the broader q-commerce sector: no operator has yet been able to deliver strong growth and sustainable profitability simultaneously.

The pattern is consistent: the faster you grow in quick-commerce, the more money you tend to lose, because winning customers requires heavy spending on marketing, discounts, warehouse expansion, and technology.

No q-commerce company in this table has yet convincingly demonstrated that it can grow fast and make healthy profits at the same time. That unresolved question sits at the heart of every valuation conversation in this sector.

4) Competition is fierce, and investors are unforgiving for margin compression even when framed as temporary and reversible. EBITDA is declining across every profitable name in the table despite each growing revenue or GMV.

Across the GCC, intensifying competition and the investment required to respond to it have compressed margins across marketplace and hybrid operators alike. Management assurances that margin pressure is temporary and controllable have done little to arrest share price declines across the sector. Investor patience for margin compression has limits, regardless of how it is framed.

◈ Concluding remarks◈

Across every business model examined in this analysis, one pattern holds consistently: growth, GMV, and revenue conversion are necessary but no longer sufficient on their own to command a premium valuation.

The market has shown, repeatedly and across every business model in this set, that it will discount a growth story the moment unit economics come under visible pressure.

For any operator preparing to test public market appetite in this sector, the evidence assembled here points to a consistent standard: a credible path to durable unit economics, and contribution margins that hold up under sustained competitive pressure rather than only in a period of reduced promotional intensity, are what the market now requires before extending a premium valuation.

This is the central question that any prospectus in this space will need to address, and that investors should require a clear answer to before committing capital.