As Saudi Arabia ramped up refined product exports, chiefly jet fuel, through its Red Sea port of Yanbu in March 2026 due to the effective closure of the Strait of Hormuz, flows surged to near-record levels — with the pipeline feeding Yanbu running at full capacity.

Many of these cargoes left port without a fixed buyer or destination, available to whoever offered the best terms. It is not only Yanbu telling this story. Two tankers loaded with jet fuel from India set course for Europe, then turned back mid-voyage and headed to Asia instead — where prices had become more attractive.

In shipping, it is a common practice that a vessel loaded with energy products leaves port without a confirmed buyer or destination. While sailing, the cargo is actively sold, and the ship heads wherever the best deal is struck.

Under standard shipping contracts, the buyer can change the destination mid-voyage — a routine commercial right, not an exception. In practice, tankers slow to a near-stop or anchor in holding areas in central Mediterranean while brokers shop the cargo to the best bidder across multiple regions.

No port is to blame here. The cargo left on time. The shipping system simply sent it to wherever buyers paid most — which, in this case, was not Europe.

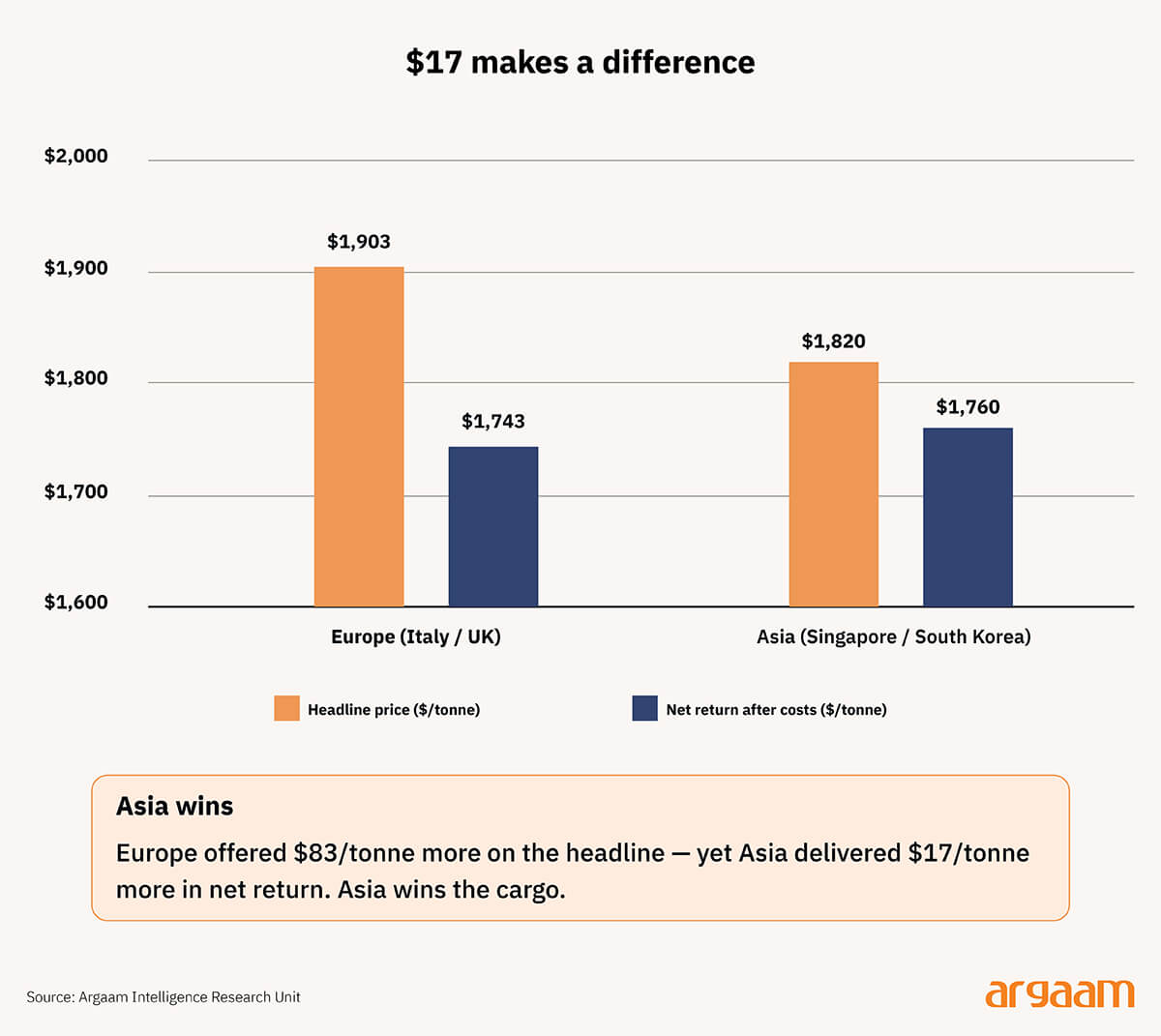

For example, on April 2, 2026, northwest Europe was paying $1,903 per tonne — a record. That sounds like an obvious destination. But jet fuel margins are not calculated on the flat price alone.

A broker compares the net return after freight costs, port dues, and discharge fees for every competing destination.

If an Asian buyer — say in Singapore or South Korea — is offering $1,820 per tonne, but the voyage to Asia costs $60 per tonne less than the voyage to a port in Italy or the UK, the Asian cargo nets $1,760 against Europe's $1,743. Asia wins, despite the lower headline price.

Europe's shortage is not currently then caused by any upstream supplier withholding fuel. It was caused by Europe's own long-standing dependence on imported jet fuel with no guaranteed priority over other markets.

Europe's jet fuel vulnerability predates the current conflict — refinery closures, soaring aviation demand, and import dependence have quietly built this exposure for years. The UK is the most exposed market, relying heavily on Gulf imports that transit the Strait of Hormuz.

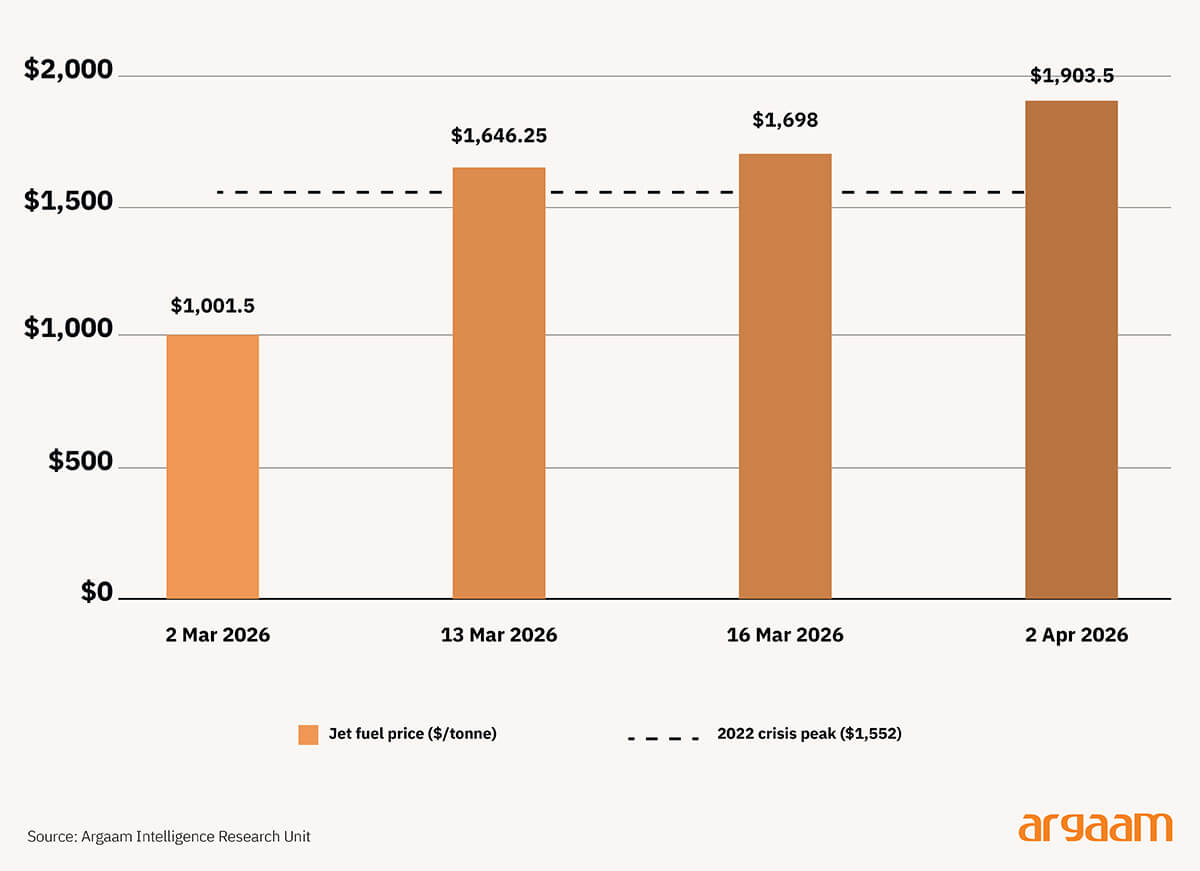

Jet fuel prices across Europe shattered multiple records within days. By mid-March 2026, prices hit $1,646 per tonne — surpassing even the 2022 energy crisis peak.

Most strikingly, jet fuel was trading at more than double the price of crude oil, a ratio that signals genuine physical shortage, not market speculation.

By mid-March 2026, jet fuel prices in northwest Europe reached their highest level ever recorded, with the gap between jet fuel and other fuel products also hitting an all-time high.

Two weeks later, on April 2, prices jumped by nearly $300 in a single day — surpassing the record set just a fortnight earlier and closing at $1,904 per tonne.

The tanker’s behaviour described in this analysis did not cause the price crisis in Europe then, but it made it worse and longer. The underlying cause is straightforward: the effective closure of the Strait of Hormuz removed a significant volume of jet fuel from the global market. That is the root shock.

What made a bad situation worse was that Europe could not count on any of the fuel that was already at sea. Ships had left port loaded with jet fuel, but none of it was guaranteed to arrive in Europe. It could go anywhere.

In a normal market, a cargo leaving Yanbu heading to Rotterdam is, for practical purposes, Europe's cargo. In a 'for orders' market, it belongs to whoever pays most when the ship reaches its decision point — which may not be Europe.

This matters because Europe has spent the past decade dismantling much of its domestic refining capacity.

That decision made economic sense when Gulf supply was reliable and committed. It makes far less sense when Gulf cargoes are simultaneously scarce due to the severe geopolitical tensions.

When that lock-in does not exist — and the 'for orders' model is specifically designed to prevent it — European buyers cannot tell the difference between a cargo that will arrive and one that will not.

Europe needs fuel that is not just produced and shipped, but formally promised to European buyers before it goes up for sale to the rest of the world. Without that promise, Europe competes for every cargo on equal terms with Asia, and in a crisis, it can lose.

In a well-supplied market, that uncertainty is a minor inconvenience. In a market already pricing in a massive supply shock, it becomes a second crisis layered on top of the first.

Buyers pay a premium not just for fuel, but for the guarantee of delivery — and in an uncommitted spot market, that guarantee does not exist. That is why prices reached levels that the physical shortage alone cannot fully explain.

The policy lesson is structural: import dependence is manageable. Commitment dependence — relying on foreign cargoes to voluntarily prioritise your market in a crisis — is a strategic vulnerability of a different order entirely.