This analysis is not mainly about food inflation in general. It is about what happens when the price gap between a national brand and a supermarket’s own label starts to narrow during a supply shock.

That question matters because a war shock raises costs on both sides of the shelf at the same time. Brent crude rose over to $100 a barrel as the Iran-Israeli-US conflict escalated, and that disruption around the Strait of Hormuz was also pushing urea and ammonia prices up by roughly 30% to 40%.

Those pressures feed into fuel, freight, packaging, and food inputs, so both branded and private-label staples become more expensive.

For low-income households in the Arabian Gulf and the Middle East in general, the key issue is not simply whether one product becomes more expensive, but whether the supermarket’s own version remains meaningfully cheaper than the branded one.

That gap is a quiet budget buffer. When it compresses, the safety net becomes thinner. A private label is a product made by a manufacturer but sold under the retailer’s own brand; it is usually cheaper because it carries lower brand, advertising, packaging, and distribution costs.

The economics literature treats this gap as more than a retail curiosity. Work on private-label competition argues that the relationship between national-brand and store-brand prices is shaped by retailer power, competitive interaction, and cost conditions rather than by chance alone.

This paper therefore asks a narrower and more practical question: under what conditions does that gap compress in a Gulf country like the UAE, and what is the most fiscally efficient way to preserve it? In short, the key welfare variable in a retail supply shock is not the level of prices alone, but the survival of the private-label discount.

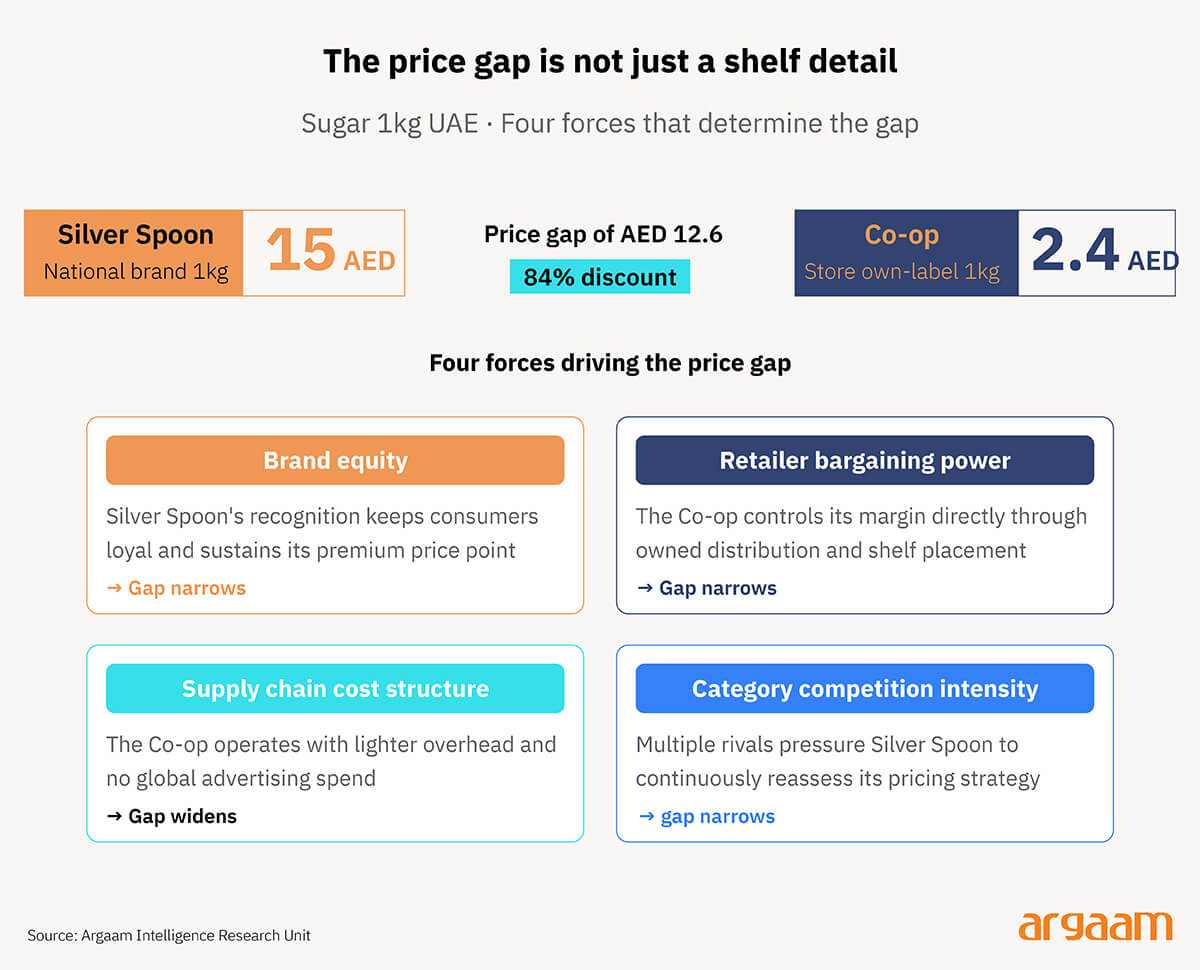

The Distance Between Two Prices Is Not Accidental

The price gap between a national brand and a private label is not just a shelf detail. It is an economic variable shaped by market structure.

That gap reflects at least four forces working together: retailer bargaining power, the brand premium that national manufacturers can sustain, the cost structure of the supply chain, and the intensity of competition inside the category. When those forces change, the gap changes too.

A supply shock, therefore, does not just raise prices in general; it can also alter the relative distance between branded and private-label products, which is what matters for household substitution.

The entry and pricing of private labels affect the competitive equilibrium itself, rather than simply adding a cheaper product to the shelf.

Private-label competition can change how brands price, which means the gap between the two is structurally determined, not accidental.

The UAE Shelf as Economic Indicator

The economics of private labels shows that private labels influence retailer-manufacturer bargaining, pricing strategies, and market outcomes across the category.

That matters because the price gap can be treated as a welfare-relevant indicator: when it narrows, the consumer’s option to trade down becomes weaker. That is why the next step is not simply to compare prices, but to measure the gap directly through a Price Gap Index.

The UAE is a useful case study in our analysis because it combines high food import dependence with a mature modern retail system in which private labels and national brands are sold side by side, making the price gap directly observable.

The three staples used here are: wheat flour, which is tightly linked to imported wheat; cooking oil, which is sensitive to imported raw materials, freight and energy; and rice, a core staple with strong import dependence and visible brand/private-label comparators on UAE supermarket shelves.

To measure whether the private-label advantage is holding up, this paper uses a simple Price Gap Index, defined as:

◆ Price Gap Index = private-label price / national-brand price

A lower ratio means a wider discount and a stronger consumer buffer. This is more informative than the absolute price difference alone.

If a branded item rises from AED 28 to AED 34 while the private label rises from AED 16 to AED 22, the dirham gap stays at AED 12, but the ratio changes from 0.57 to 0.65.

In other words, the cheaper option is still cheaper, but it is no longer as good a bargain as before. That is the economic meaning of gap compression.

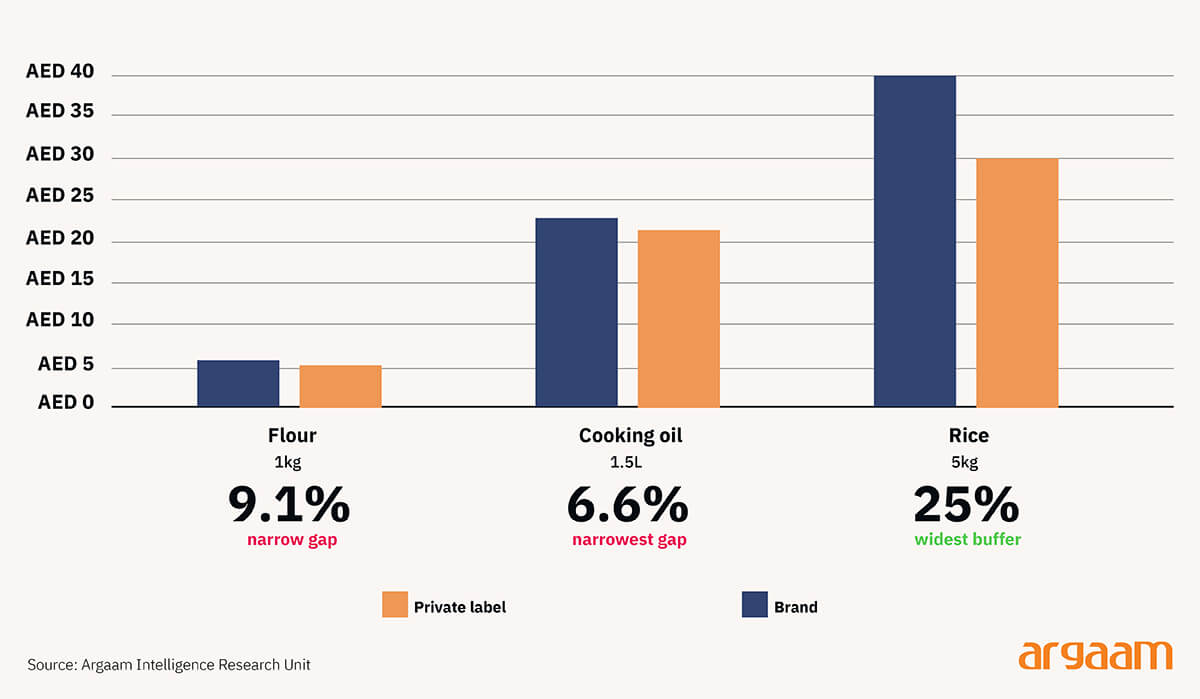

Current Carrefour UAE prices already show that this buffer varies sharply across staples. For flour, Carrefour Chakki Fresh Atta 1kg is listed at AED 4.99, while Al Baker All Purpose Flour 1kg is AED 5.49, giving a Price Gap Index of 0.91 and a discount of only 9.1%.

For cooking oil, Carrefour Cooking and Frying Oil 1.5L is AED 21.29, while Afia Pure Sunflower Oil 1.5L is AED 22.79, implying an index of 0.93 and a discount of just 6.6%.

Rice still offers a wider buffer: Carrefour 1121 XXL Extra Long Grain Basmati Rice 5kg is AED 29.99, while Tilda XXL Extra Long Grand Basmati Rice 5kg is AED 39.99, which gives an index of 0.75 and a discount of about 25%.

The point is not that all private-label products are losing their advantage equally. It is that the safety margin is already thin in some categories, especially flour and cooking oil.

Once a supply shock pushes input, freight or handling costs higher, those categories have much less room before the household’s trade-down option starts to weaken materially.

This is why our analysis moved from “food prices are rising”to the narrower question of which price gaps are most vulnerable to compression, and how much it would cost to preserve them.

Not Everyone Feels the Gap the Same Way

Gap compression does not affect all households equally. When the price difference between a branded product and a store-own alternative narrows, the households that feel it most are those already spending a large share of their income on food.

For these families, trading down to the cheaper option is not a preference — it is a strategy. When that strategy becomes less effective, because the saving has shrunk, their real exposure to rising food prices increases.

This is why the gap should be read as a welfare indicator, not simply a retail pricing outcome. The smaller the discount on the store-own product, the less room lower-income households have to absorb a price shock without cutting consumption.

And cutting consumption of basic food staples carries a welfare cost that falls unevenly — concentrated precisely among those with the least capacity to absorb it.

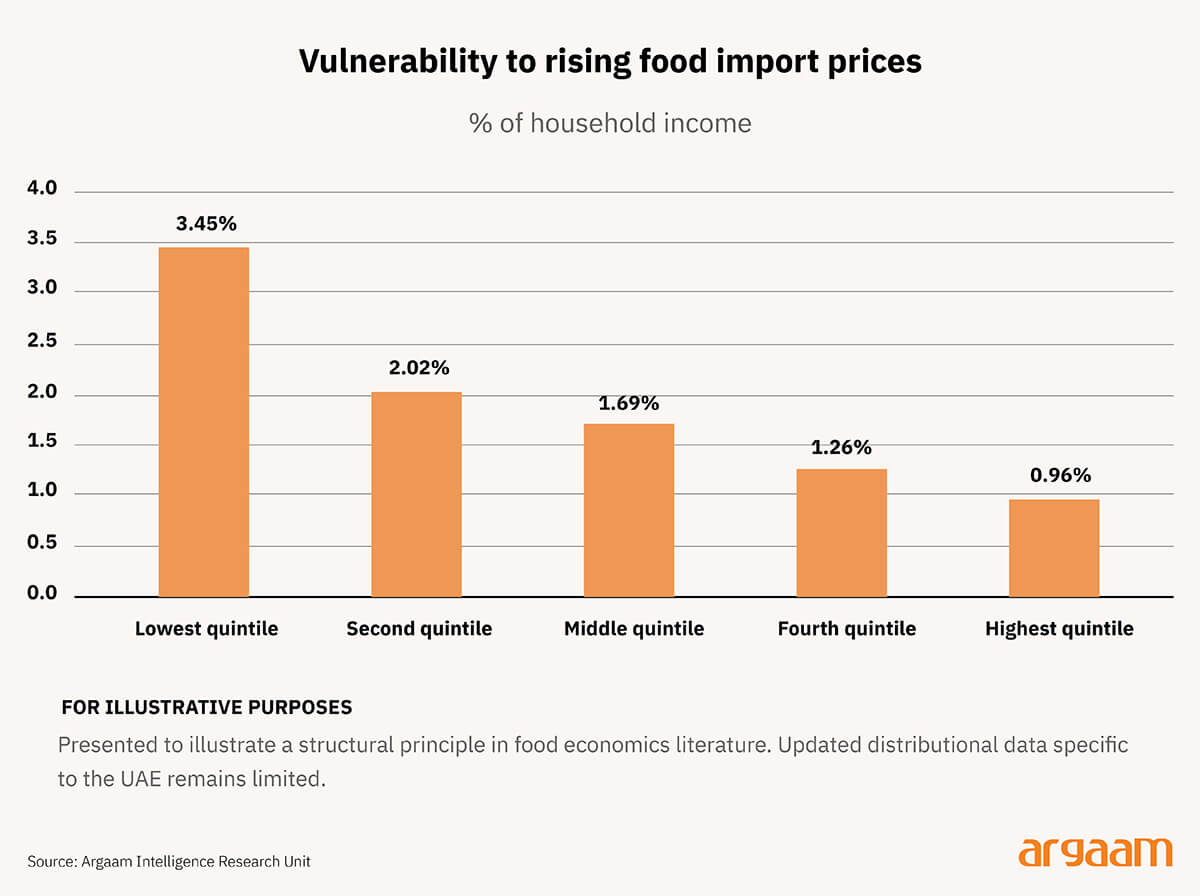

For the UAE, reliable research about vulnerability to rising food import prices in the UAE finds that households in the lowest income quintile are 3.5 times more vulnerable than those in the highest quintile.

So, If the private-label discount narrows in staples such as flour, cooking oil, and rice, the loss is not just a smaller bargain on the shelf. It is a larger effective income shock for the households least able to absorb it.

Data are drawn from a World Bank policy research paper and are used here just to illustrate a structural principle well established in the food economics literature, not as a current measurement of UAE conditions.

Updated distributional data specific to the UAE remains limited in availability. The underlying relationship the chart captures — that lower-income households absorb a disproportionately larger share of food import price shocks — is a finding that has been replicated consistently across comparable economies.

Efficient Government Intervention Starts With the Right Metric

The next question is not whether governments should intervene, but how to do so efficiently. For this analysis, the most useful metric is Intervention Cost-per-Gap-Point: the fiscal cost required to preserve one percentage point of the private-label discount during a supply shock.

A government can try to protect households through blunt price controls, through direct cash support, or through supply-side relief that helps retailers keep private-label prices from rising too quickly.

The economically relevant question is which option preserves the discount most cheaply and with the least distortion. Cost increases often move through supply chains faster than cost relief does, so policy efficiency depends on how quickly support reaches the shelf.

In the UAE case, that logic points away from broad tariff policy as the main instrument for flour and rice. The UAE already maintains zero import tariffs on wheat grain and wheat flour, and the tariff schedule also lists rice at 0%.

That means the fiscally relevant margin is more likely to be customs speed, handling costs, clearance frictions, and logistics continuity than a headline duty waiver on those two staples.

In other words, a government in the Arabian Gulf in general should not ask how to lower all food prices in general. It should ask how to preserve the private-label discount at the lowest pass-through cost.

Dubai Customs, for example, offered a clear precedent during COVID when it introduced fast-track clearance and release procedures for food and critical medical supplies while keeping physical inspections to a minimum.

This kind of measure does not force retailers to sell below cost. Instead, it lowers the cost of maintaining supply and gives them more room to hold the private-label line.

◆ Here is a plainer version:

Any government support of this kind needs to be carefully bounded. It should cover only a short list of essential staples, last only as long as the supply shock lasts, and apply across several retailers rather than just one.

Without these limits, a policy designed to help households ends up benefiting a single retailer more than the people it was meant to protect.

The more effective approach is not to fix the shelf price directly, but to address whatever is pushing that price up in the first place — whether that is freight costs, import duties, or supply chain bottlenecks. Intervening at those points is usually cheaper and less likely to distort the market in the long run.

The goal is to keep the price gap meaningful for households during a crisis. It is not to hand any one retailer a permanent advantage once the crisis has passed. |