The war with Iran is doing something beyond disrupting supply chains and pushing up oil prices. It is forcing investors and businesses to fundamentally reassess where it is safe to deploy capital, how quickly that capital can be moved if conditions deteriorate, and whether the legal and political frameworks protecting it will hold under pressure.

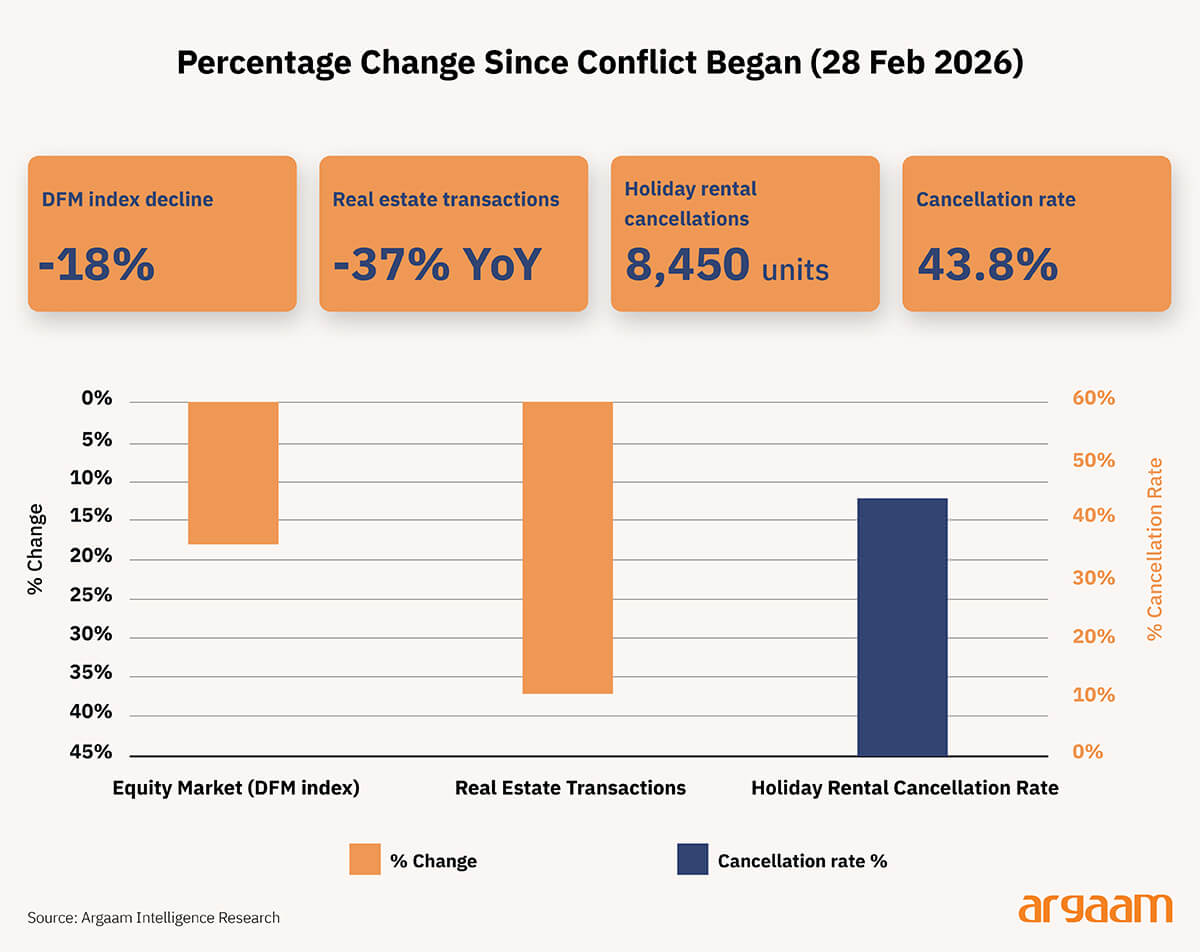

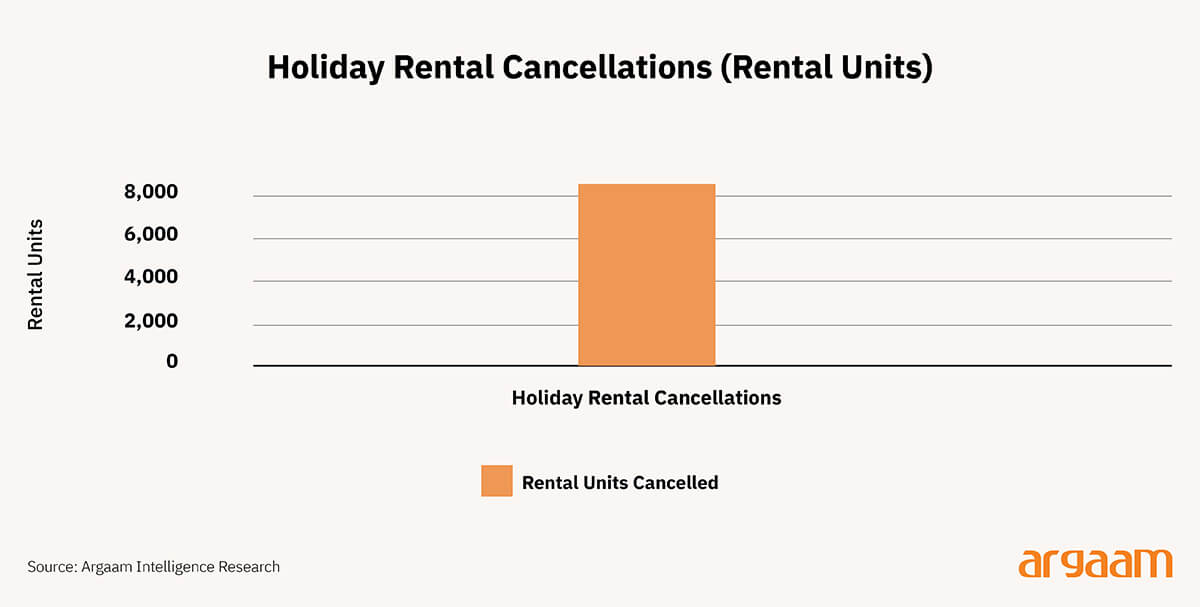

In the Arabian Gulf, this shift is already visible: equity markets have fallen sharply, with Dubai’s main index down more than 18% since the conflict began on February 28, while real estate transactions dropped 37% year-on-year in early March.

At the same time, investors have started reallocating assets across jurisdictions, with some moving funds from Dubai to Singapore amid rising geopolitical uncertainty.

Yet this is not merely a story of capital leaving risk. It is a story of where it goes instead. The war is accelerating an existing shift: mobile, digital-native capital is increasingly flowing toward jurisdictions that offer regulatory clarity and legal certainty, rather than physical safety alone.

This raises a central question: does the disruption of Dubai’s physical economy paradoxically strengthen its case as a digital asset capital markets hub—and is its regulatory infrastructure ready to capture that shift?

Unlike tourism, logistics, or real estate, Dubai’s crypto sector remained largely functional because many firms are cloud-based, virtual-first, and able to operate remotely. Core regulatory functions also continued to run.

How Dubai Is Assembling the Only Complete Crypto Credit Framework in the Region

Dubai's edge in the crypto space is not just a welcoming attitude toward digital assets. It is that over the past few years it has built a regulatory structure that is genuinely suited to how crypto credit markets actually work.

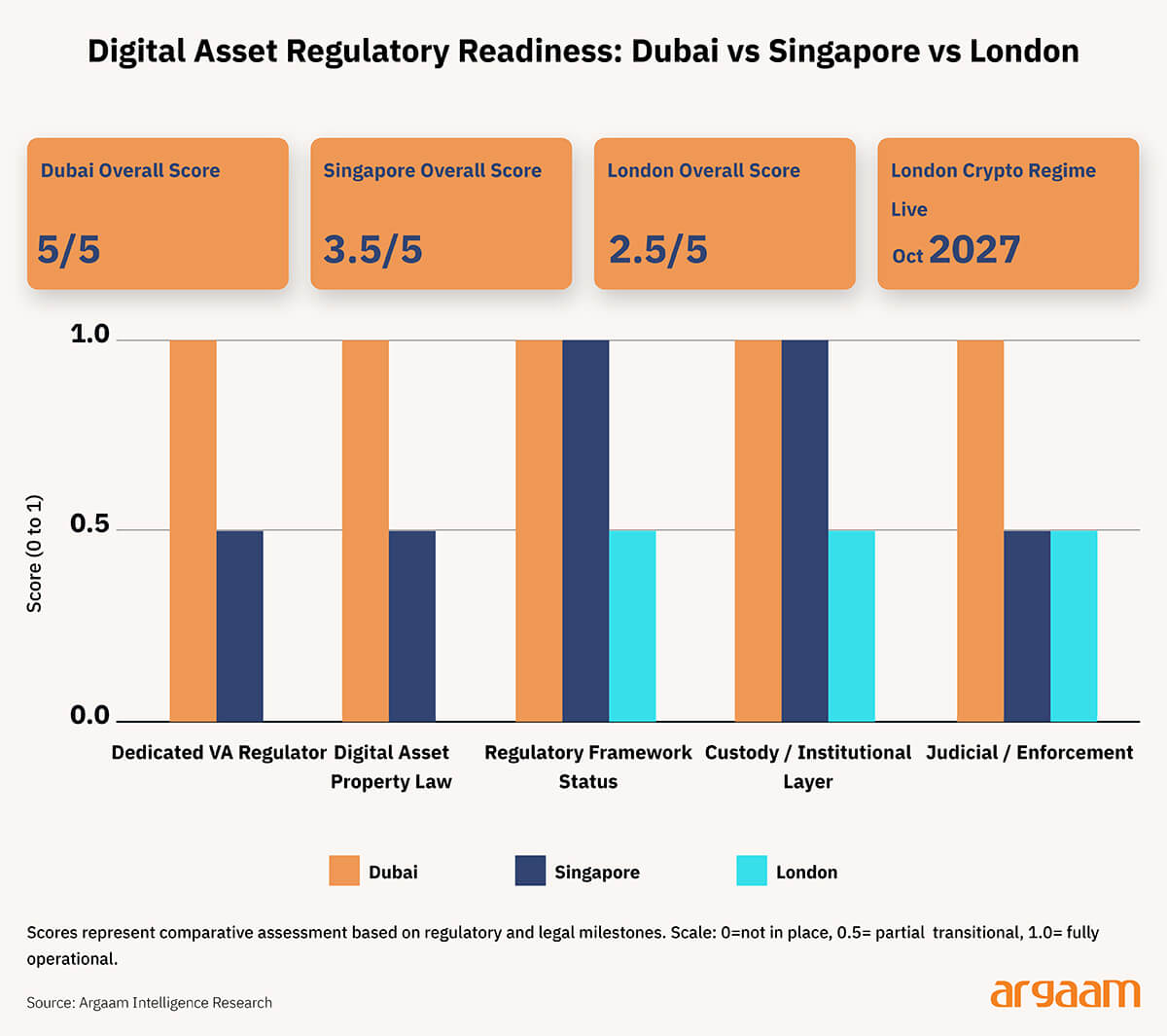

At the centre of that structure is VARA — the Virtual Assets Regulatory Authority — which oversees crypto activity across Dubai's mainland and its free zones, with the exception of the DIFC which has its own separate regime.

What makes VARA significant is that its 2023 framework was built specifically for digital assets from the ground up, rather than retrofitting old securities laws to cover something they were never designed for. That distinction matters more than it sounds.

DAT — short for digital asset transactions, meaning any financial activity where the underlying asset is a cryptocurrency or token — involves instruments, risks, and market participants that simply do not map cleanly onto traditional finance.

When a company borrows against its Bitcoin holdings, or issues a convertible note backed by crypto collateral, the regulator overseeing that transaction needs to already understand what Bitcoin collateral is, how liquidation works in a volatile digital market, and what the intermediaries involved actually do. A regulator applying adapted securities rules is always one step behind.

VARA was designed to be one step ahead. For digital capital, the central question is not "is the city safe" but "is the jurisdiction legible and enforceable?"

Dubai's Bet on Regulatory Alignment with International Standards

Digital capital moves faster than any single regulator can track. That makes governance more important, not less — but it also changes what good governance means. The question is no longer whether a jurisdiction has rules, but whether those rules are recognised and enforceable beyond its own borders.

Corporate Bitcoin strategy has moved well past the point of simply buying and holding. Companies are now using their Bitcoin holdings as the basis for more sophisticated financing — issuing convertible bonds, preferred shares, and structured debt that treats Bitcoin as collateral rather than just a balance sheet asset.

By June 2025, at least 61 listed companies worldwide had adopted some form of Bitcoin treasury strategy. But the more significant shift is qualitative, not quantitative. Strategy, the most advanced example, moved beyond equity raises into convertibles and then preferred stock — essentially building a capital markets operation around its Bitcoin position.

The question the market is now asking is not just which companies hold Bitcoin, but which ones can borrow against it, structure around it, and create yield from it. That is a fundamentally different and more mature phase of institutional adoption.

In Dubai, the more important layer is DIFC’s legal architecture. DIFC’s Digital Assets Law No. 2 of 2024 gives digital assets a property-law footing and sets out how they may be controlled, transferred, and dealt with.

For a DAT market, that is not a technical detail. If Bitcoin is used as collateral, or if repayment terms are linked to its price, the transaction depends on clear rules over control, security interests, and enforcement. In other words, Dubai is not only making trading easier; it is making digital assets more usable inside credit documentation.

That legal base is reinforced by the institutional regulatory layer inside DIFC. The DFSA’s updated Crypto Token regime, effective from 12 January 2026, strengthened rules around token suitability, market integrity, investor protection, and operational clarity for firms in the centre.

This is important because DAT credit does not sit neatly inside “crypto” or “traditional finance.” It requires custody, advisory, and asset-management functions that can connect both worlds. Dubai’s edge is that these functions are beginning to sit inside one regulatory ecosystem rather than across disconnected ones.

Finally, DIFC Courts’Digital Economy Court adds something many jurisdictions still lack: a visible dispute-resolution channel for digital-economy cases. That does not guarantee market dominance, but it does improve credibility.

For DAT credit, the key issue is no longer access to crypto alone, but whether claims on it can be documented, protected, and enforced. Dubai is becoming one of the few places where the regulatory, legal, and judicial pieces are starting to align around that problem.

In other words, the bottleneck is increasingly institutional rather than technological.

You Don't Need to Be in Dubai to Use Dubai Law

A fund manager in Singapore or a family office in Zurich does not need to be physically present in Dubai to benefit from what Dubai has built in its crypto market as long as they have a registered entity in Dubai.

What they need is a jurisdiction whose legal definitions, documentation standards, custody frameworks, and courts they can rely on from anywhere — and that is precisely what Dubai's regulatory architecture is designed to provide.

This is where the alignment with international standards becomes commercially significant. Dubai's legal framework for digital assets draws from English common law principles, its regulatory approach mirrors the IMF and FSB frameworks for crypto oversight.

And its custody and conduct standards are increasingly legible to institutional counterparties in London, Singapore, and New York. That mutual legibility is what transforms a local framework into a globally usable one.

In a conflict environment, capital does not stop moving — it moves more selectively. Investors caught between a disrupted Gulf and an uncertain global order are not looking for physical safety alone. They are looking for jurisdictions that can define what they own, protect how they hold it, and enforce what they are owed.

Dubai is building precisely that case — and its regulatory alignment with international standards is what makes the argument credible beyond the region. Dubai is moving earlier than London whose dedicated crypto regime is only expected to come into force on 25 October 2027.

That leaves the UK in a transitional phase: credible, but not yet fully operational for this market. Singapore is more advanced in implementation, yet its 2025 DTSP regime has been notably selective and conservative, especially for offshore-facing firms and retail-related risk.

MAS has also prohibited digital payment token service providers from offering credit or leverage to retail customers, reinforcing its prudential bias.

Dubai has a real but narrow window of opportunity. It is not yet the dominant venue for crypto credit — but it may be the most execution-ready jurisdiction for deal structures serving the Gulf, Asia, and Africa, regions that New York and London have historically underserved.

The framework is credible.

The harder question is whether Dubai can convert regulatory advantage into actual market activity. That requires more than good rules. It needs deep liquidity, specialist law firms that understand crypto credit, structuring banks, reliable custody infrastructure, and enough institutional trust for counterparties to actually use Dubai law and Dubai courts when it matters.

Cross-border enforceability is also unresolved — crypto credit will not stay local, and Dubai's framework needs to work beyond its own borders to be genuinely useful.

Being first in regulation does not guarantee becoming the dominant hub. Dubai has the design right. Whether it can build the market around it is the open question.

Concluding remarks:

The technology for crypto credit already exists. What is missing is not the blockchain or the smart contract — it is the institutional infrastructure around it: regulated custodians that major banks will trust, legal opinions that hold up in court, and credit documentation that international lenders will sign.

Dubai's regulatory build-out is directly targeting this bottleneck, which is why its ambition is credible in a way that most crypto-friendly jurisdictions are not.