The dairy industry in Saudi Arabia has historically been centered around livestock farming, with production heavily dependent on land, water, and challenging climate conditions.

In recent years, the country has increasingly turned to technological innovations but still to better manage these biological cycles, to enhance efficiency and sustainability in milk production.

This analysis by Argaam Intelligence raises a novel manufacturing technique that allows for the cost-effective production of high-quality milk proteins within controlled laboratory or industrial facilities, significantly reducing operational expenses and capital costs by bypassing the resource-intensive processes and capital investments traditionally required for livestock farming.

This shift is often misunderstood as another form of“alternative milk,” similar to soy or oat-based products. In reality, lab-grown milk protein targets the core functional inputs of the dairy industry.

By producing proteins that are chemically identical to those found in cow’s milk, this approach does not aim to change consumer preferences, but to replace how dairy ingredients are supplied to manufacturers, foodservice operators, and processors.

If production costs reach parity with traditional dairy inputs, the implications extend far beyond niche products on supermarket shelves.

The transition would represent a move from an agricultural supply chain to a manufacturing-led one—reshaping cost structures, supply reliability, and procurement logic across the dairy sector in the kingdom.

For markets such as Saudi Arabia, where dairy self-sufficiency has been achieved at a high structural cost, this novel model raises important questions about efficiency, resilience, and long-term capital allocation.

ℹ︎

Bybassing the cow milk

● Minimising reliance on costly variables such as feed, water, land, and labor ● Decreasing then marginal costs per unit ● The cost of producing each additional unit often decreases, while production increases ● Competitive pricing strategies ● Capturing market share from conventional dairy products

Saudi Arabia has built a highly industrialised dairy sector, dominated by large, vertically integrated producers with modern farms, processing capacity, and national cold-chain distribution.

Note Vertical integration in the dairy sector refers to a business model where a single company controls multiple stages of the supply chain, from production to processing and distribution. Cold-chain distribution is a logistics system that maintains perishable products like dairy at controlled, refrigerated temperatures throughout the entire supply chain.

The size of Saudi Arabia’s dairy sector is quite large; for example, Almarai reported having over 166,000 cows by the end of 2024, showing that the country has moved well beyond relying on small farms or individual farmers. Overall, Saudi Arabia’s food security data indicates that the country has a plentiful and sufficient supply of dairy products.

ℹ︎

Why aren’t dairy products measured in liters?

Natural milk contains more than 90% water, while its actual economic value lies in the functional proteins used in producing cheese, infant formula, and processed foods.

Therefore, this analysis does not rely on comparing liquid milk prices, but rather on the cost per industrially usable gram of milk protein, which is the true unit of measurement within B2B food supply chains.

The Economic Dynamics of Saudi Dairy Production

GASTAT’s Food Security Statistics reported a 131% self-sufficiency ratio for dairy products. Implying domestic production capacity can exceed domestic demand for some categories.

But this output is produced under a cost structure shaped by environmental constraints rather than farming economics. Water scarcity is a central pressure point.

For example in 2018, the kingdom moved to restrict water-intensive fodder cultivation. Argaam cited official sources indicating green fodder crops consumed ~17 billion m³ of water annually, with ~9 billion m³ expected to be saved after the ban took effect, while the same policy discussion pointed to increased reliance on imported fodder to fill the gap.

Feed dependence matters because it introduces commodity price volatility into farm-gate milk costs.

Note "farm-gate" refers to the price or value of agricultural products, such as milk, at the point of leaving the farm, before any processing, transportation, or retail markups. It represents the price that farmers receive directly from buyers for their raw products.

In 2025, Saudi Arabia's livestock fodder imports were projected for barley to reach around 4 million tonnes (MMT) and corn potentially reaching 4.9 MMT.

Climate is the other structural driver. High temperatures reduce milk productivity and force farms to invest continuously in heat-mitigation systems (cooling, ventilation, water use, and electricity).

Empirical studies in arid environments show that cooling systems can materially affect cow performance, but also require significant inputs of resources, chiefly water and energy.

Saudi Arabia’s dairy sector is operationally advanced and capable of scaling up, but its profitability depends on water policies, reliance on imported feed, and the costs of managing heat—challenges that are difficult to eliminate or reduce within the current agricultural production system.

ℹ︎

Rethinking farm economics

● Investing in biotechnology versus traditional investment in heat-mitigation systems ● Sustainability will not longer depend on geopolitical and market fluctuations ● Biological cycles will no longer be a cost multiplier

The key point is lab-grown milk protein follows a different cost structure. Traditional dairy is anchored in livestock farming, where costs are driven by biological and environmental variables that are hard to control.

Feed is typically the single largest variable cost. Industry data suggests feed can account for ~70% of variable costs on dairy farms, making farm-gate economics highly exposed to global commodity prices.

In Saudi Arabia, this exposure is structurally amplified because water constraints have pushed the sector toward imported feed.

ℹ︎

Pressure Test

Unit costs in the dairy sector are shaped by: ● Climate stress ● Feed-market volatility ● More time for biological processes

The Economics of Lab-Grown Milk

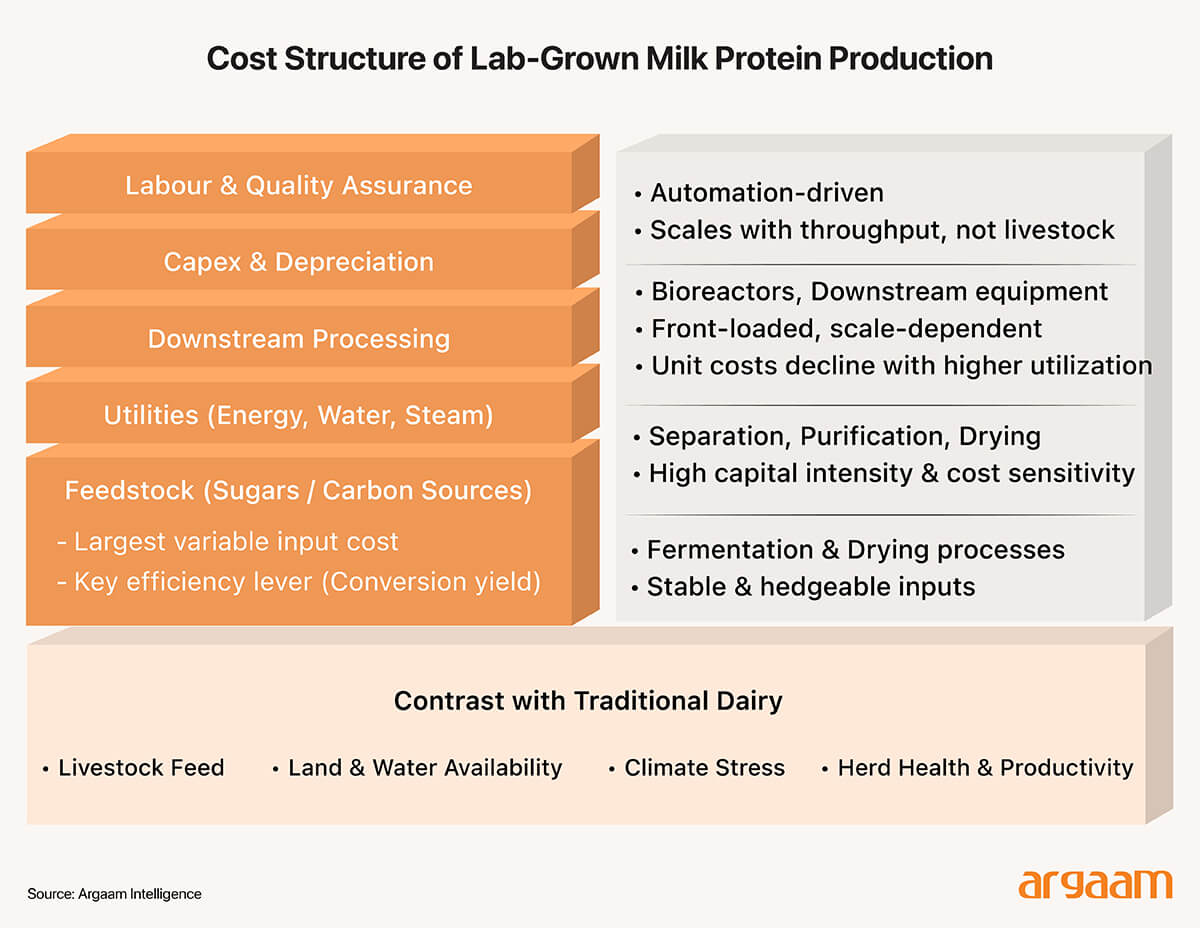

In a manufacturing-based model, the cost structure of lab-grown milk protein is driven by a limited number of clearly defined inputs. Feedstock, typically sugars or other carbon sources, represents a direct variable cost and one of the most important levers for achieving cost parity.

Industry analyses consistently highlight improvements in conversion efficiency—how effectively feedstock is turned into target protein—as central to long-term cost reduction.

Utility costs, including energy, water, and steam, are primarily determined by fermentation conditions and downstream drying processes. While these inputs are not negligible, they tend to be more stable and predictable than the climate- and feed-driven shocks that affect livestock-based dairy production, and can be partially managed through procurement strategies and energy hedging.

Downstream processing—covering separation, purification, and drying of milk proteins—is widely recognised as the most capital- and cost-intensive stage of precision fermentation.

At industrial scale, it also represents the main source of uncertainty, as purification requirements directly influence both operating costs and facility design.

Capital expenditure, concentrated in bioreactors and downstream equipment, is front-loaded but inherently scalable. As utilisation rates increase and facilities operate closer to capacity, depreciation per unit declines.

Depreciation per unit declines because when a facility is used more, the total depreciation cost is spread over a larger number of products. So, the more products you make with the same depreciation cost, the lower the depreciation cost is for each individual unit.

Labour and quality assurance costs are typically more automated and standardised than in animal-based dairy production. Rather than being tied to herd size and animal care, these costs scale primarily with throughput and production volume, reinforcing the manufacturing character of the system.

This is where scale effects become structurally different. In farming, scaling output does not remove exposure to feed price cycles, heat stress, and herd health risks.

In manufacturing, scale and learning effects can compound: larger vessels, higher utilisation, yield improvements, and incremental process optimisation can push costs down over time.

Good Food Iinstitute’s techno-economic synthesis highlights feedstock costs, feedstock conversion, and capital efficiency as central levers for cost reduction across fermentation-derived ingredients.

In other words, fermentation-derived dairy has the potential to be cost-competitive with conventional dairy, especially at scale, by leveraging technological efficiencies and reduced resource inputs, thereby supporting its economic viability as a sustainable alternative. The risk profile also shifts.

Dairy farming carries inherent biological and seasonal volatility; precision fermentation turns supply reliability into an operations and quality-control problem.

That matters for B2B buyers: it improves price predictability, reduces the need for buffer inventory, and makes delivery schedules more contractable.

In other words, the competition is less “natural vs alternative” and more “agricultural volatility vs manufacturing control.” If cost parity is reached, the manufacturing model offers not just lower expected unit costs, but a more manageable risk structure for processors and foodservice customers.

ℹ︎

Natural farming: Pressure test

● Variability in milk yield and quality due to biological factors ● Supply inconsistency due to seasonal factors ● Unpredictable disruptions to herd productivity ● Fluctuations in milk prices driven by supply-demand imbalances

Profits Near Major Dairy Giants

Saudi Arabia’s dairy market is not small. The market at USD 6.04bn (2025), rising to USD 7.58bn by 2031 (3.85% CAGR), according to independent forecasts.

Importantly, the market for dairy alternatives in Saudi is still tiny (USD 61.1m in 2025), which supports the view that near-term value is less about retail shelf disruption and more about ingredient substitution inside the existing dairy/food system.

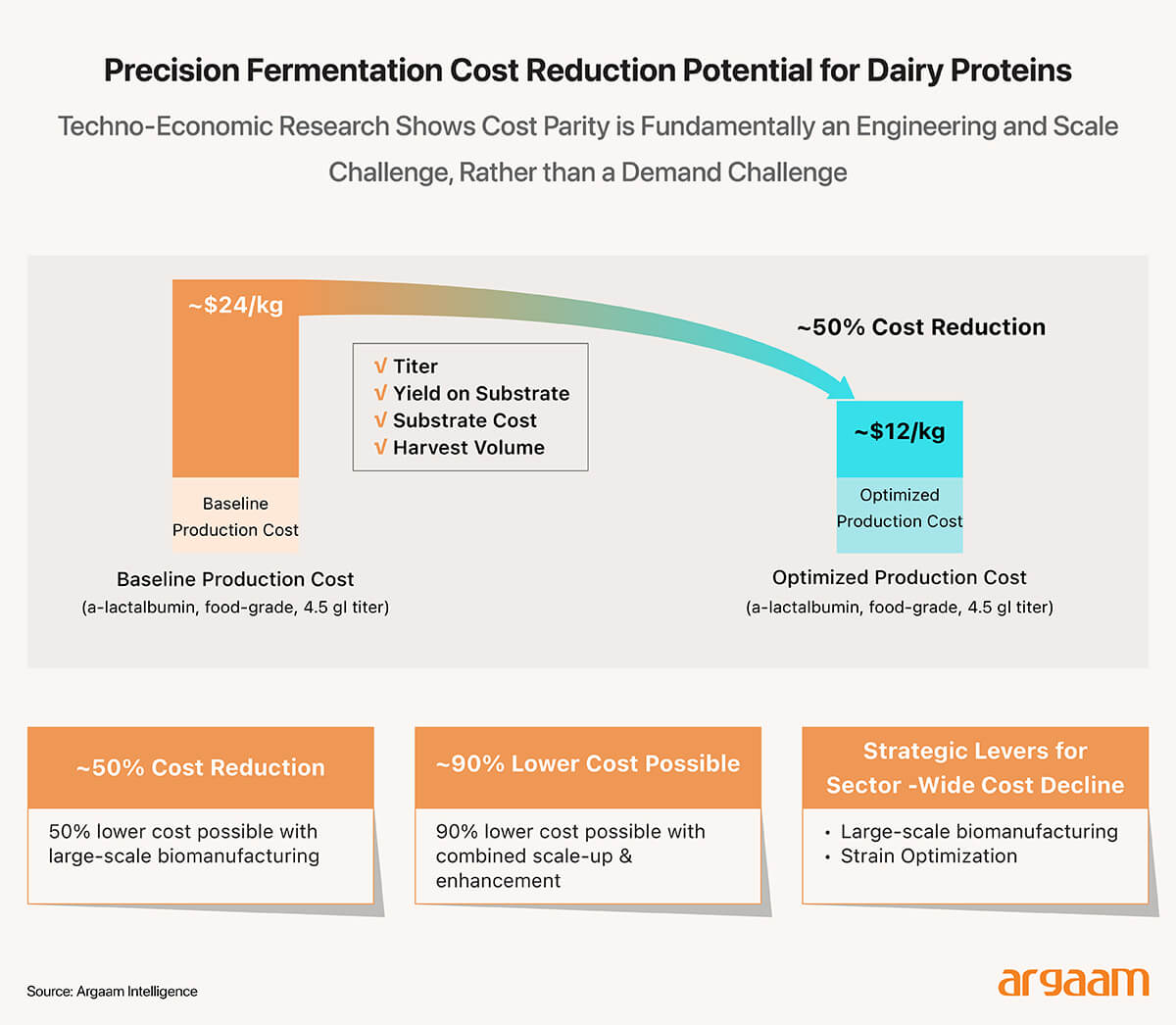

Recent studies on production costs suggest that reaching price competitiveness for fermentation-derived dairy depends mainly on engineering and scaling up the process, rather than consumer demand.

One case study estimates that producing food-grade fermentation dairy currently costs about $24 per kilogram.

But with improvements in four key areas—amount of product produced per unit of bacteria (titre), how efficiently the bacteria convert the substrate into the desired product (yield), the cost of the raw materials (substrate), and the total amount that can be harvested—the cost could drop to around $12 per kilogram.

Additionally, building large, optimized manufacturing plants can potentially reduce costs by about 50% using current techniques, and potentially by up to 90% if both scale and biological improvements are combined.

This shows that there is a huge potential for costs to come down as technology and production methods improve over time.

The price of regular dairy proteins like casein varies a lot worldwide, with prices in 2024 ranging roughly from $11.40 to $44.10 per kilogram (because of market ups and downs).

If a new, precise fermentation process can produce milk proteins at around $12 per kilogram and sell them for $15 to $20 per kilogram (depending on how they are used), it would give a profit (or gross margin) of about 20% to 40% before subtracting other expenses like selling and administrative costs.

This is similar to the profit margins of major dairy companies in Saudi Arabia, like Almarai, which had a gross margin of about 31.8% in 2024.

Note The $12/kg cost pertains to isolated milk proteins (like casein and whey), which are valuable ingredients in various processed foods, rather than the entire milk commodity.

Whole cow’s milk includes water, fats, lactose, and other components, making it much cheaper (around $1.50/kg or less).

Milk proteins are high-value ingredients used in specialty foods, infant formulas, sports nutrition, and pharmaceuticals. Their market price can be significantly higher, making fermentation-derived protein economically viable when sold as an ingredient.

ℹ︎

Cost Target: $12 per kilogram

● Reaching this cost level does not assume government subsidies or price protection; it relies on operational efficiency and large scale industrial discipline. ● Cost reduction is achieved by improving microbial process productivity, increasing extraction yields, and spreading fixed costs over greater production volumes. ● Competitiveness in this model is driven by manufacturing structure and scalability, rather than demand growth or shifts in consumer preferences. ● At this cost point, industrially produced protein becomes competitive as a B2B ingredient within existing supply chains.

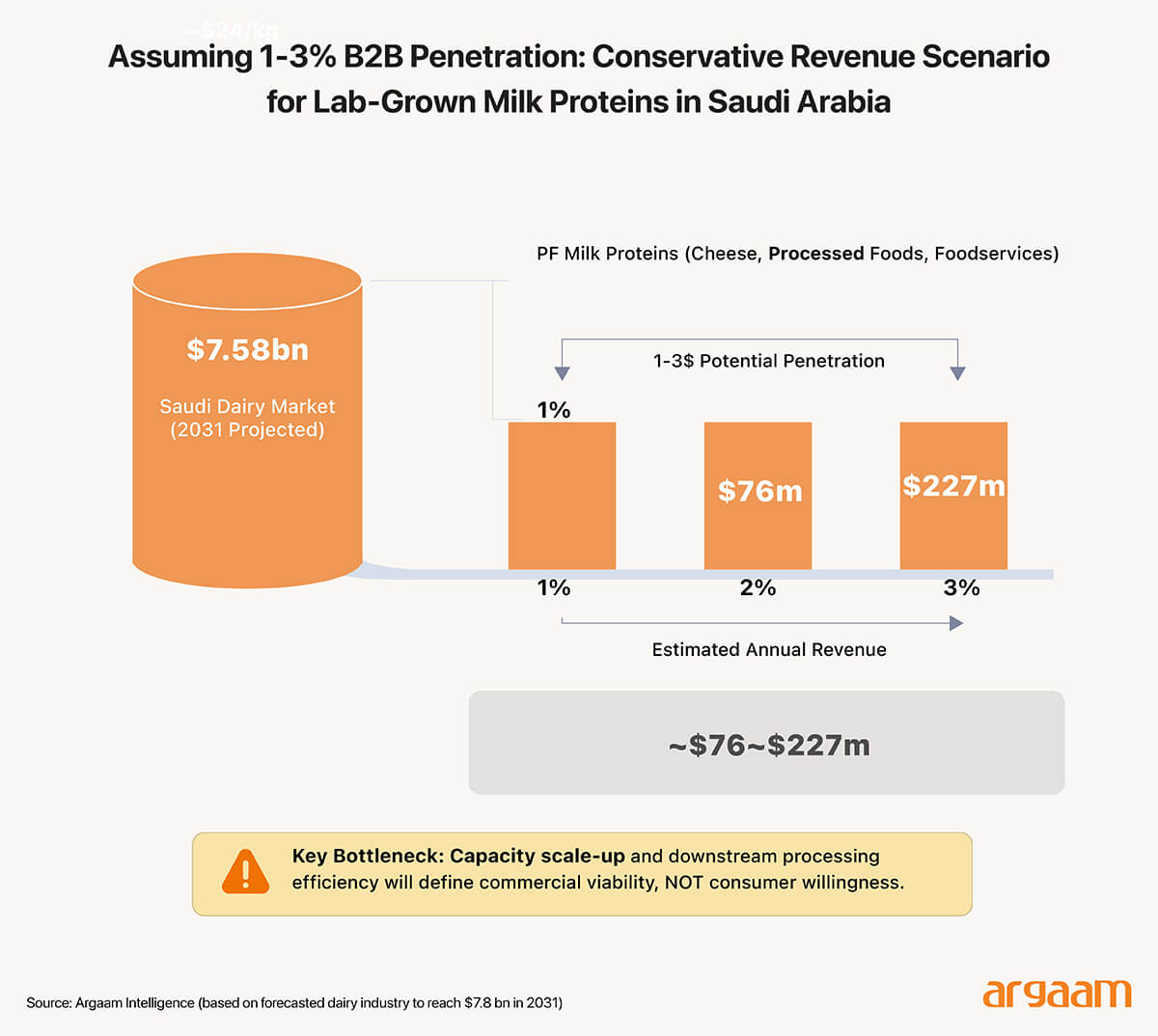

If fermentation-produced milk proteins manage to capture just 1–3% of the Saudi dairy market by 2031 (based on the forecast that the dairy market will reach $ 7.58bn by 2031)—mainly by being used as ingredients in cheese, foodservice, or processed foods—it would mean earning about $76 million to $227 million each year.

However, the biggest challenge isn’t whether people want to buy it; instead, it’s whether companies can produce enough of the product efficiently and improve the processes used after production. These are the main costs that need to be managed as production scales up.

Concluding Thought:

The most realistic way to introduce fermentation-derived dairy products is to focus on selling ingredients directly to food companies, rather than directly to consumers.

This approach is similar to how vegetable cream became popular: food manufacturers and restaurant operators used it because it was stable, worked well in recipes, and was affordable, with consumers not noticing much.

Lab-grown milk proteins work even better with this strategy because they perform just like natural dairy proteins in cooking and processing.

This means companies can buy them based on their functional properties—like how they behave in making cheese, sauces, baked goods, or ready-made meals—without needing to change their branding or marketing directly to consumers.

For everyday liquid milk, it will be harder to break into the market until large-scale production makes costs comparable to traditional milk.

More this Weekend

The 90+ Barrier: Unlocking Saudi Profit in a Tough New Video Game Market

Analyzing Saudi Arabia’s strategic approach to its substantial investments in the online gaming and e-sports industries necessitates a nuanced understanding of current global industry dynamics and associated risks.

Evaluating Saudi Banking Sector’s Priorities: Why Malaysia Rather Than India

Saudi banks' presence in Malaysia and absence from India reflects strategic and smart capital allocation aligning institutional capabilities with market structures that enable optimal monetization. Strategic selectivity recognizes structural differences, deploying capital where competitive advantages generate optimal returns.