|

Managing an air carrier, especially one as prominent as Riyadh Air, which’s the second flag carrier of Saudi Arabia, is an intricate endeavor fraught with challenges.

The collateral strategy

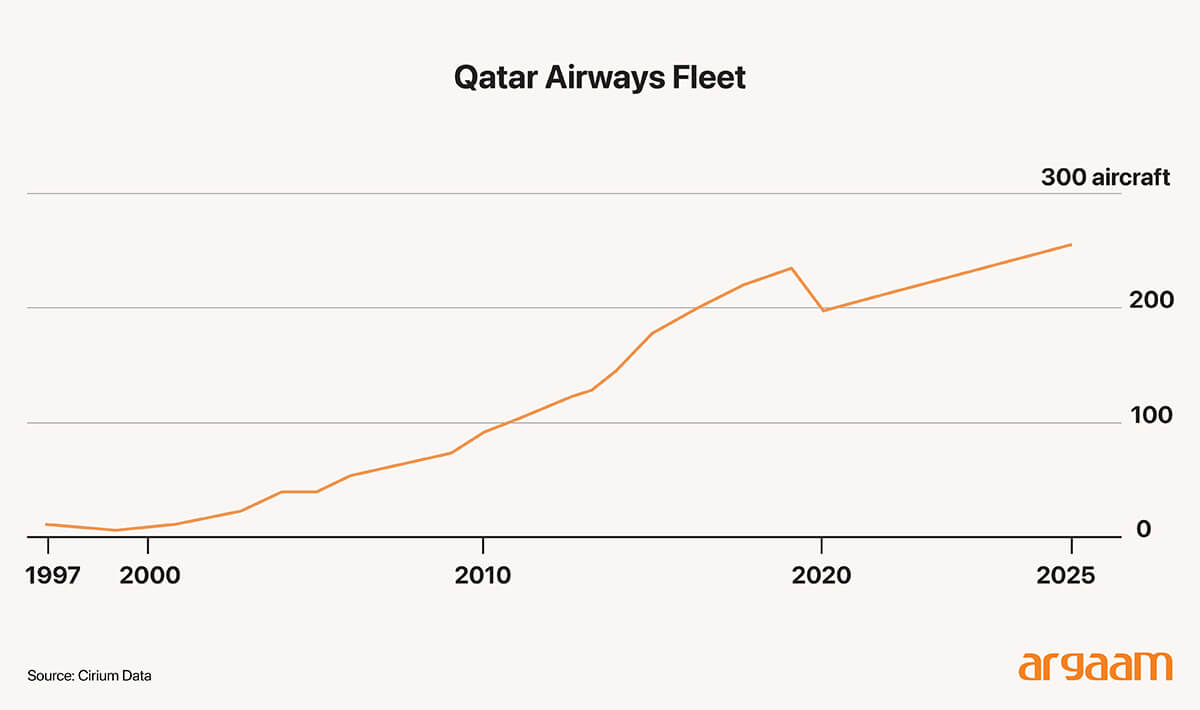

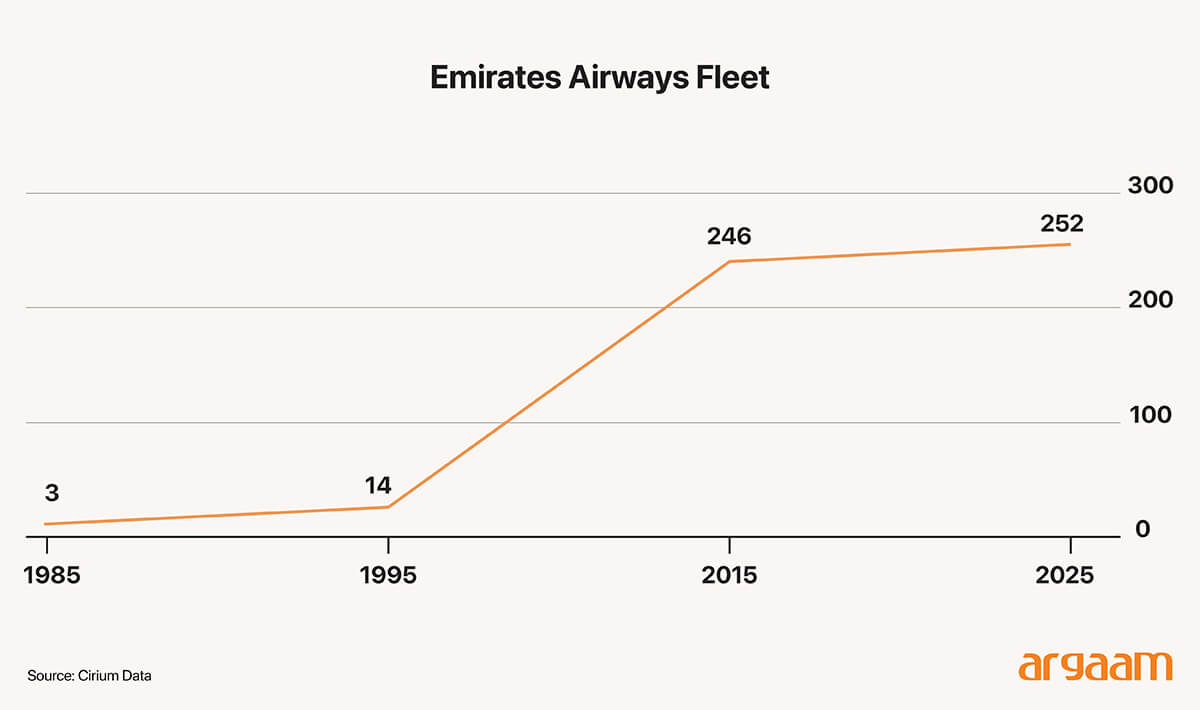

Launching its first commercial flights in early 2026, Riyadh Air is currently in the process of establishing its approximately 183 fleet which is mainly based on Boeing 787 and Airbus A350. The carrier already has made purchase orders of at least 72 aeroplanes. These are tangible assets that hold significant potential both as operational tools but also as financial assets, since their advanced technological features, fuel efficiency, and prolonged lifespan, up to 50 years for the Boeing 787 and around 30 years for the Airbus A350, enhance their attractiveness as collateral. Such aircrafts are highly marketable and recognized globally, ensuring that lenders view them as secure forms of collateral with relatively low depreciation risk over their operational life, potentially enabling the airline to obtain financing at favorable terms, such as lower interest rates. By offering these aircrafts as collateral, Riyadh Air can negotiate favorable loan terms to cover the cost of the additional 111 planes needed to complete its fleet. This suggestion allows the PIF to finance the fleet expansion without directly tying up its financial resources and preserve its capital for other high-value investments and multi-billion dollar deals.

Islamic bonds Saudi Arabia contributed to the global sukuk market's growth in 2025, accounting for 38.9% of the total market volume in the first half of the year. The global sukuk market is poised to maintain its strength in 2025, with foreign currency-denominated issuances expected to reach between $70 billion and $80 billion. In the first half of 2025, foreign currency sukuk issuances rose 8.94% year on year to $41.4 billion. The robust investor demand for Saudi Arabia's Sukuk, exemplified by the recent international issuance in September as reported by Argaam attracting an order book of approximately $19 billion (around 3.5 times the issued amount) underscores the deepening confidence in the kingdom’s Shariah-compliant bonds. The issuance’s scale demonstrates the market's readiness to support large-ticket projects like Riyadh Air and infrastructure investments with stable, long-term funding, reducing reliance on traditional debt that involves interest payments prohibited in Islam. The involvement of major global banks such as Citigroup, HSBC, JP Morgan, and Standard Chartered as joint global coordinators and active book-runners in the latest Sukuk issuance by Saudi Arabia is an important sign of the credibility of the Saudi Islamic bonds market. Their participation ensures the successful distribution of the Sukuk to a broad and diverse investor base worldwide. As Riyadh Air should seek to diversify its sources of funding beyond reliance on equity from the PIF, engaging these prominent banks, if it issues Islamic bonds, it will tap into international capital markets and enlist the expertise of these leading financial institutions to ensure the issuance's structural and regulatory robustness, making the Sukuk more attractive to international investors.

Powered by Revenue Streams A third financing method is based on an established concept in finance called ‘revenue bonds’, which’s explained in detail in an academic paper published by the University of Texas. It’s a form of debt that leverages the anticipated income generated by a specific project to secure funding. Unlike traditional bonds backed by the creditworthiness and financial strength by a government or a sovereign fund, revenue bonds are repaid solely from the revenue produced by the financed asset, making their success heavily dependent on the project's financial performance. So if Riyadh Air aims to expand its fleet by purchasing and not leasing new aircrafts to meet its its international flight goal by 2030 or increase its capacity, instead of relying on PIF funding, Riyadh Air could issue revenue bonds to finance the acquisition of these new aircrafts. he airline’s revenues from ticket sales, baggage fees, in-flight sales, and other related income from the flights operated by the new aircraft serve as the funds used to make bond payments. Each year in let’s say a 10-year bond agreement, Riyadh Air pays interest on the bonds, calculated at the agreed rate (for example 4% just for the sake of clarification). For a $1 billion bond issue, the annual interest might be $40 million. This interest is paid periodically (annually, semi-annually, depending on the bond terms) from the revenue generated.   One key revenue strategy we suggest in its initial phase is the implementation of dynamic pricing, with initial ticket prices set below regional competitors. This will presents a compelling opportunity to capitalize on excess demand early in its operational phase. Given that bookings are opening to the public early next year and that demand is anticipated to significantly outstrip supply, the airline can leverage this price advantage to attract a substantial customer base quickly. One might find this strange or counterintuitive as demand outstrips supply, but there’s a valid reason for this. This coming phase is vital for the launch as it can incentivize a large volume of early reservations to key destinations like London. This helps the airline quickly establish a customer base, build brand loyalty, and generate buzz around its services, as it takes to the high skies. |

|

|

|

|

|