|

In recent weeks, we have seen a striking moment on TikTok that captures the evolving landscape of luxury consumption among Saudi youths. Young Saudi men and women from Gen Z openly express that despite having the means to afford luxury wedding experiences including dresses or throw extravagant celebrations, they are choosing to think differently. Their videos have inspired us to write this analysis on this growing mindset in Saudi society prioritizing the experience itself in their own views rather than the traditional displays of wealth or the mere ownership of local luxury items like gold and luxury textiles. This reflects a significant shift in consumer behavior within the luxury market in the kingdom. Taking into consideration these young voices on social media and studying the market including the latest report on the State of Fashion Luxury by McKinsey & Company, we believe that it is crucial for Saudi luxury houses to shift their strategic focus from traditional notions of culture and authenticity toward aligning with the actual preferences of young Saudis and what they really want to buy to become competitive with international brands. As of the end of 2024, the six Gulf Cooperation Council (GCC) countries have a combined luxury market value north of $16.9 billion. Saudi Arabia commands about 40% of the region’s luxury market, certain to increase with more international luxury retailers relocating stores to the kingdom. The United Arab Emirates holds the largest market share at nearly 50%. Also, given Saudi Arabia’s demographic landscape where over 63% of the population under the age of 30 as of 2023, it is imperative for Saudi luxury brands to recalibrate their offerings to appeal to Saudi Gen Z consumers.

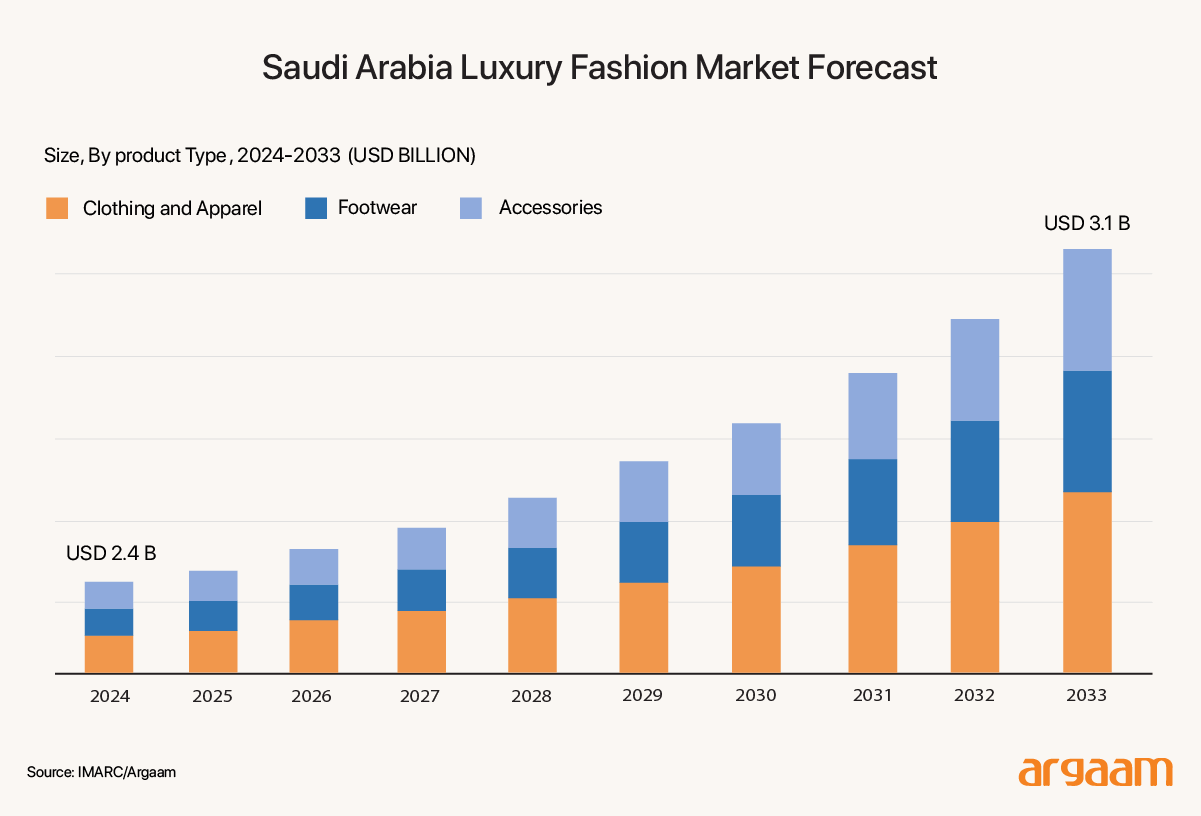

Prioritizing Financial Metrics The core shift involves moving from a focus on storytelling rooted in heritage to a completely different approach which emphasizes financial performance, operational scalability, and long-term sustainability. While creative artistry remains fundamental to the essence of luxury brands, recent industry data from the kingdom shows us why it’s important to prioritise financial metrics over creative artistry, brand heritage, or emotional value. The Saudi Arabia luxury fashion market size reached $2.4 Billion in 2024. Looking forward, it’s expected the market to reach only $3.1 Billion by 2033, exhibiting a growth rate (CAGR) of 3.09% during 2025-2033. The market's largest segment is the watches and jewelry with a market volume of $856.62 m in 2025.

Since the luxury consumption is driven more by the average expenditure on luxury goods per household irrespective of the number of population, we compare the Saudi market growth to another market in an emerging economy like India. An economy with high disposable income can have a more substantial luxury market than a larger population with lower average income. Saudi Arabia's household disposable income was $18,260 per year in 2025 compared to less than $10,000 per household in India. The luxury fashion market in India was valued at an estimated $9.37 billion in 2024, with a forecast to reach $15.13 billion by 2033, growing at a CAGR of 5.03% during the 2025-2033 period. The Saudi luxury fashion market’s modest growth signifies that luxury consumption is static. If Saudi luxury brands aim to maintain a strong balance sheet in a market where younger consumers are increasingly gravitating toward international brands and Western fashion norms, it is crucial for them to adapt their strategies to prioritize relevance and consumer engagement. Relying solely on traditional notions of craftsmanship or artisanal storytelling may no longer suffice to capture the attention and loyalty of this digitally influenced demographic. Our analysis is identical to insights from Sabyasachi Mukherjee, who cannily built India's largest luxury brand specialised in the traditional saree. He said in a TV interview in March 2025 that he had to re-focus his business model towards producing western-style clothes for the luxury customers with his brand but with Indian materials and labour if the brand wanted to remain competitive in the Indian market.

The Strategic Role of Licensing in Saudi Luxury Growth Given the market's slow growth and shifting consumer preferences, striking licensing agreements with international brands can help Saudi local luxury brands to leverage this reputation. Such partnerships remain important despite modest and forecasted slow growth in the global luxury market because they offer strategic advantages, chiefly to produce, sell, or distribute products under the international brand’s name using Saudi materials and integrating Saudi cultural elements into the product design, branding, and marketing narratives, without the need to create a new luxury brand from scratch. Globally renowned brands often possess exclusive designs, innovative materials, and signature styles that are difficult for nascent local brands to replicate independently. Luxury fashion giants believe that it takes at least a hundred years for a luxury brand to be built, as it needs to establish a deep heritage rooted in craftsmanship, quality, and above all exclusivity and identity. (Hermès, Cartier and Louis Vuitton are all over 170 years old). This long history fosters trust and emotional connection with consumers. Trust accumulates over generations of consistent quality, storytelling, and exceptional customer experiences, going beyond the mere financial transaction aspect since a luxury brand should cultivate a community of loyal customers.  Money-can’t-buy Experiences Internationally well-established luxury brands are shifting focus from traditional brand-centric and product-centric models to creating immersive, “money-can’t-buy” experiences. International luxury brands are investing heavily in tech, AI, and data analytics to better understand and personalize the customer journey for Gen Z. Accordingly, they are hosting bespoke events, private viewings, and exclusive meet-and-greets that are tailored for high-value or promising Gen Z customers. These events often involve personalized interaction with designers or celebrities, and are instrumental in building long-term customer lifetime value. Brands like Louis Vuitton or Prada offer made-to-order services, allowing customers to customize bags, shoes, or accessories with unique embroidery, materials, or design elements. This personalized service commands premium pricing, often 2-3 times the standard product price, reflecting the value placed on exclusivity that comes with a big name. For instance, a custom Louis Vuitton bag could retail for €10,000-€50,000, compared to a mass-produced version costing around €2,000, with the premium justified by the bespoke experience. Digital innovations include virtual reality (VR) previews of upcoming collections, exclusive virtual meet-and-greets with designers, or limited-edition digital collectibles (NFTs). These virtual experiences are often offered to top-tier clients as a digital 'access pass'—creating a sense of exclusivity. While direct sales are harder to quantify, such initiatives foster digital loyalty, potentially increasing lifetime spend by 10-20% among Gen Z customers, according to industry estimates.

The Shift in Luxury Values While sustainability may not be the primary factor in luxury purchasing, Gen Z consumers place high importance on ethics, transparency, and social responsibility. British luxury fashion designer Stella McCartney could easily have opted for the route of traditional luxury brands. Instead, she has been a trailblazer in sustainable luxury fashion since establishing her eponymous label in 2001. From the outset, McCartney eschewed the use of leather, fur, and feathers in all designs, a revolutionary stance in the luxury fashion industry at the time. Beyond her core brand, she continues to invest in emerging fabric alternatives. The Gen Z luxury fashion customers are different than their parents and the old generations. A recent academic research titled “Sustainability preferences of luxury consumers: Is all that glitters green?” that the older generations perceive sustainability as a "good-to-have" feature rather than a necessity, and thus do not allocate additional financial resources for it. The research, based on interviews with affluent German respondent, found that even when sustainability messages are communicated by brands, these consumers tend to ignore or dismiss them when making purchase decisions, focusing instead on factors like product quality and brand prestige. |

|

|

|

|

|